How Safe are European Safe Bonds? An Analysis from the Perspective of Modern Portfolio Credit Risk Models

Published 30 Jan 2020 in q-fin.PR, q-fin.MF, and q-fin.RM | (2001.11249v2)

Abstract: Several proposals for the reform of the euro area advocate the creation of a market in synthetic securities backed by portfolios of sovereign bonds. Most debated are the so-called European Safe Bonds or ESBies proposed by Brunnermeier, Langfield, Pagano,Reis, Van Nieuwerburgh and Vayanos (2017). The potential benefits of ESBies and other bond-backed securities hinge on the assertion that these products are really safe. In this paper we provide a comprehensive quantitative study of the risks associated with ESBies and related products, using an affine credit risk model with regime switching as vehicle for our analysis. We discuss a recent proposal of Standard and Poors for the rating of ESBies, we analyse the impact of model parameters and attachment points on the size and the volatility of the credit spread of ESBies and we consider several approaches to assess the market risk of ESBies. Moreover, we compare ESBies to synthetic securities created by pooling the senior tranche of national bonds as suggested by Leandro and Zettelmeyer(2019). The paper concludes with a brief discussion of the policy implications from our analysis.

The paper introduces an affine credit risk model with regime switching to quantify ESBies' expected loss and market risk.

The analysis demonstrates that under normal conditions, ESBies offer robust diversification, making them safer than many euro area sovereigns.

The study compares ESBies to PSNTs, highlighting ESBies' stability across varying LGD assumptions even in crisis scenarios.

How Safe are European Safe Bonds? An Analysis from the Perspective of Modern Portfolio Credit Risk Models

Introduction

The paper "How Safe are European Safe Bonds? An Analysis from the Perspective of Modern Portfolio Credit Risk Models" investigates the safety of European Safe Bonds (ESBies), synthetic securities backed by diversified portfolios of euro area sovereign bonds. These bonds are proposed to enhance stability in the European monetary union by increasing the supply of safe assets and mitigating the sovereign-bank nexus. The analysis employs an affine credit risk model with regime switching to assess the risk profile of ESBies, focusing on their expected loss and market risk under varying economic scenarios.

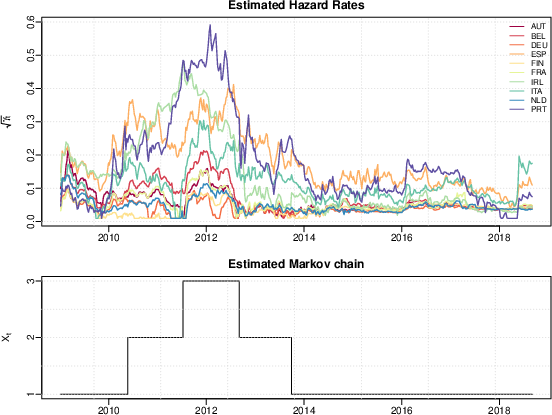

Default Model and Calibration

The model considers euro area sovereigns as obligors with default times driven by CIR-type dynamics, modulated by a finite-state Markov chain representing economic regimes. Default intensities are conditionally independent, allowing for efficient calibration to historical CDS spreads. The calibration, conducted over a decade, supports the regime-switching setup with states interpreted as expansion, mild recession, and strong recession. Hazard rate trajectories are crucial for assessing ESBies' credit risk and simulating spread behavior over time.

Figure 1: Time series plots of the estimated hazard rates and the calibrated Markov chain. Note that we graph γt.

Risk Analysis

Expected Loss and Crisis Scenarios

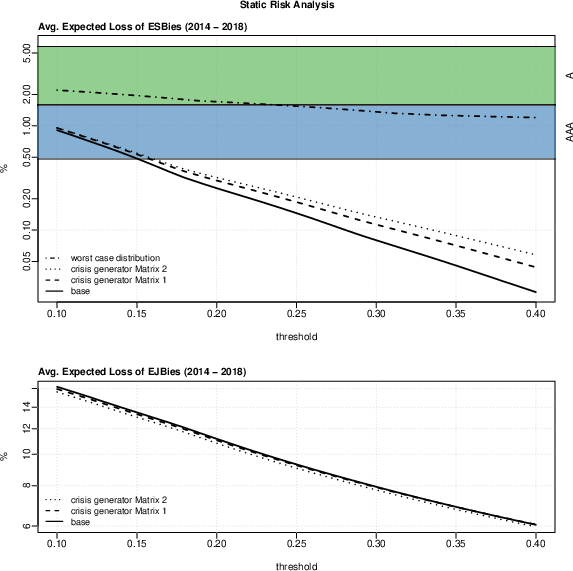

The paper quantifies the risk-neutral expected loss of ESBies, demonstrating that with typical subordination levels, ESBies remain safer than many euro area sovereigns. The analysis confirms that, under normal conditions, ESBies offer robust diversification benefits due to their construction from pooled sovereign debt.

Figure 2: Average expected loss of ESBies for different thresholds and parameterizations (in \%).

However, when subjected to crisis scenarios—particularly with altered transition intensities in the Markov chain—the loss probability increases. These scenarios underline the necessity of choosing conservative attachment points for ESBies to maintain their safety characteristics.

Spread Trajectories and Market Risk

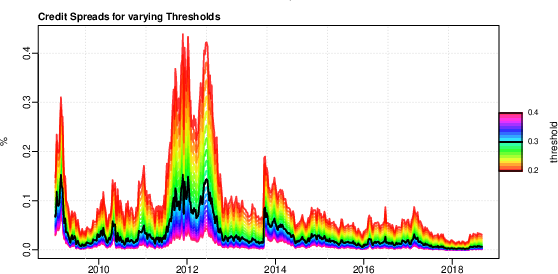

To further assess ESBies' robustness, the paper examines historical spread trajectories under varying economic states. It reveals that ESBies with lower attachment points exhibit significant volatility, indicating vulnerability during financial distress.

Figure 3: Spread trajectories of ESBies with varying threshold levels.

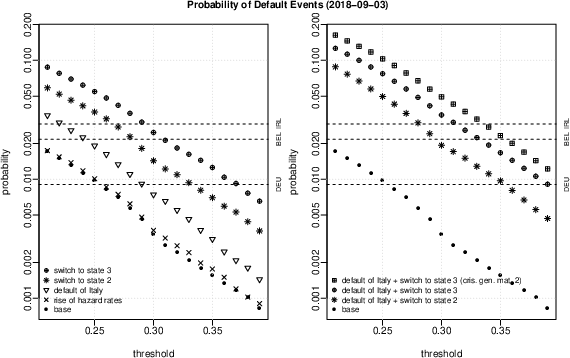

Additional market risk analysis, encompassing loss probability under contagion scenarios, suggests that policy measures should accompany ESBie issuance to mitigate default contagion effects. These include improving risk sharing mechanisms within the euro area.

Comparing PSNTs and Robustness with Respect to LGD Variance

The analysis compares ESBies to pooled senior national tranches (PSNTs), an alternative proposal for creating euro area safe assets. It demonstrates that while PSNTs' expected loss is highly sensitive to assumptions about loss given default (LGD), ESBies are comparatively stable across varying LGD specifications. This highlights ESBies' advantage in capitalizing on sovereign diversification.

Figure 4: Spread of ESBies and PSNTs for varying κ and different LGD variance.

Conclusion

The paper concludes that, under normal conditions, ESBies are effective safe assets. However, their robustness against extreme scenarios necessitates careful consideration of attachment points and complementary policy interventions. The introduction of ESBies, alongside measures to limit contagion risk, could significantly enhance the euro area's financial stability.