- The paper introduces a dynamic curve mechanism for AMMs that eliminates arbitrage by aligning pool prices with market prices via price oracles.

- It uses real-time simulations comparing static and dynamic AMMs, showing significant improvements in liquidity maintenance and asset value stability.

- Dynamic curves convert trader slippage into liquidity provider gains, thereby enhancing economic efficiency in decentralized cryptocurrency exchanges.

Dynamic Curves for Decentralized Autonomous Cryptocurrency Exchanges

Introduction

The paper "Dynamic Curves for Decentralized Autonomous Cryptocurrency Exchanges" proposes a novel mechanism for Automated Market Makers (AMMs) in the decentralized finance (DeFi) sector. It addresses critical issues such as liquidity depletion and value reduction caused by arbitrageurs in existing AMMs like Uniswap and Curve, which rely on static liquidity pool models. The introduction of dynamic curves, modulated by a market price oracle, aims to ensure that pool prices automatically adjust to reflect market prices, thus eliminating arbitrage opportunities and maintaining higher liquidity and value.

Mechanism of Dynamic Curves

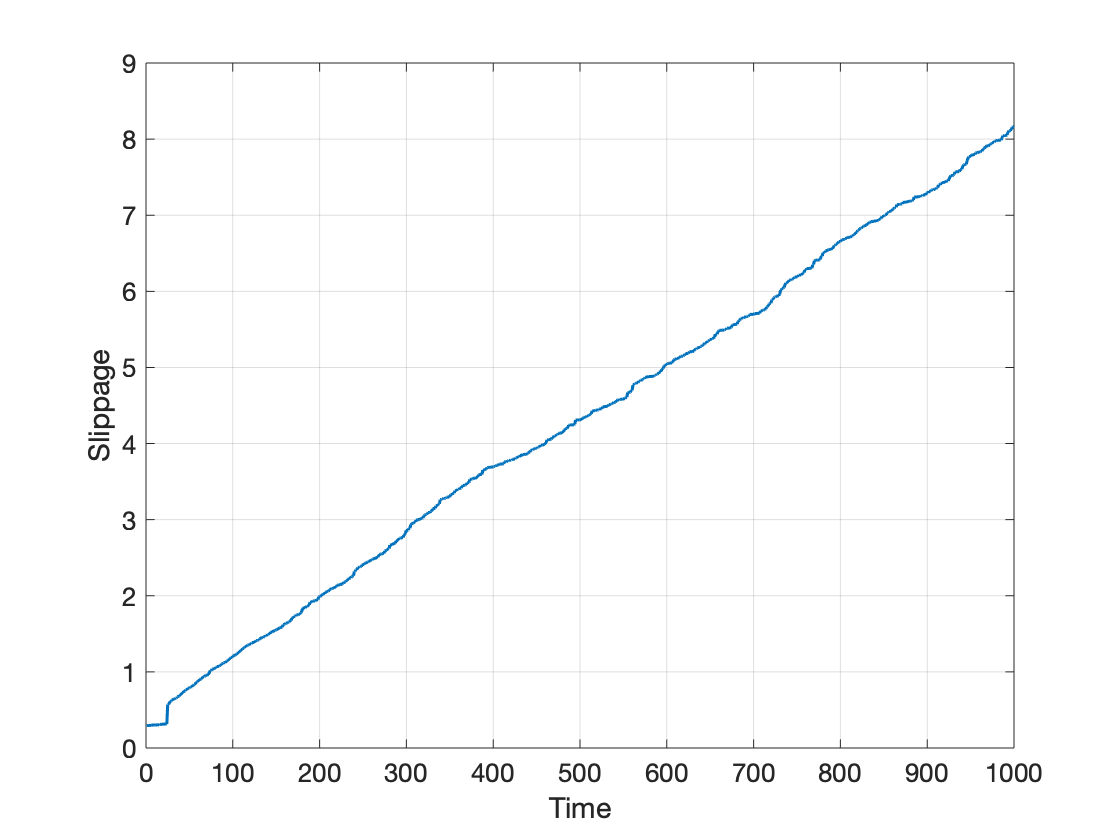

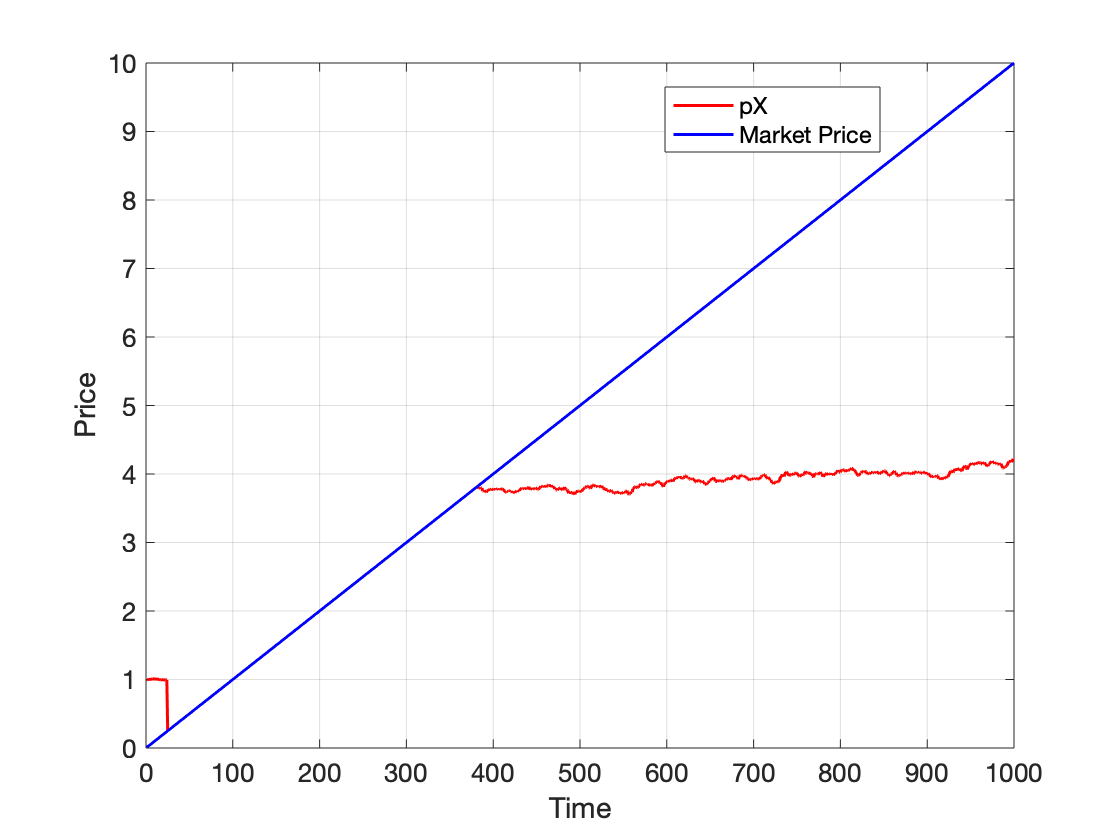

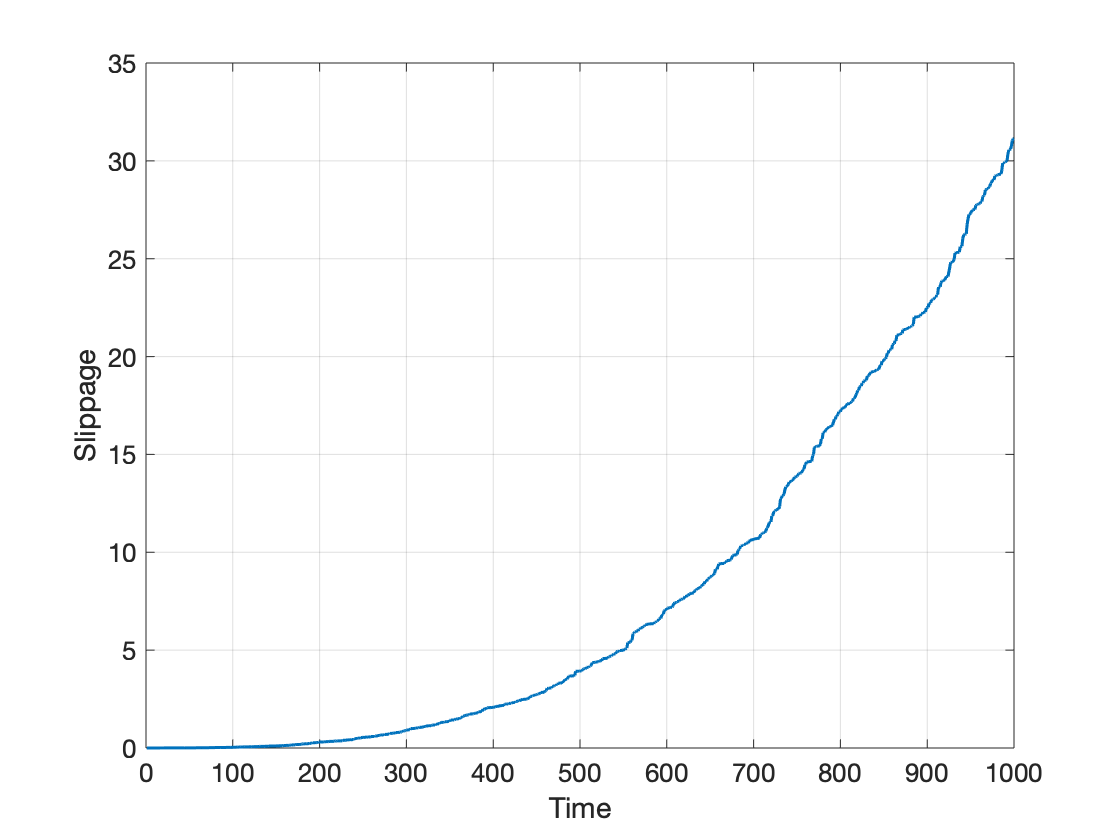

The concept of dynamic curves involves adjusting the mathematical relationship (curve) between assets in an AMM in real-time via input from a market price oracle. This mechanism ensures that the pool price constantly reflects the market price for any given asset, obviating the need for external arbitrage to maintain equilibrium. By maintaining parity between pool and market prices, the system eliminates divergence loss and converts trader slippage loss into liquidity provider gains, enhancing the economic efficiency of decentralized exchanges.

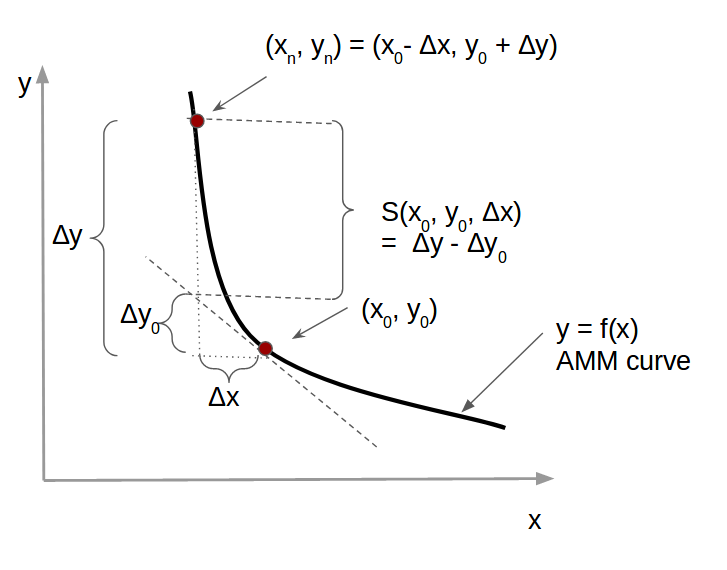

Figure 1: Illustration of Price Slippage on a Trade.

Advantages Over Static AMMs

Static AMMs, like constant-sum and constant-product models, often rely on arbitrageurs to realign pool and market prices, incurring losses in liquidity and total value. The dynamic approach outlined generalizes these static models, allowing for adaptive curve parameters that automatically synchronize with market conditions. This adaptability ensures sustained liquidity across a broader range of market conditions and preserves pool value without external intervention.

Key features of dynamic curves include:

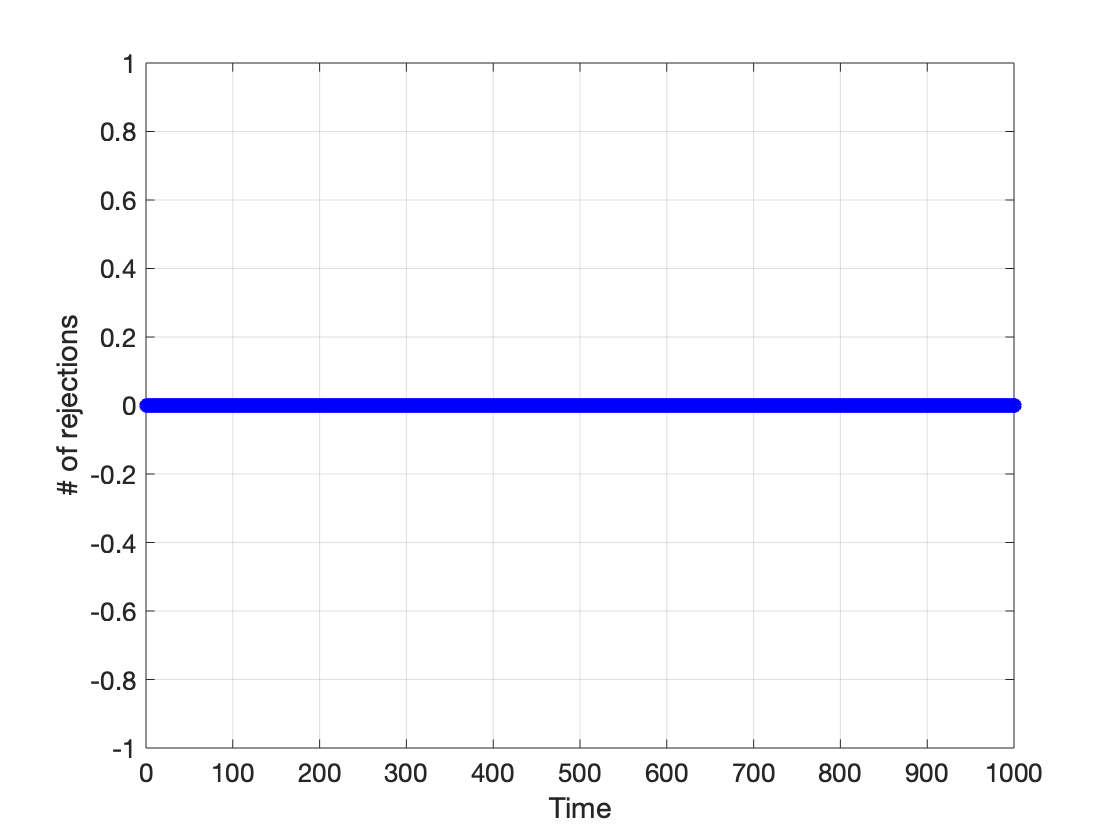

- Elimination of Arbitrageurs: By continuously aligning pool prices with market prices, dynamic curves remove arbitrage incentives, preserving liquidity and reducing value diminution.

- Improved Liquidity: Dynamic curves adaptively maintain liquidity, especially during volatile market shifts, thereby serving small traders more effectively.

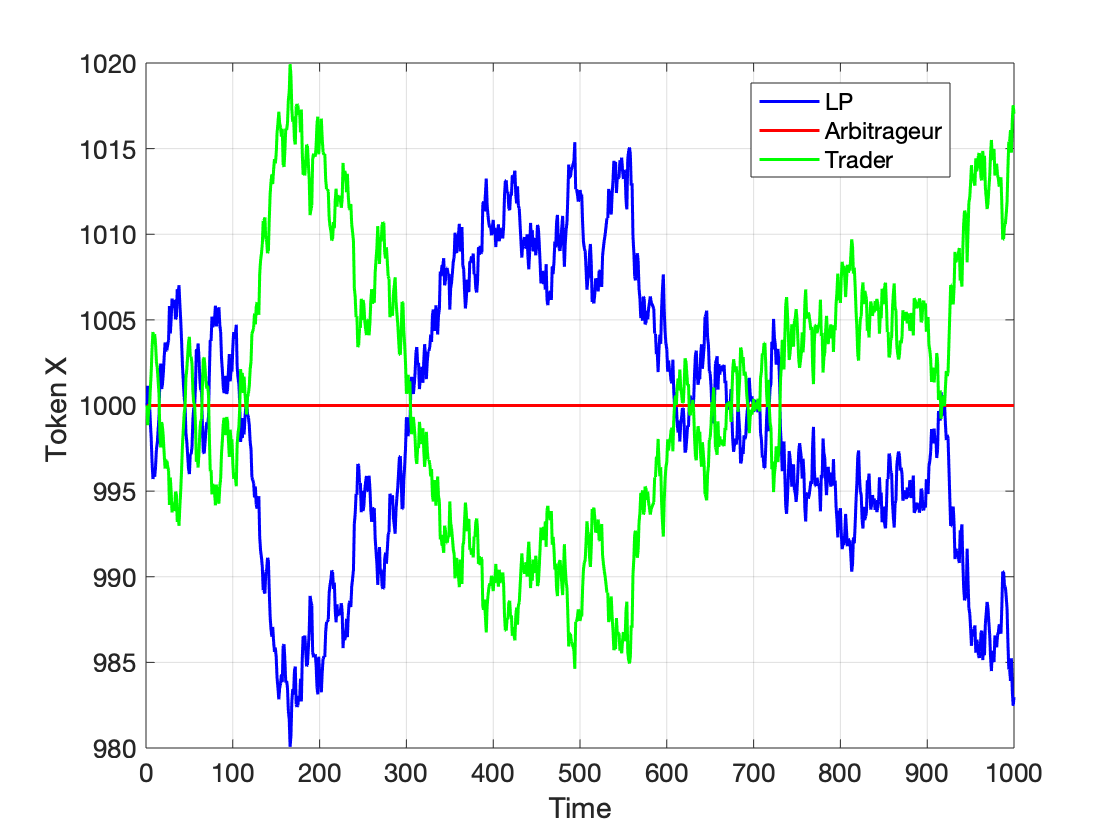

- Gain from Slippage: Slippage loss incurred by traders is directly translated into gains for the liquidity pool, providing a tangible financial benefit to liquidity providers.

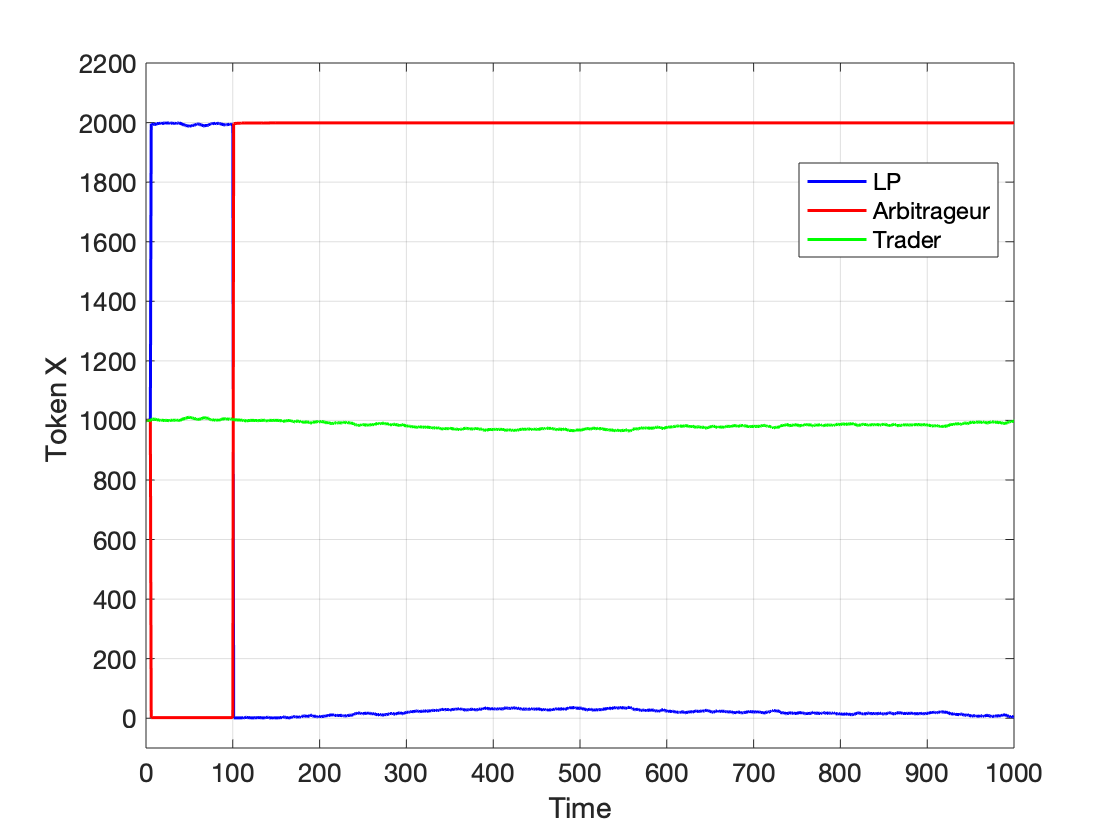

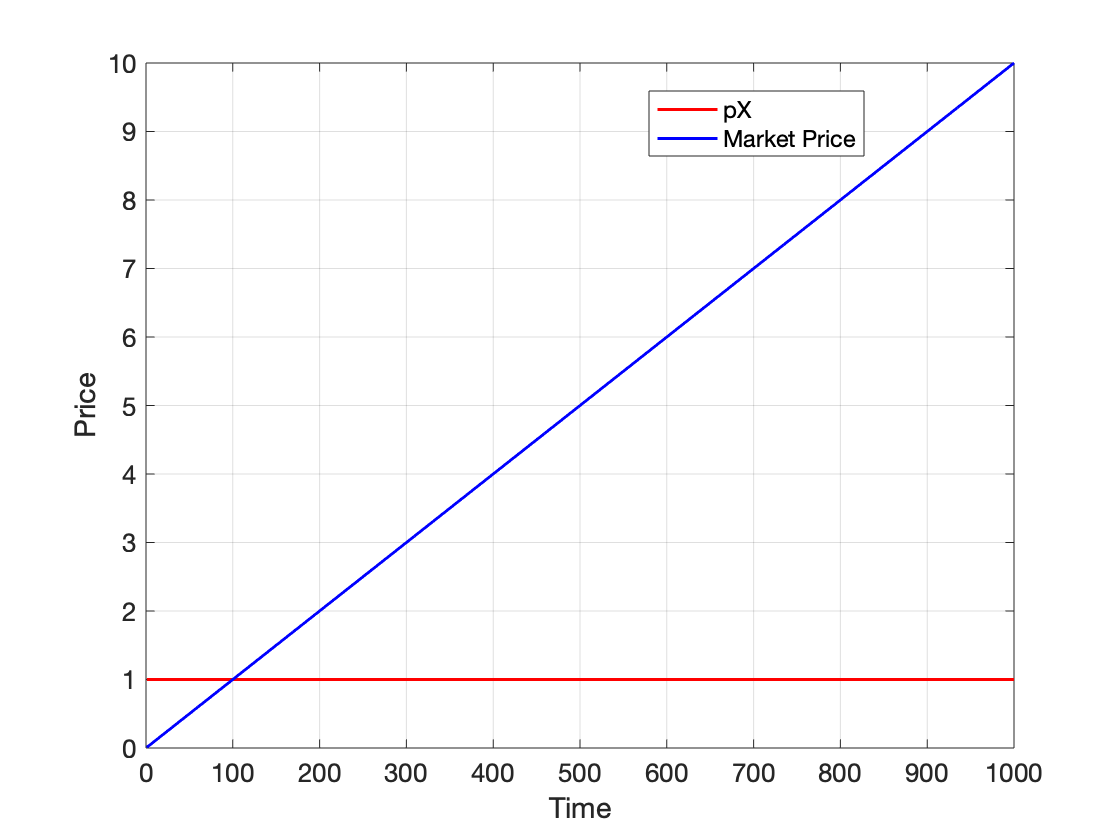

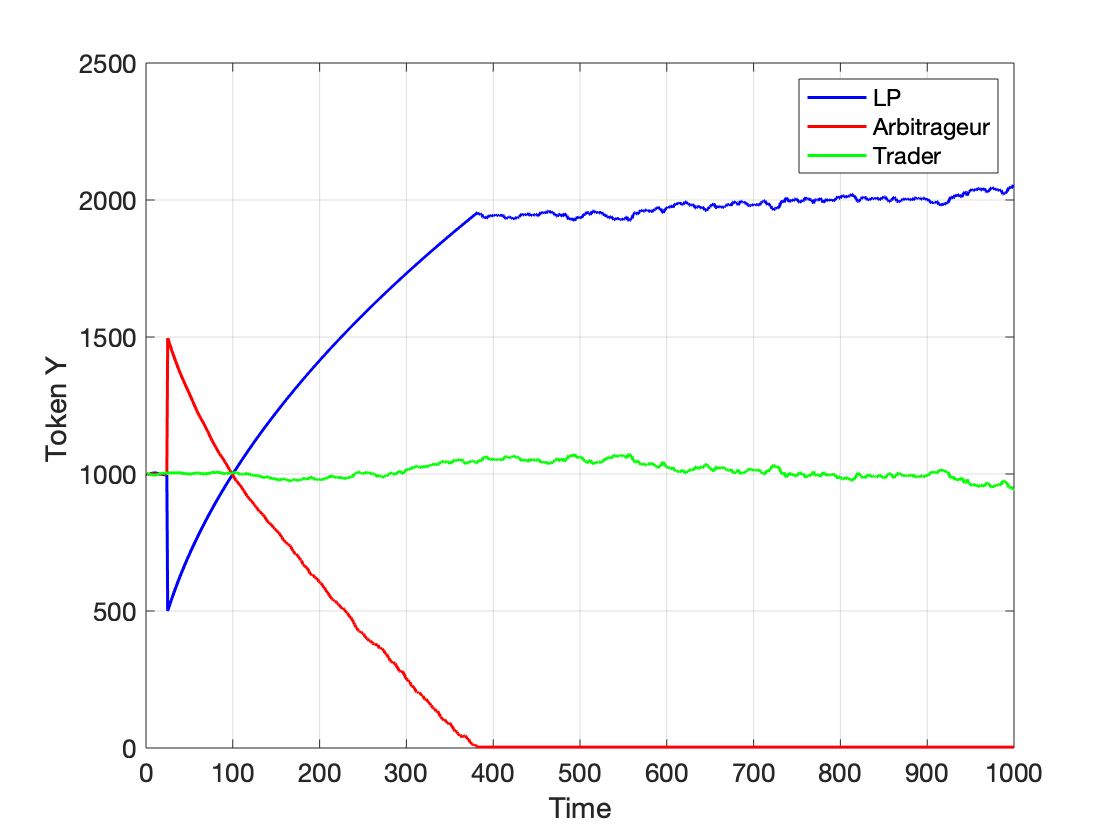

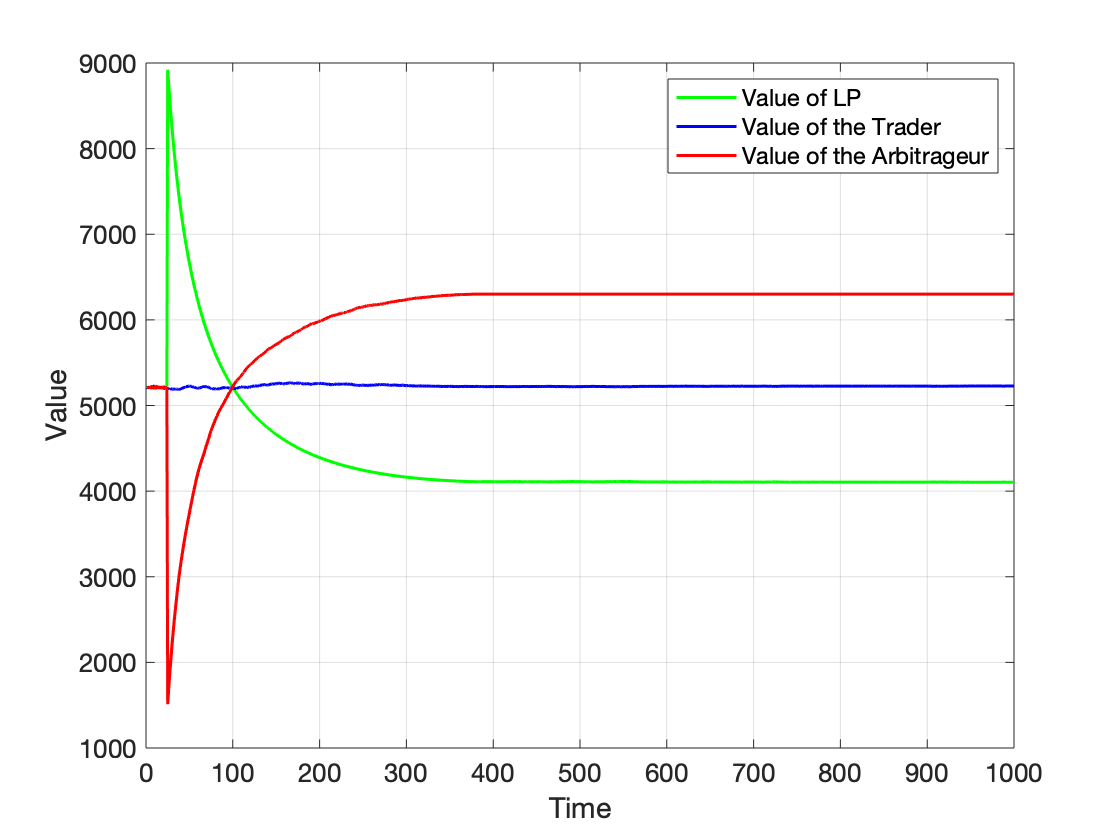

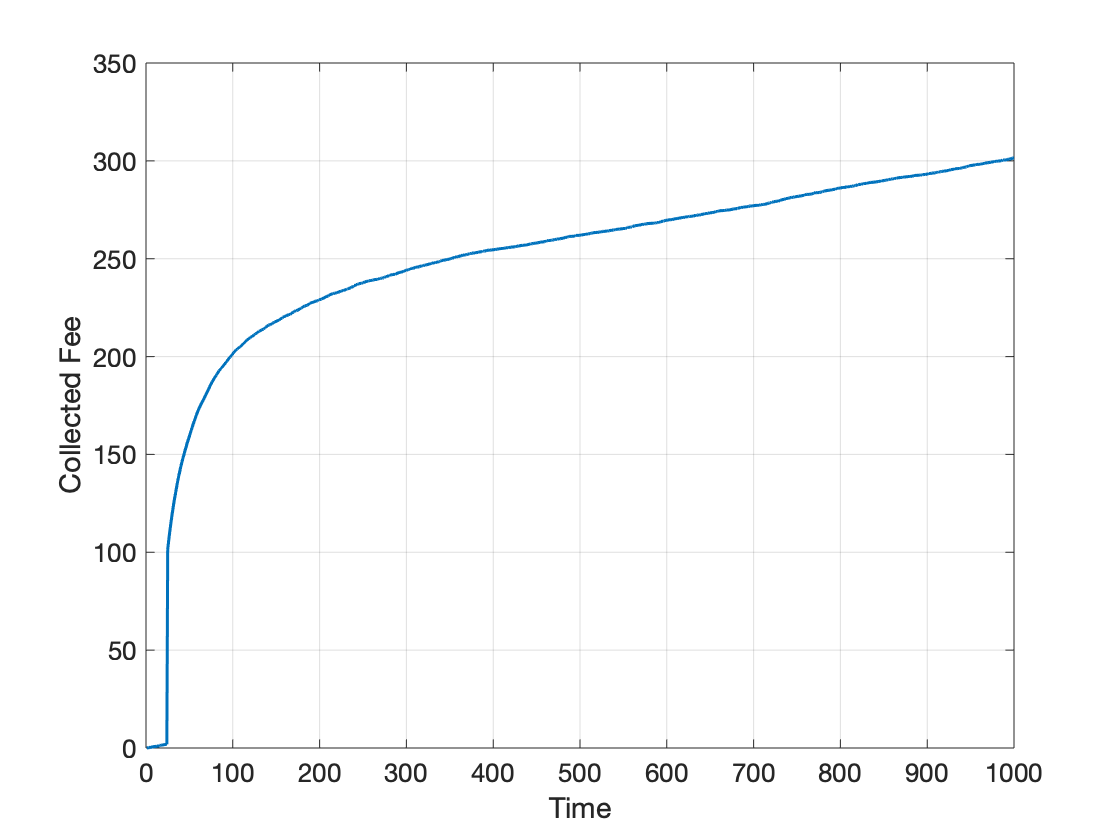

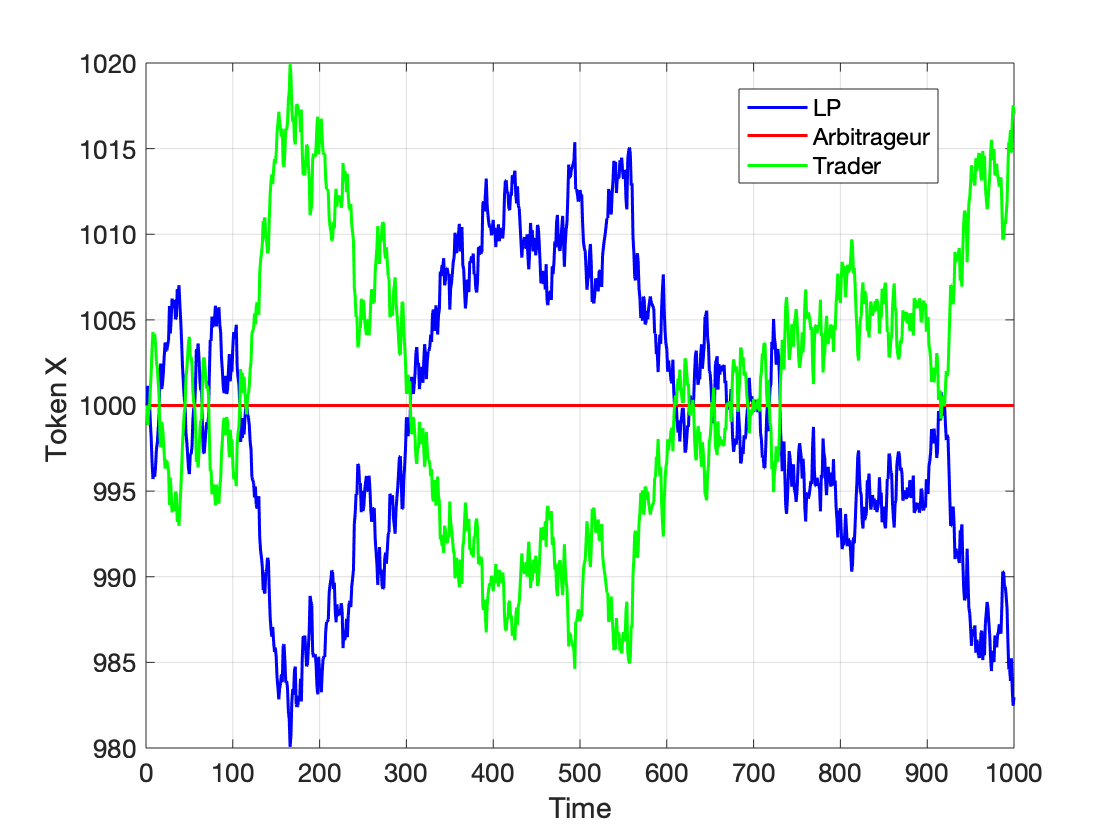

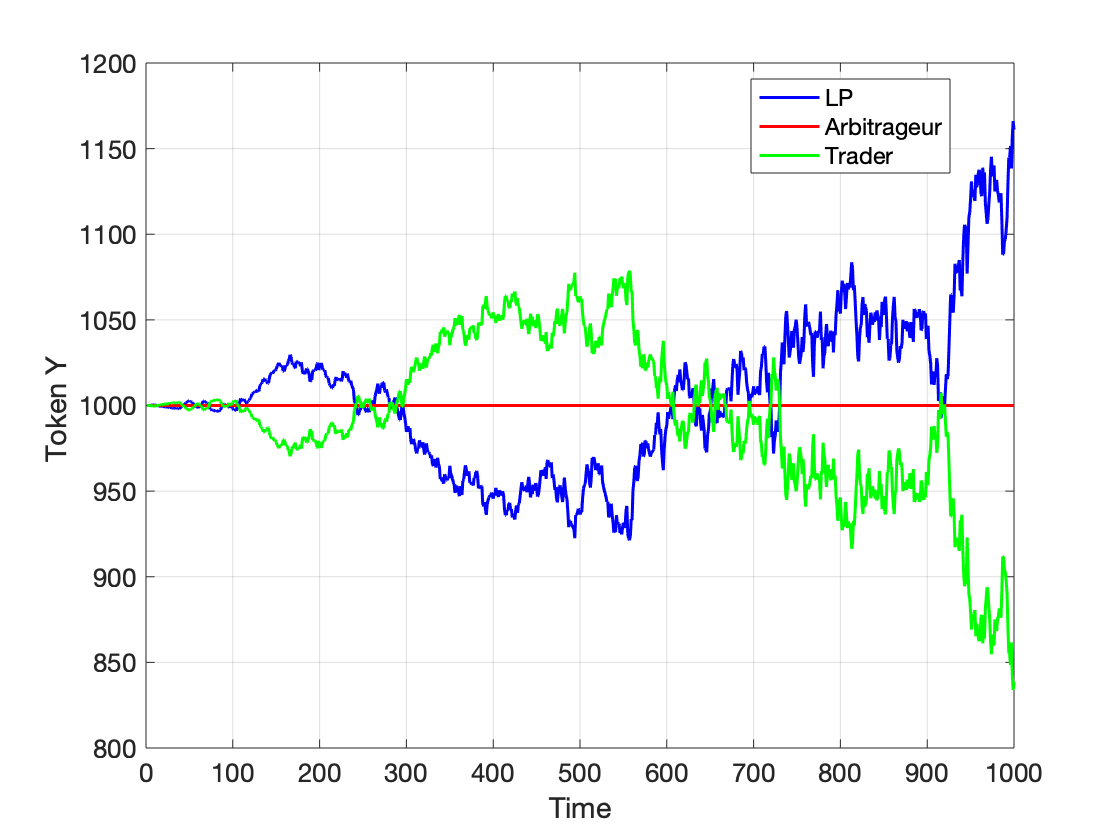

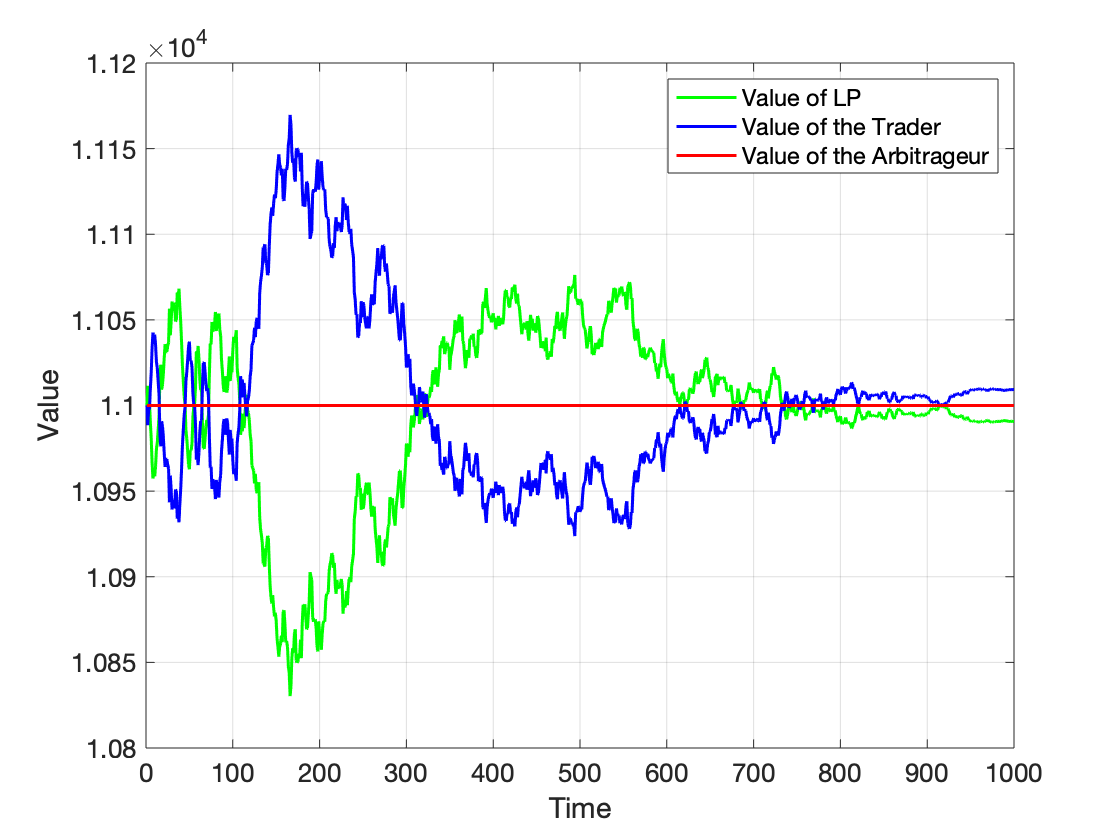

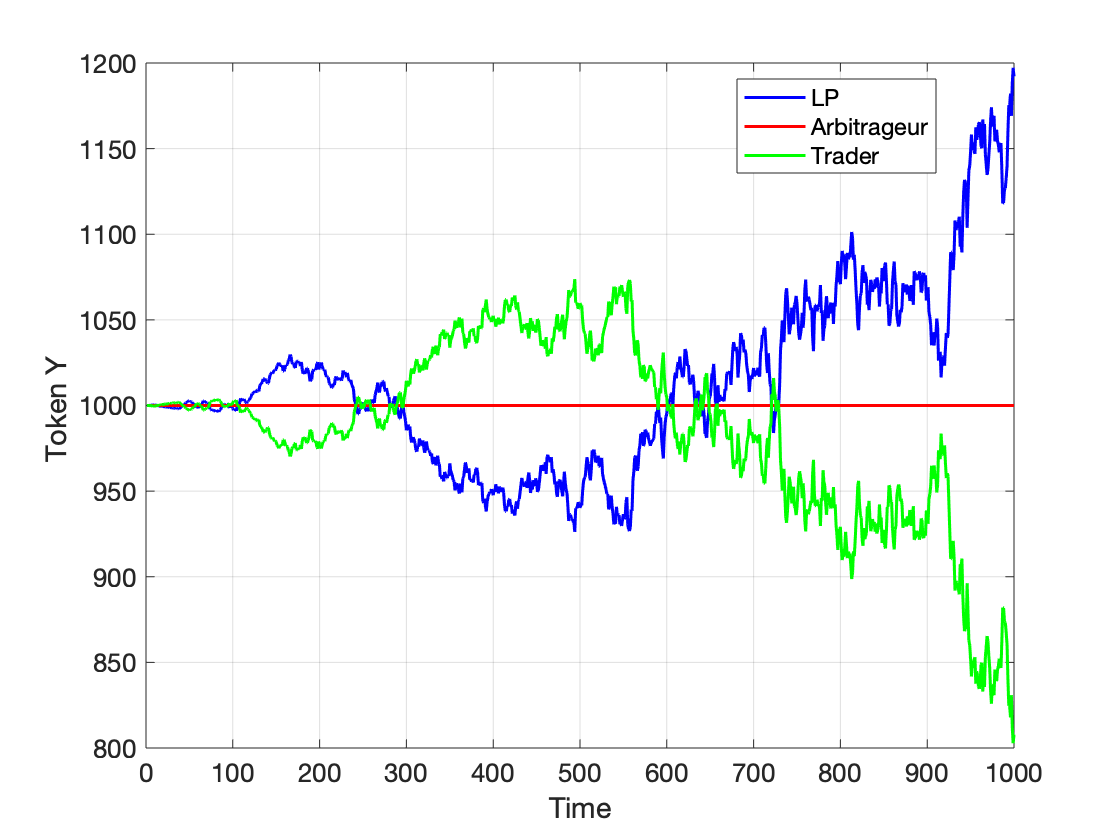

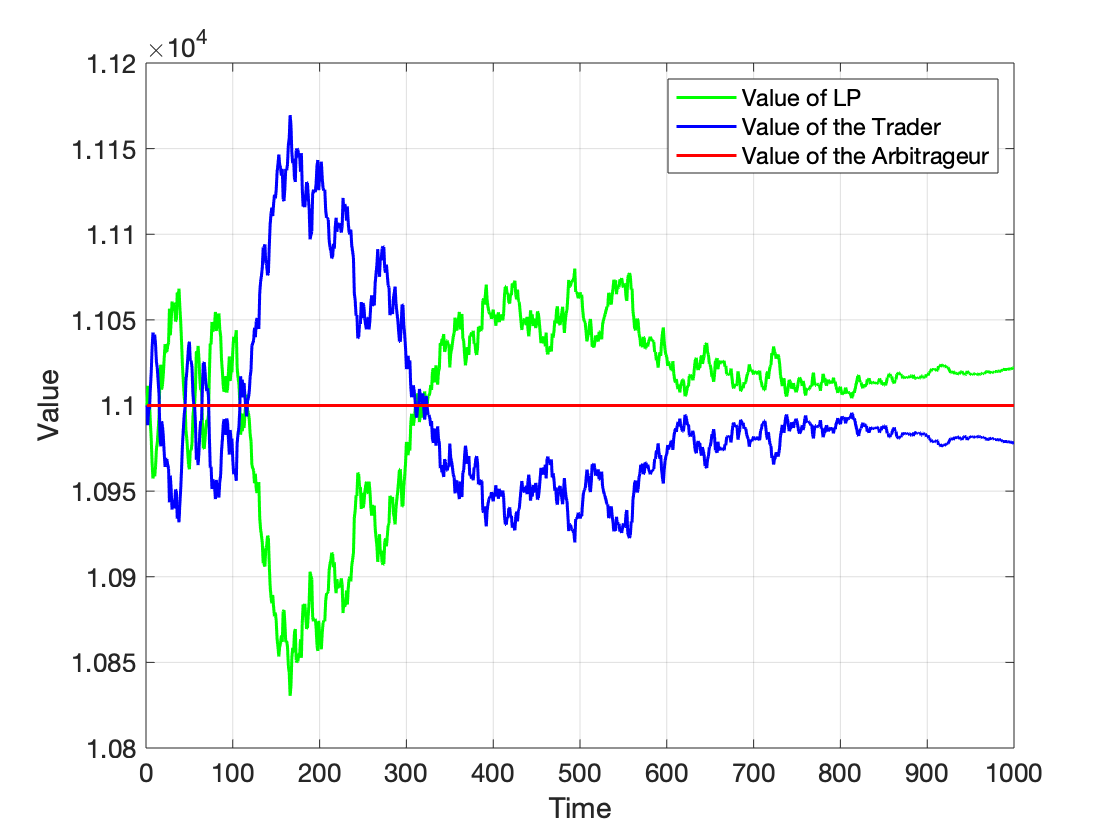

Figure 2: Simulation of a Static Constant Sum AMM.

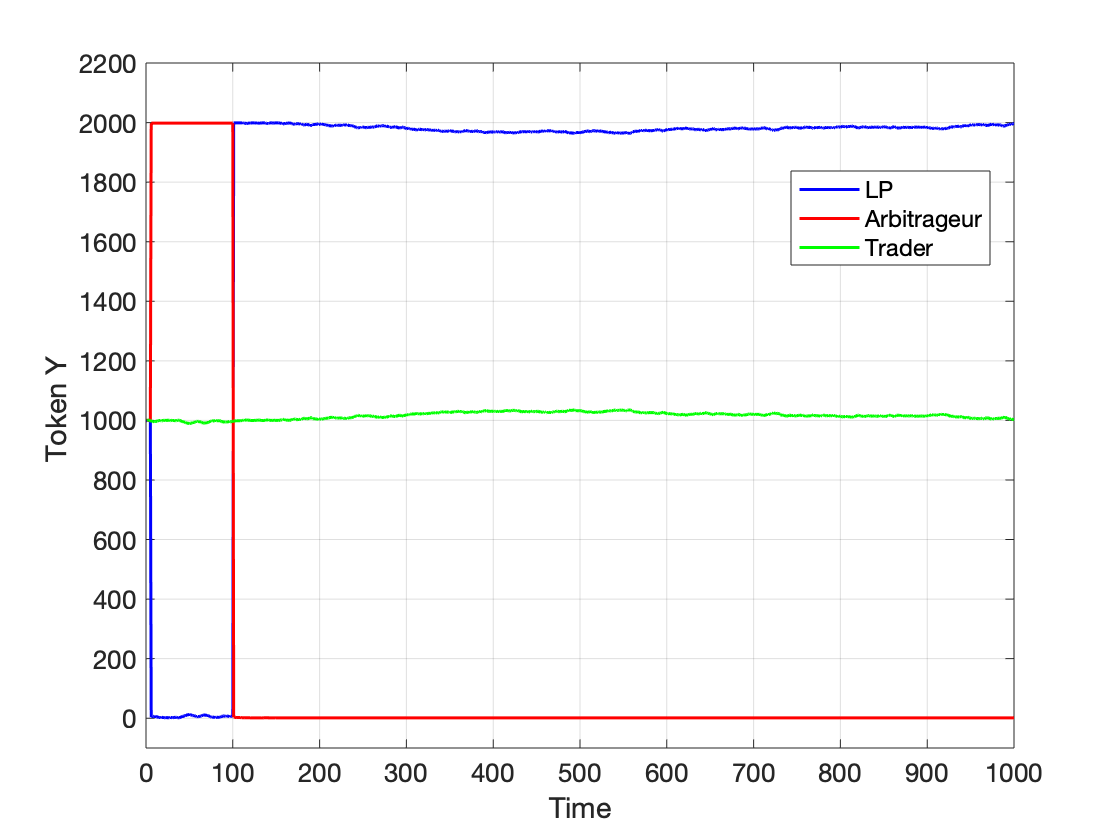

Figure 3: Simulation of a Static Constant Product AMM.

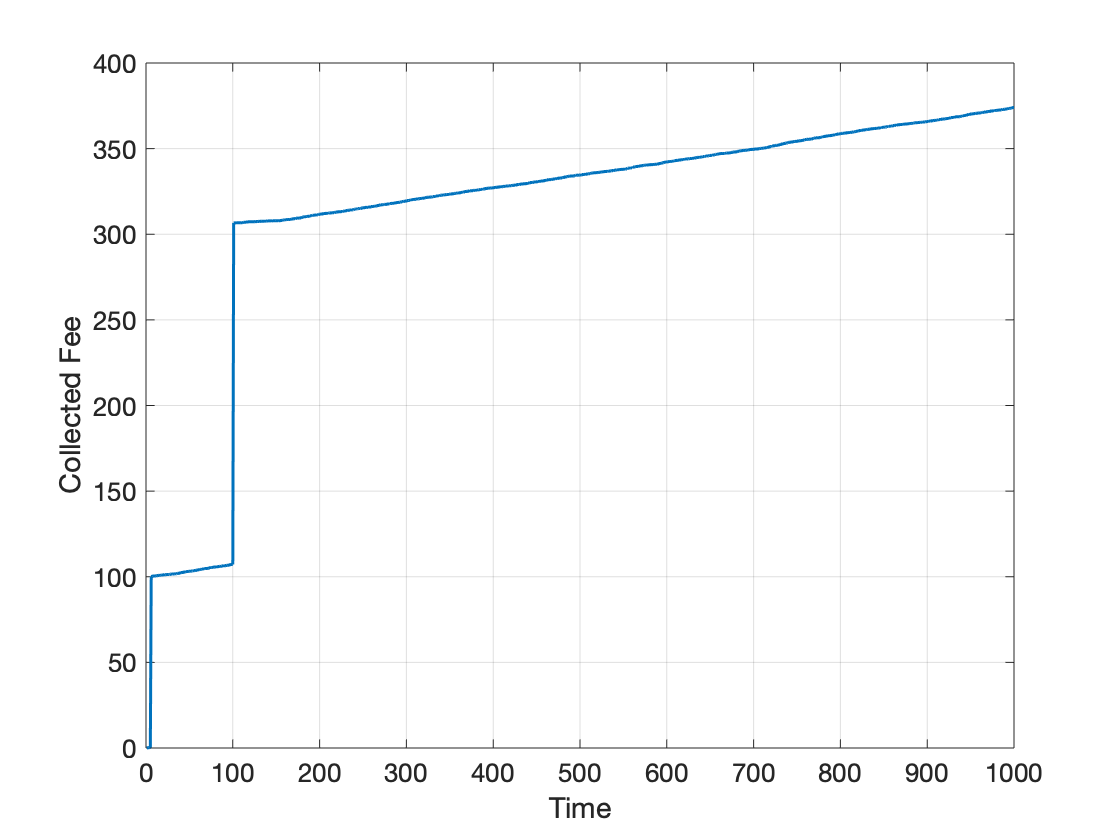

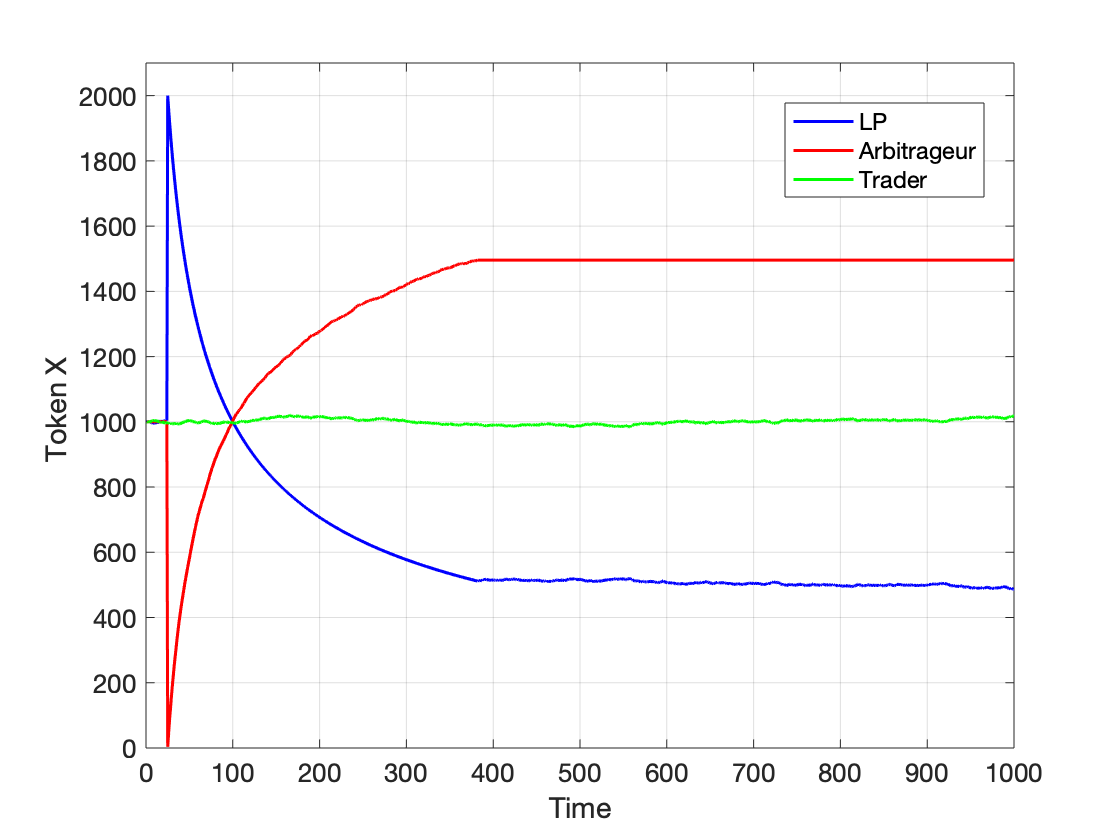

Simulation Insights

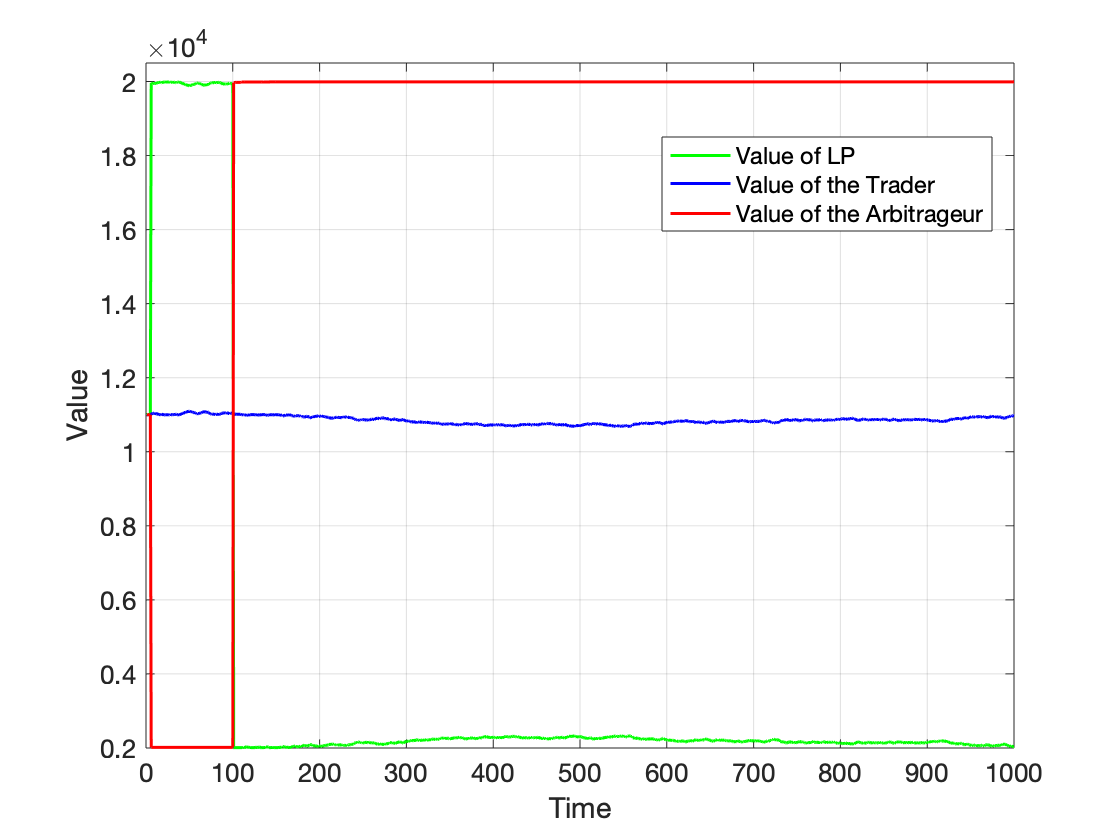

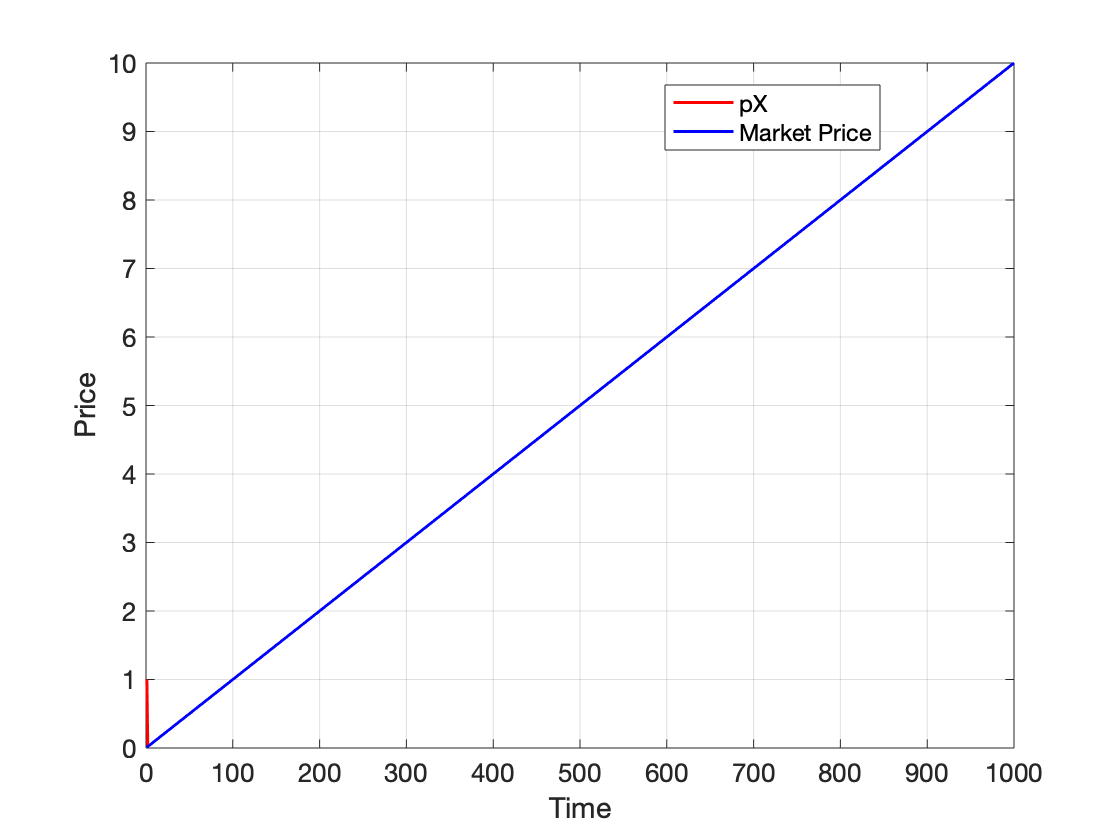

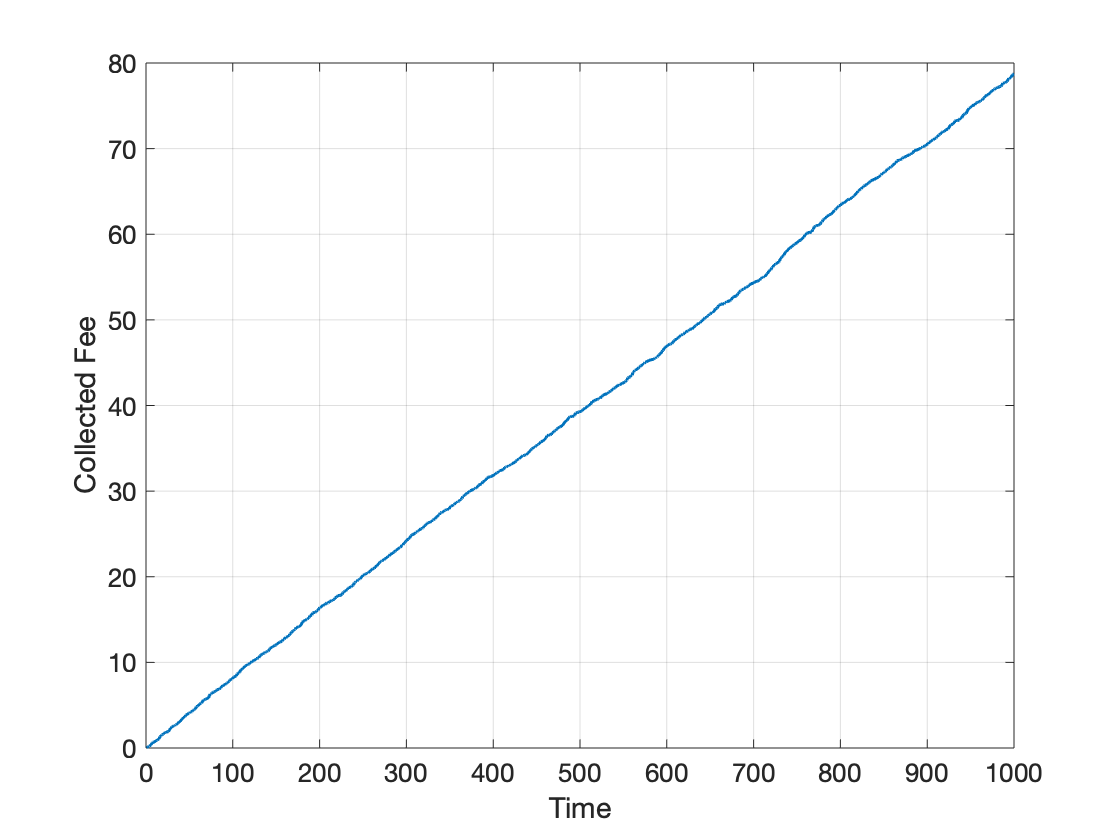

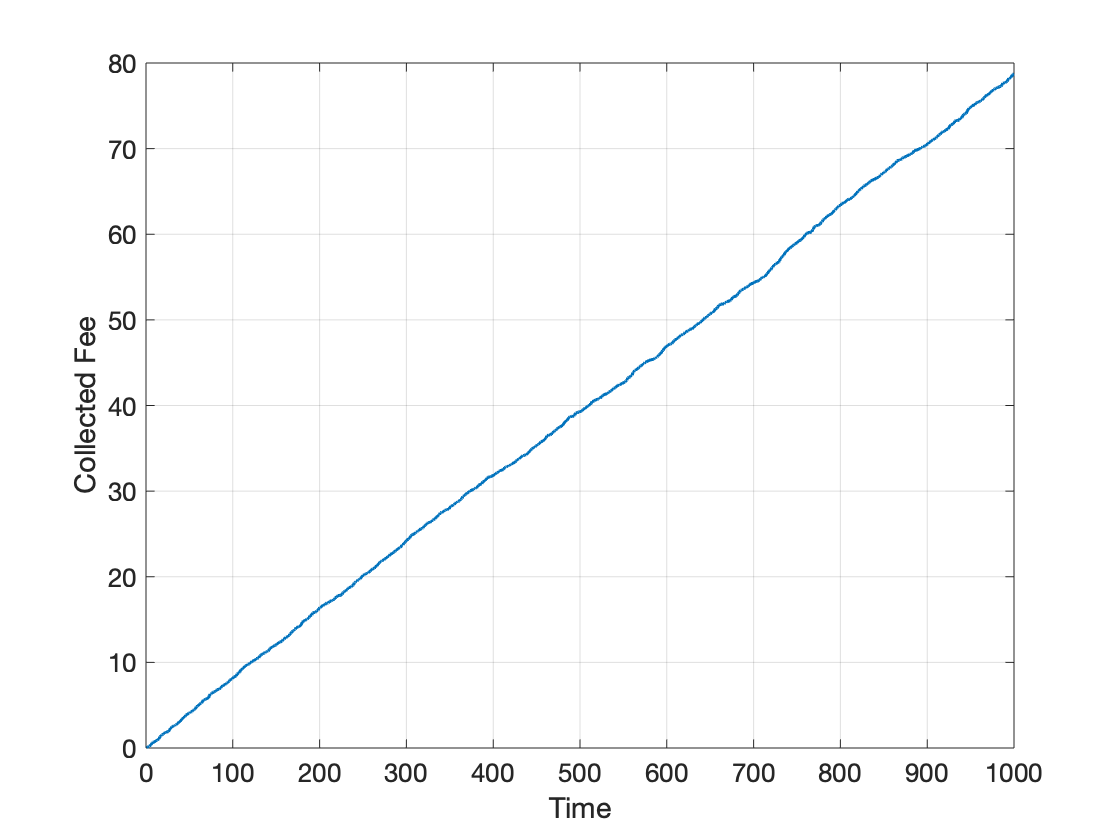

Simulations conducted to compare static and dynamic AMMs demonstrated the efficacy of dynamic curves in maintaining liquidity and value. In these simulations, two static AMMs (constant-sum and constant-product) and their dynamic counterparts were evaluated.

Findings include:

- Liquidity Maintenance: Dynamic AMMs consistently preserved a high percentage of initial tokens, highlighting their robustness against market volatility.

- Value Stability: Dynamic models showed minimal value fluctuation and lower total asset loss compared to static AMMs.

- Slippage and Fee Collection: Dynamic AMMs, while collecting fewer fees due to the absence of arbitrageurs, benefited from slippage gains, compensating for the fee deficit.

Figure 4: Simulation of a Dynamic Constant Sum AMM.

Figure 5: Simulation of a Dynamic Constant Product AMM.

Potential for Practical Implementation

The adoption of dynamic curves in real-world applications necessitates reliable market price oracles to ensure accurate and timely price adjustments. Such infrastructure would enable dynamic AMMs to achieve their potential in reducing arbitrage-induced losses and enhancing liquidity provisioning. Future work could focus on integrating these models within existing decentralized exchanges and empirically validating their performance in a live market environment.

Conclusion

The dynamic curve approach proposed in this paper offers a promising avenue for enhancing the functionality and robustness of decentralized cryptocurrency exchanges. By eliminating arbitrage opportunities and optimizing liquidity through real-time curve adjustments, this mechanism holds potential for greater economic efficiency and utility in decentralized finance. Real-world implementation of this model could significantly strengthen decentralized market infrastructures, fostering wider adoption and resilience in various trading conditions.