- The paper presents an algebraic framework that utilizes Dirac notation and creation/annihilation operators to model order book dynamics.

- The methodology involves a Markovian master equation and Gillespie algorithm simulations to capture stochastic order arrivals, cancellations, and market liquidity.

- The framework’s compositional nature allows analysis of diverse trading strategies and offers potential for future extensions in multi-asset market models.

An Algebraic Framework for the Modeling of Limit Order Books

This essay provides a technical summary of the paper "An Algebraic Framework for the Modeling of Limit Order Books", focusing on the proposed algebraic modeling framework for limit order books (LOBs) using tools from physics and stochastic processes. The paper highlights a novel approach to modeling complex financial systems, focusing on the dynamics of LOBs.

Introduction

The paper introduces a sophisticated algebraic framework for modeling LOBs by leveraging concepts from physics, particularly Dirac notation, and advanced stochastic processes. The presented approach addresses the intricacies of LOB dynamics by capturing critical actions such as order creation, annihilation, and matching, alongside the temporal evolution of LOB states. This algebraic representation facilitates simulations in diverse market scenarios and allows for the analysis of variations in trader behavior, influencing market observables like spread, return volatility, and liquidity. The framework's strength lies in its compositional nature, accommodating heterogeneous traders and multiple market structures.

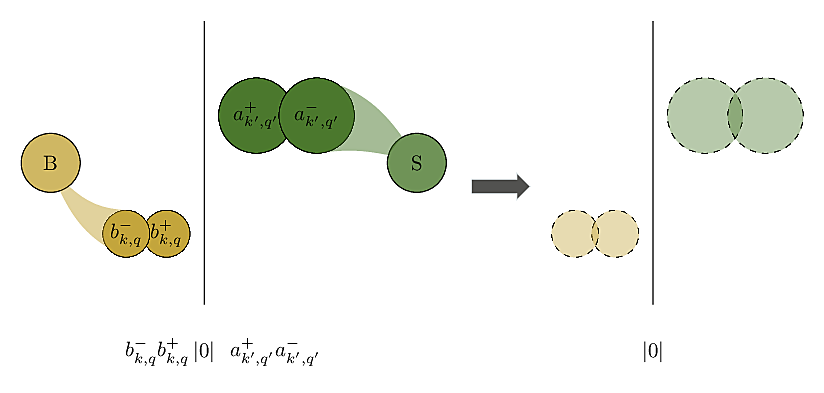

Figure 1: Overview on LOB states.

The Algebraic Design of Limit Order Books

Limit Order Book Structure

The LOB serves as a centralized venue where buy and sell orders are matched based on price and time priority. Orders submitted to the LOB include limit orders, which reside in the book until execution, and market orders, which execute immediately upon entering the book.

Algebraic Representation

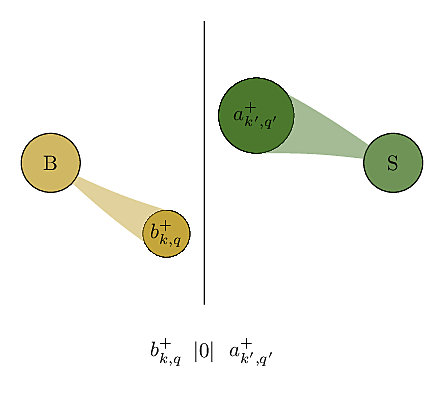

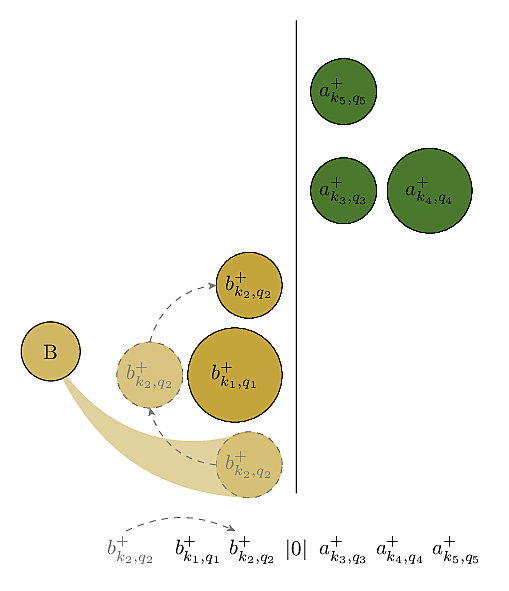

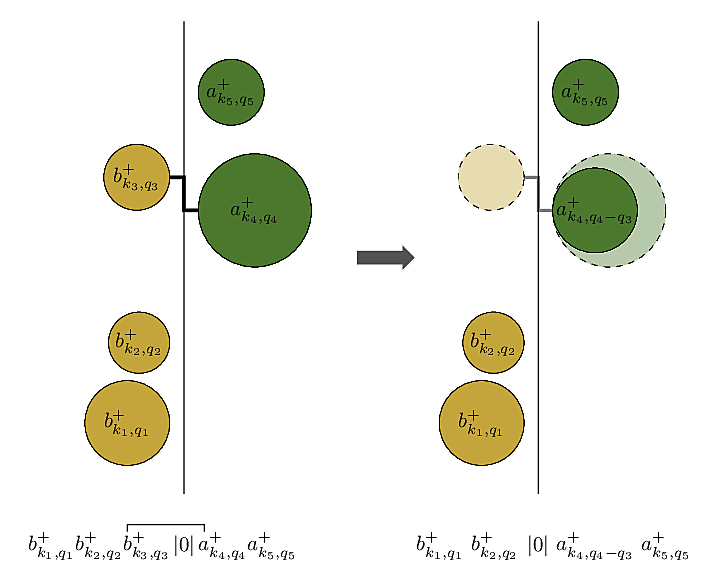

The paper uses Dirac notation to abstractly represent the state space and dynamics of LOBs. In this framework, operations such as order submission and cancellation are expressed through creation and annihilation operators. These operators act on an order book state with specific algebraic rules reflecting priority and matching procedures.

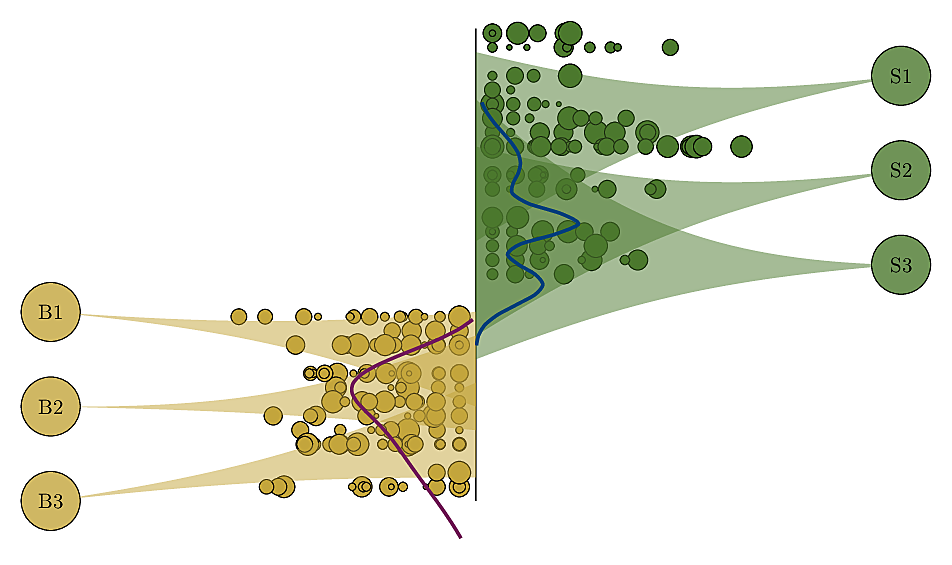

Figure 2: Rules of the Limit Order Book.

The algebraic model supports a comprehensive set of "pure" order book states, which can be combined into "mixed" states—linear combinations of pure states weighted by probabilities. This not only reflects the current configuration of the LOB but allows for modeling its probabilistic evolution over time.

Stochastic Time Evolution

Markovian Dynamics

The framework models the LOB dynamics as a continuous Markov process, outlined through a master equation that dictates the time evolution of the system. This Markovian formulation captures the probabilistic nature of order arrivals and cancellations, effectively modeling the stochastic variability within real-world order books.

The Role of Transition Rates

Transition rates, representing probabilities of order events, serve as critical parameters in capturing LOB dynamics. These rates can be fine-tuned based on empirical observations and adjusted to reflect heterogeneous trading behaviors.

Hamiltonian Operator

The Hamiltonian operator effectively encodes all possible transitions between order book states, enabling explicit modeling of market mechanics in equilibrium through the use of an effective Hamiltonian. This facilitates precise simulations of LOB behavior under varying market conditions.

Simulation and Scenario Analysis

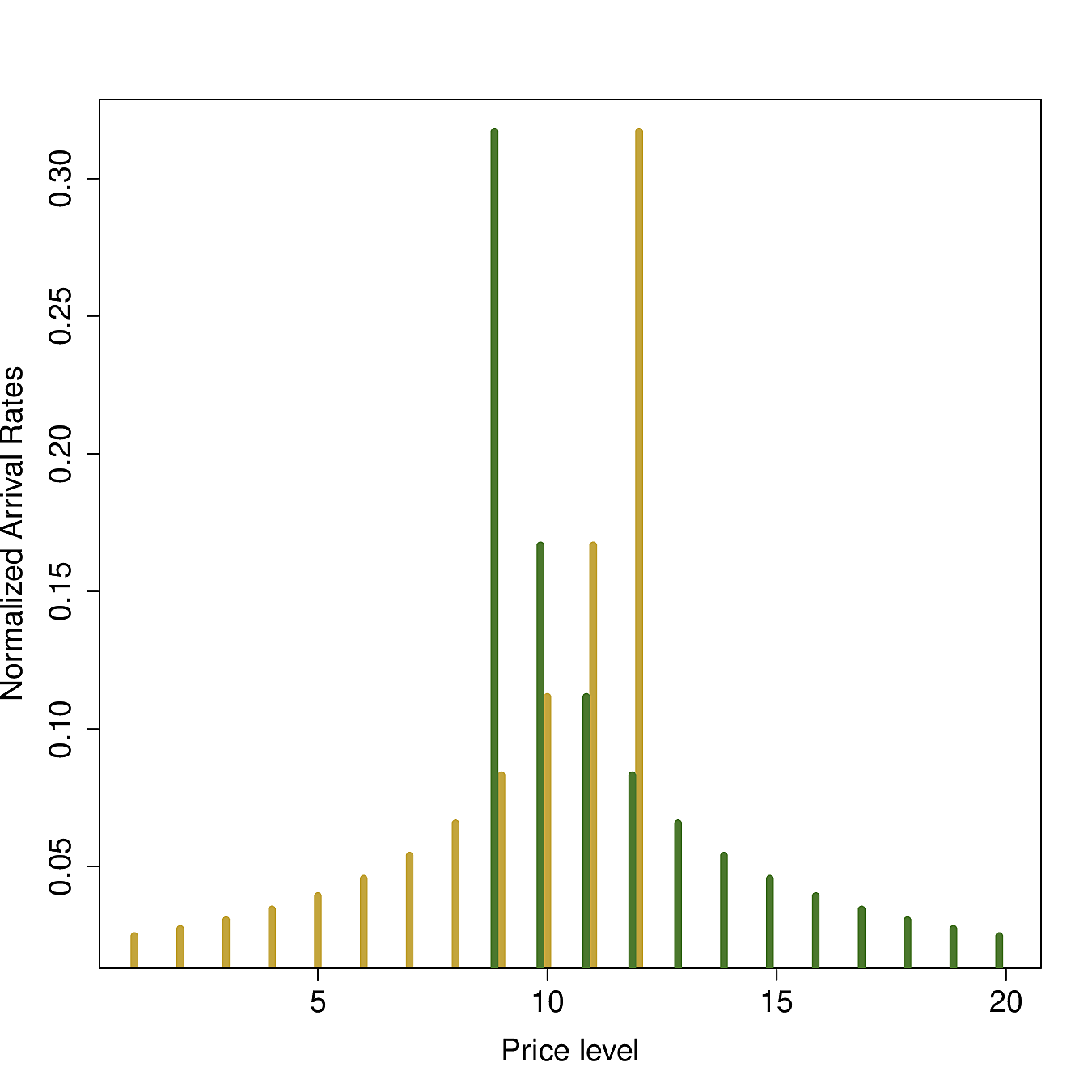

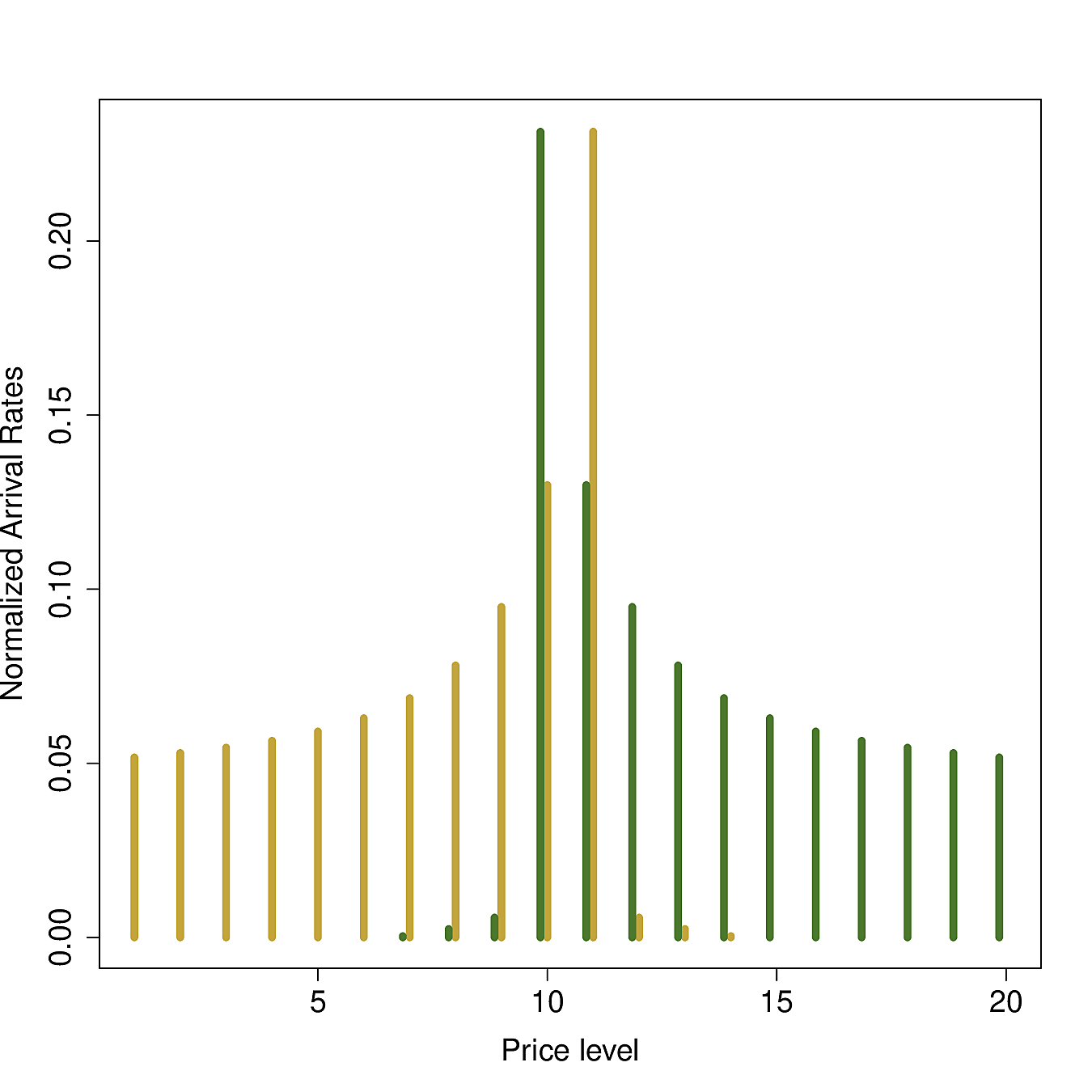

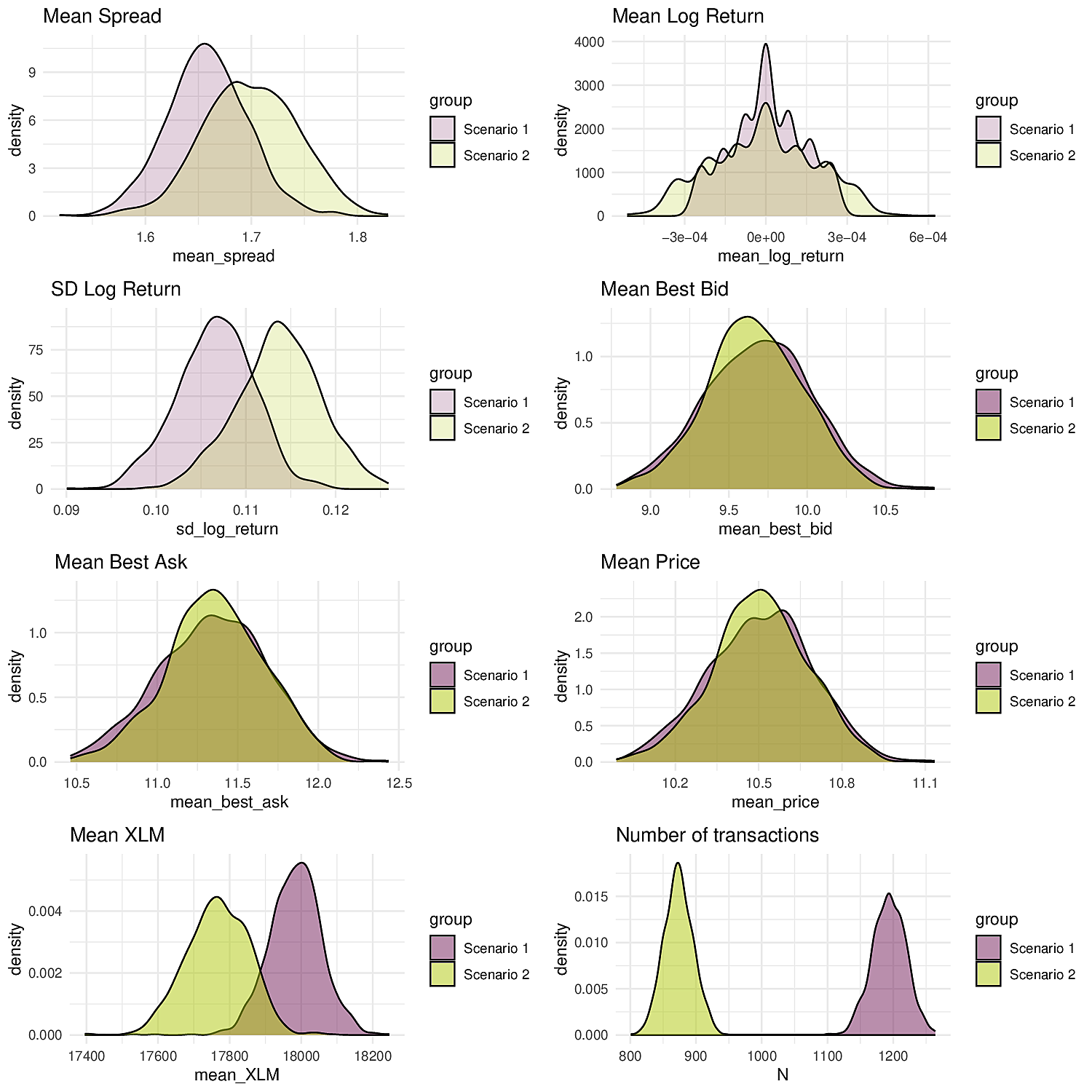

Simulations leverage the Gillespie algorithm, enabling exact generation of stochastic LOB dynamics over time. The paper demonstrates two scenarios with different trading strategies and analyzes their impact on key market observables such as spread, transaction rates, and liquidity.

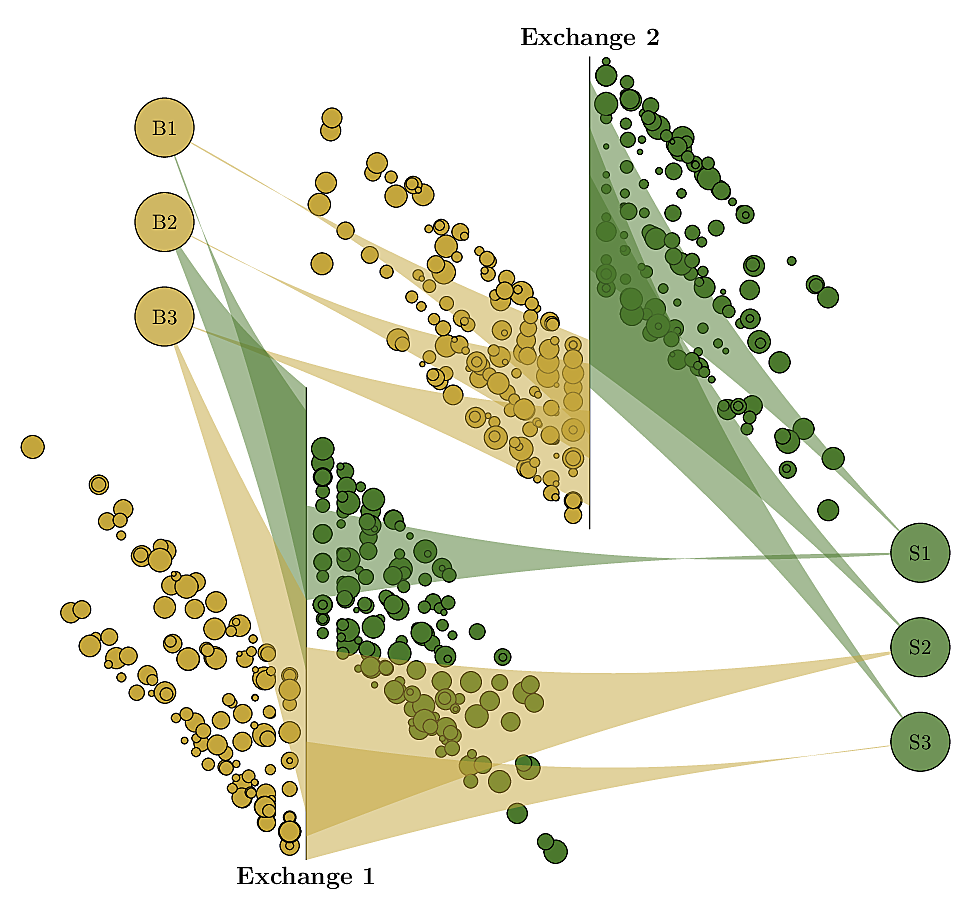

Figure 3: Arrival Rates.

Implications and Future Research

The algebraic framework presented in this paper offers a robust tool for dissecting the subtleties of market microstructure, providing insights into the impact of trading strategies and market regulations. Its extensibility promises future applications, including more sophisticated order types and multi-asset environments.

The framework's abstraction lends itself to possible expansions in incorporating adaptive event rates and complex trader interactions. This could further deepen the understanding of key market dynamics and ultimately guide the formulation of regulations and policies that maintain market integrity and efficiency.

In conclusion, the introduction of this algebraic framework for LOB modeling marks a significant advancement in the quantitative study of financial markets. Its ability to simulate and predict order flow dynamics has practical implications for traders, market makers, and policymakers aimed at optimizing market structure. Future work in this area is poised to refine and expand upon these capabilities, integrating them into broader market analysis and strategic decision-making processes.

Figure 4: Simulation Results: Key Observables.