- The paper introduces a hybrid VAR-FNN model that merges linear and non-linear techniques for enhanced OFI prediction in high-frequency trading.

- The VAR component captures interdependencies in buy/sell orders while the FNN models non-linear residuals to improve prediction accuracy.

- Empirical results indicate significantly lower MAE and MSE along with higher R² scores, validating the model's precision and effectiveness in trading intensity prediction.

Hybrid Vector Auto Regression and Neural Network Model for Order Flow Imbalance Prediction in High Frequency Trading

Introduction

This paper presents a hybrid modeling approach to predict Order Flow Imbalance (OFI) in high-frequency trading (HFT) environments. The model combines Vector Auto Regression (VAR) with a Feedforward Neural Network (FNN) to leverage both linear and non-linear dependencies. The VAR model captures the linear interdependencies between buy and sell orders, while the FNN models the non-linear residuals, offering a comprehensive framework for OFI prediction. Such predictions are critical in understanding market dynamics and devising effective trading strategies.

Methodology

VAR and FNN Architectures

The VAR component of the model captures linear dependencies among multiple time series variables. It is particularly effective in examining the mutual influences of buy and sell orders across different timeframes. Each variable in the system is predicted from its past values and those of others, drawing insights into market dynamics.

The FNN component captures the non-linear dependencies that the VAR model cannot address. The architecture consists of input layers corresponding to the residuals from the VAR model and multiple hidden layers that learn complex patterns via adjustable weights and non-linear activation functions. This design enhances the model's flexibility in adapting to diverse market conditions.

Figure 1: Basic architecture of a feedforward neural network (FNN) for financial prediction.

Hybrid Model Implementation

The hybrid model first utilizes VAR to forecast future buy and sell orders and computes OFI from these forecasts. The residuals, which highlight discrepancies between actual orders and VAR predictions, are fed into the FNN. Training the FNN on these residuals allows the model to learn the non-linear aspects, improving overall prediction accuracy.

Evaluation and Results

Data and Experimental Setup

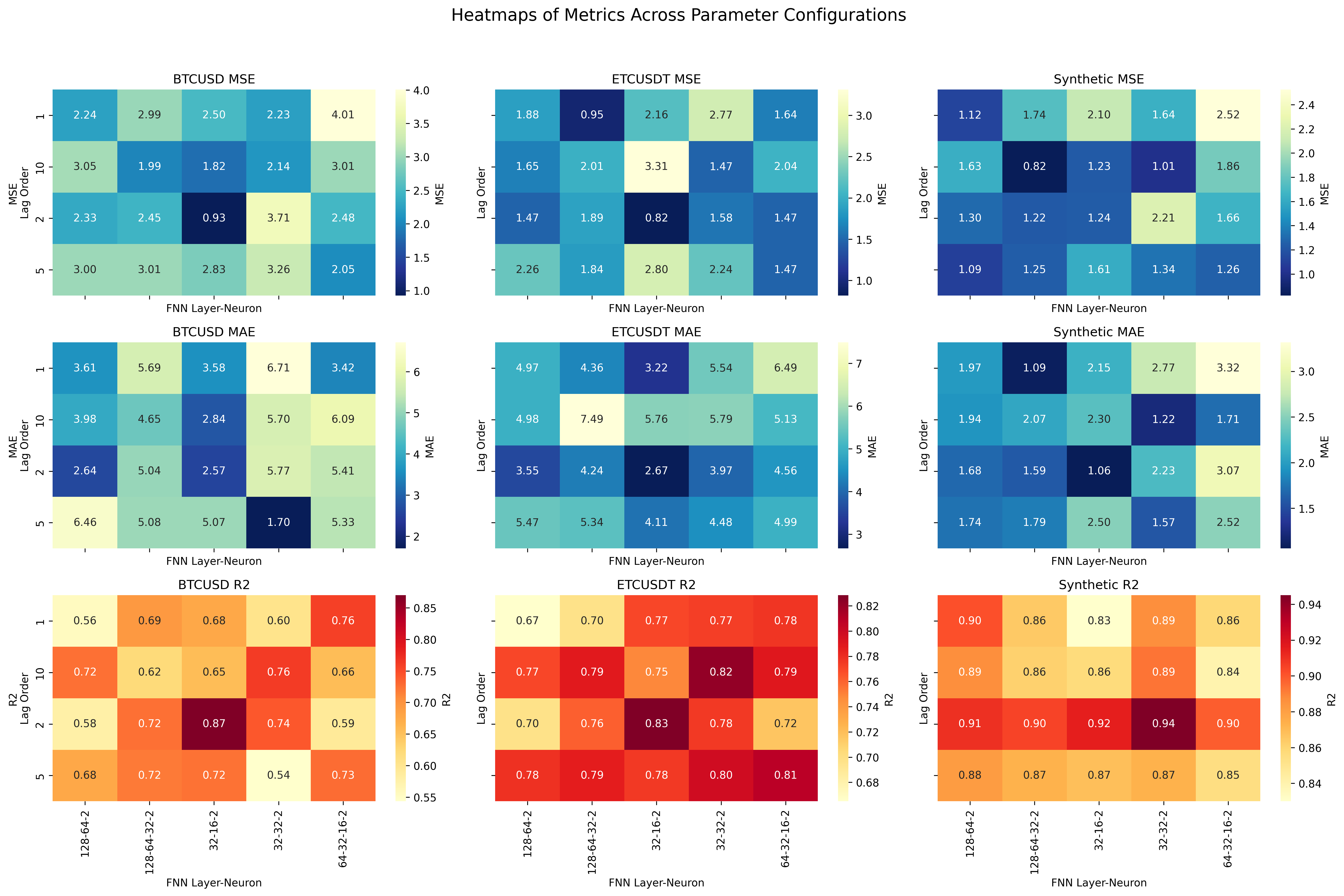

The model was trained using high-frequency trading data from Binance, employing datasets of buy and sell orders for cryptocurrencies like BTCUSD and ETHUSDT, as well as synthetic datasets to ensure robustness. Various parameters, such as lag orders in the VAR model and FNN architecture configurations, were optimized through a comprehensive sensitivity analysis.

Figure 2: Sensitivity Analysis Heatmaps: Evaluation Metrics Across Parameter Configurations

The hybrid model consistently outperformed standalone VAR and FNN models. Key evaluation metrics included Mean Absolute Error (MAE), Mean Squared Error (MSE), and R2. The hybrid approach exhibited significantly lower MSE and MAE values and higher R2 scores, indicating better predictive accuracy and generalization capability.

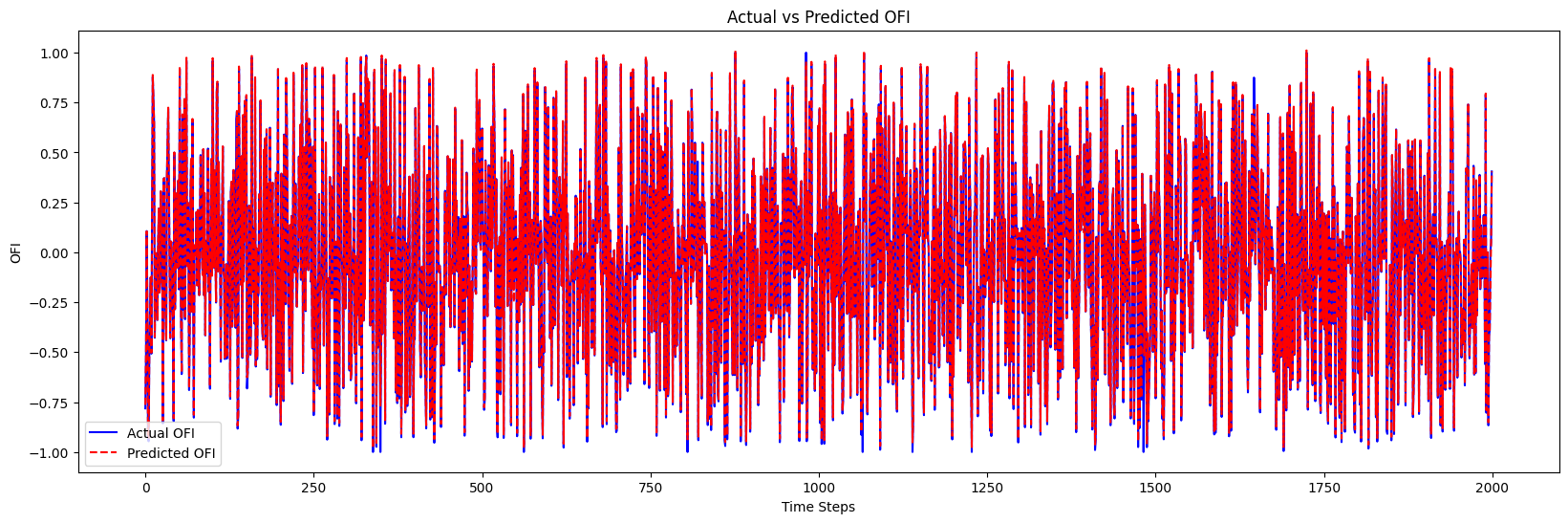

Figure 3: Predictions from the Hybrid VAR-FNN Model during Training.

Trading Intensity Prediction

The intensity metric, representing the magnitude of trading pressure on the buy or sell side, was a notable addition. The hybrid model demonstrated high accuracy and precision in predicting trading intensity signals, crucial for effective strategy formulation in trading environments.

Discussion

Implications and Future Developments

The hybrid VAR-FNN model effectively integrates the strengths of econometric time series models and machine learning, providing a robust tool for OFI prediction. Its application extends beyond HFT, offering potential benefits for liquidity management and optimal trade execution.

The model's advancement lies in its adaptability to different asset classes and market conditions. Future research could explore enhancements such as integrating Long Short-Term Memory (LSTM) networks to capture temporal dynamics more effectively, or extending the model's application to equities and forex markets.

Conclusion

This study introduces a hybrid VAR-FNN model that demonstrates superior predictive capabilities for OFI in high-frequency trading contexts. By combining the interpretability of traditional statistical models with the adaptability of neural networks, the approach delivers a balanced solution to forecasting challenges in volatile markets. The model's ability to accurately predict OFI and trading signals suggests it could serve as a valuable tool for traders and financial analysts, enhancing the precision of trading strategies and contributing to informed decision-making processes in financial markets.