- The paper introduces a quasi-likelihood-based EM algorithm that effectively estimates parameters in regime-switching SDEs with latent Markov states.

- It employs a Cauchy density approximation to simplify the complex NIG noise modeling, significantly enhancing computational efficiency.

- Simulation studies validate the algorithm's accuracy in capturing both drift coefficients and regime transitions under varied time schemes.

Quasi-likelihood-based EM Algorithm for Regime-Switching SDE

Introduction

The paper "Quasi-likelihood-based EM algorithm for regime-switching SDE" discusses an Expectation-Maximization (EM) approach for parameter estimation in regime-switching stochastic differential equations (SDEs) driven by Normal Inverse Gaussian (NIG) noise. This approach is particularly suitable for modeling systems where continuous dynamics interact with discrete-state transitions, such as those in financial markets, ecology, and engineering. By incorporating a continuous-time finite state Markov chain to capture regime changes, the model offers a more realistic representation of evolving conditions.

Quasi-likelihood Approach

The paper introduces a quasi-likelihood approach tailored for Normal Inverse Gaussian (NIG) L{é}vy processes in the context of regime-switching SDEs. Given the complexity introduced by the hidden nature of the Markov chain, the authors propose leveraging a Cauchy quasi-likelihood approximation. This is based on the asymptotic distribution of the NIG L{é}vy process for small time steps, thus facilitating parameter estimation even when the Markov chain states are unobserved.

The usual Bessel function complexity in the NIG density computation is avoided by approximating it with a standard Cauchy density, a significant simplification when dealing with high-frequency data scenarios.

EM Algorithm for Switching SDE

Methodology

The paper details an EM algorithm that iteratively updates parameter estimates in the presence of latent variables. The algorithm's main components include:

- E-step (Expectation): Calculation of the expected log-likelihood function using current estimates.

- M-step (Maximization): Optimization of the parameters that maximize the expected log-likelihood from the E-step.

For improved computational feasibility, the EM algorithm is applied in tandem with the Cauchy quasi-likelihood approach, giving rise to a finite-sample likelihood approximation suitable for high-frequency sampled data.

Computational Strategy

The algorithm is implemented with careful handling of conditional probabilities associated with the Markov chain's hidden regimes. A numerical approach is employed to estimate these probabilities, enabling the calculation of parameter updates iteratively until convergence criteria are met.

Simulation Studies

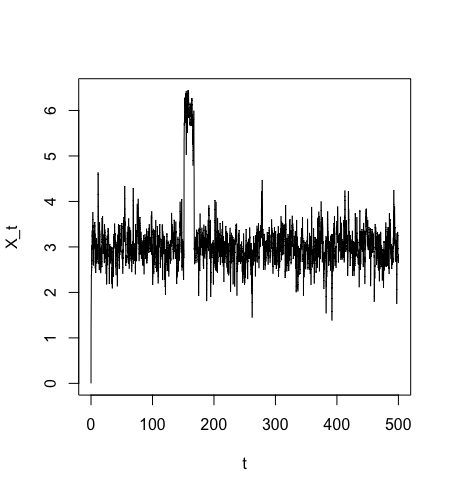

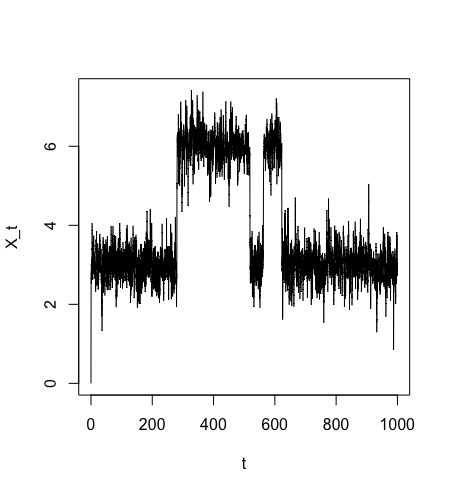

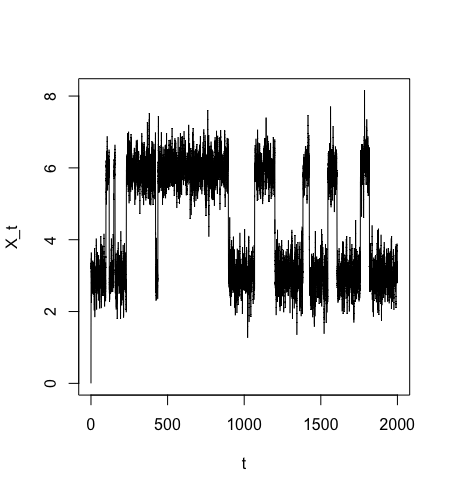

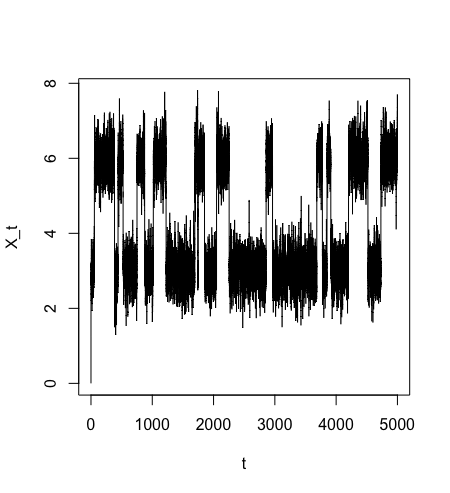

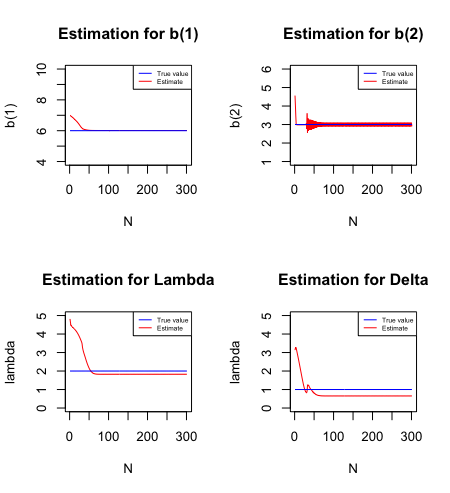

The simulation results presented in the paper validate the EM algorithm's efficacy, showing accurate parameter estimation for the regime-switching SDE model. The findings underscore the algorithm's robustness against different time schemes and its ability to handle the non-observable states of the Markov chain.

Sample paths are generated using an Euler approximation, and the algorithm is tested under various terminal times and step sizes. The results demonstrate that the estimates, particularly for parameters directly tied to the Markov chain, such as the drift coefficients, achieve high accuracy across all configurations, while the noise parameter estimates remain slightly less precise.

Figure 1: Sample path with T=500, h=0.1.

Figure 2: Iteration with T=500, h=0.1, ϵ=0.02. The blue line represents the true parameter value, and the red line represents the estimated value.

Conclusion

The developed algorithm provides a comprehensive tool for parameter estimation in regime-switching SDEs driven by NIG noise. With its unique combination of the EM algorithm and quasi-likelihood approximation, it enables effective handling of latent variables and offers a pathway for further application in fields requiring precise modeling of complex dynamic systems. Future research directions may include extending the method to other types of L{é}vy processes and addressing the estimation of transition intensities in the Markov chain, potentially incorporating additional computational techniques to enhance precision and efficiency.