- The paper demonstrates that market impact follows a double square-root law, with immediate and temporal effects scaling with the square root of traded volume.

- It employs a granular dataset with trader IDs to dissect metaorders into child orders, providing precise empirical evidence that contests traditional linear liquidity models.

- The findings suggest a mechanical origin for market impact, challenging information-driven theories and offering insights for developing adaptive trading strategies.

The "Double" Square-Root Law: Mechanical Origins of Market Impact Utilizing Tokyo Stock Exchange Data

Introduction

This essay encapsulates the findings of "The 'double' square-root law: Evidence for the mechanical origin of market impact using Tokyo Stock Exchange data" in which the authors explore the origins of market impact using an ID-resolved dataset from the Tokyo Stock Exchange (TSE). The study reveals the mechanical roots of the square-root law for market impact, challenging the conventional information-driven theories.

Square-Root Law in Market Impact

Fundamentally, the paper addresses the square-root law, which posits that the average price impact of a metaorder is proportional to the square root of the traded volume relative to daily volume. The well-documented square-root impact regime deviates from classical economic models like Kyle’s model, which predict a linear relationship, thus questioning the liquidity assumptions made in such models. Canonical examples include the linear model’s failure to describe liquidity deficits for small trade volumes accurately.

Detailed Data Analysis

The research utilizes a comprehensive dataset from the TSE, unique for its inclusion of trader IDs. This dataset allows the authors to define metaorders meticulously and to examine the microscopic origins of the square-root law. The dataset’s granularity permits a meticulous disaggregation of trades into child orders and examination of the impact these orders have both individually and collectively.

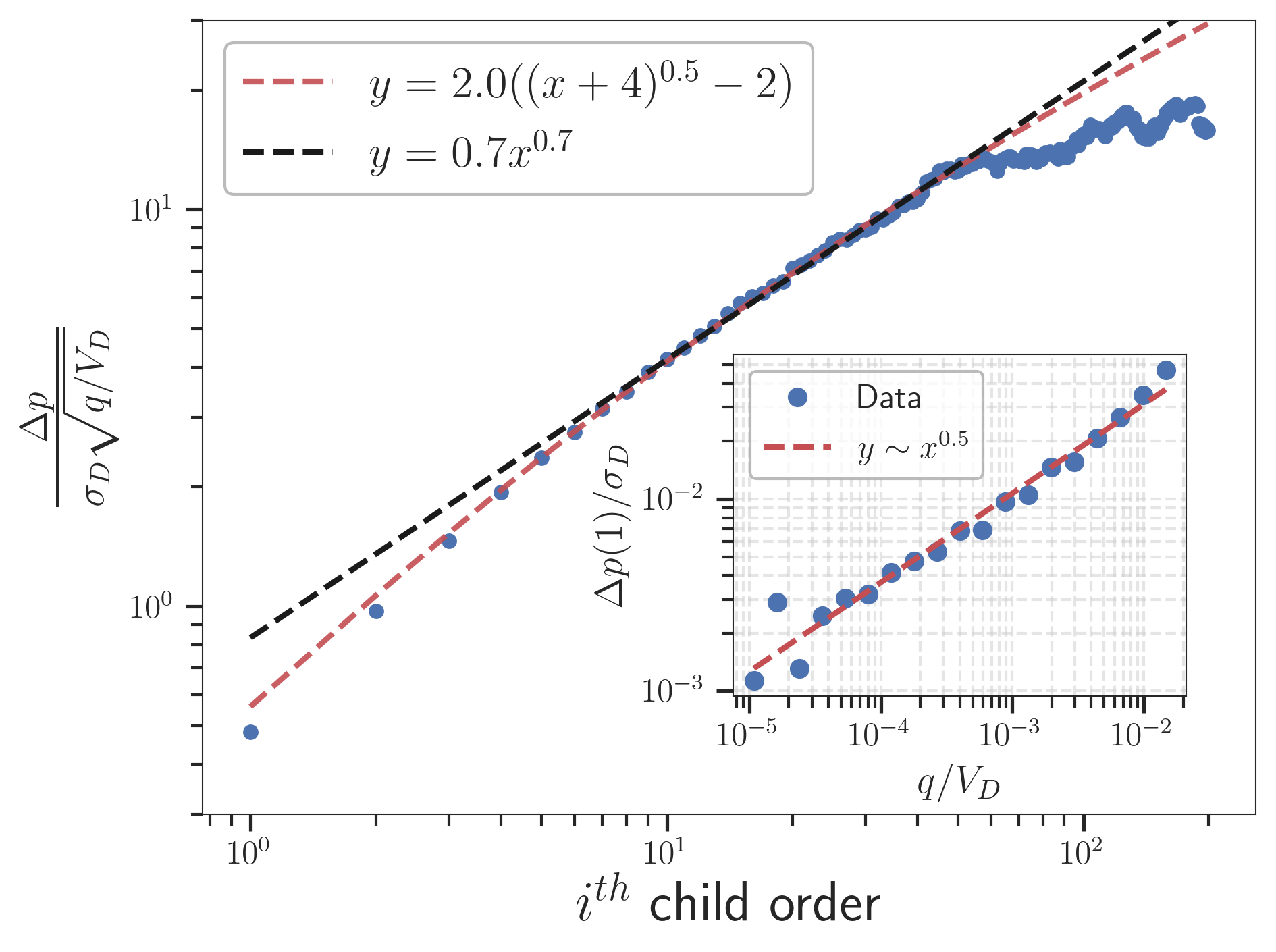

Empirical Evidence of the Double Square-Root Law

The paper’s cornerstone is the demonstration of a "double" square-root effect. Precisely, it reveals two emergent phenomena: the immediate impact of child orders correlating with the square root of their volume and a temporal inverse square-root relaxation subsequent to the child orders' execution.

Figure 1: Average price profile during the execution of a metaorder, illustrating the cumulative and relaxed impact behavior consistent with the double square-root law.

Surprisingly, the profound results show that the square-root impact law persists at the granularity of individual market orders. Notably, these results underline that the impact of single market orders follows a square-root function of volume when accounted for over time, a finding confirmed even after shuffling trader IDs, thereby nullifying individual trading strategy influence.

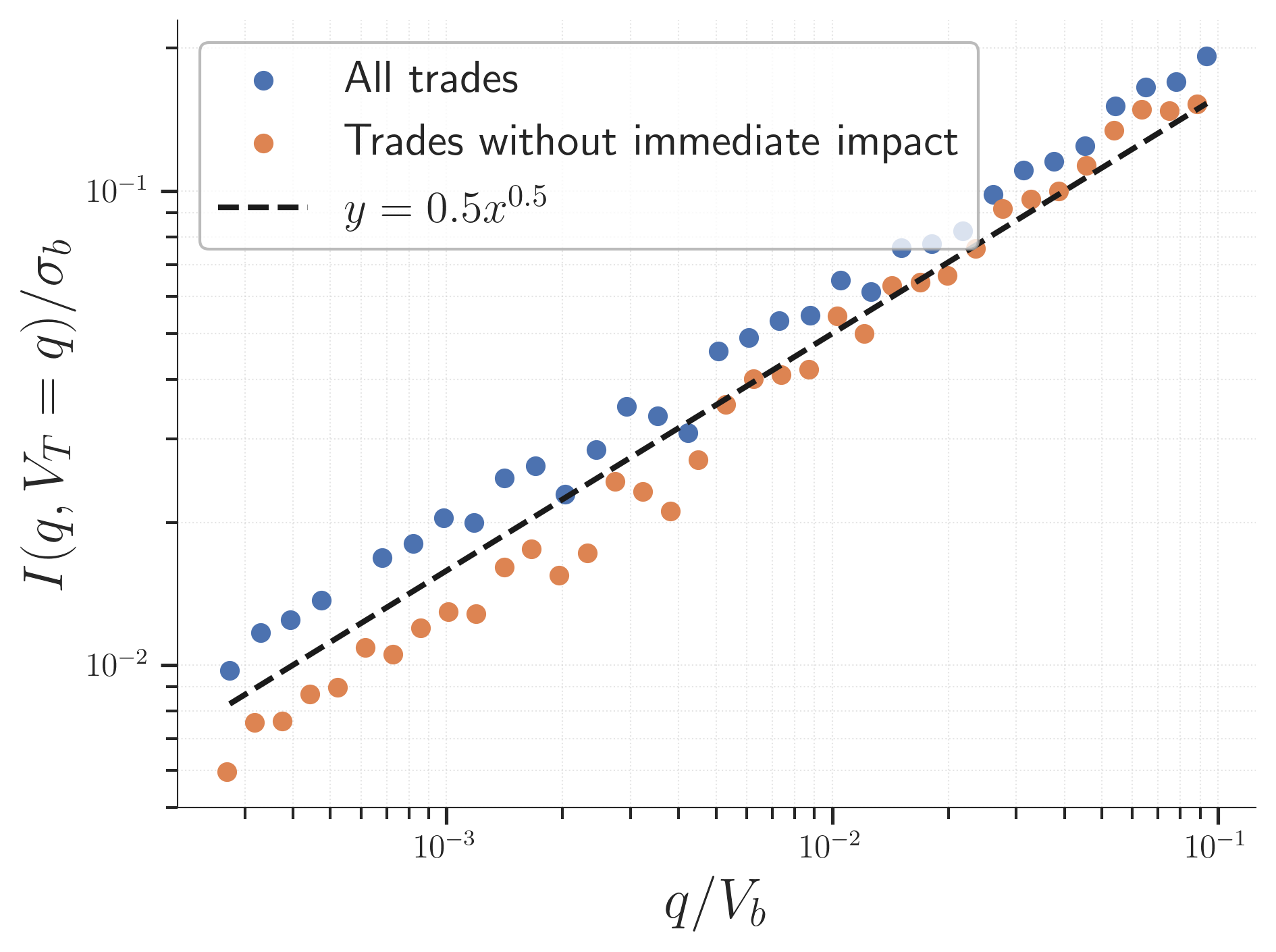

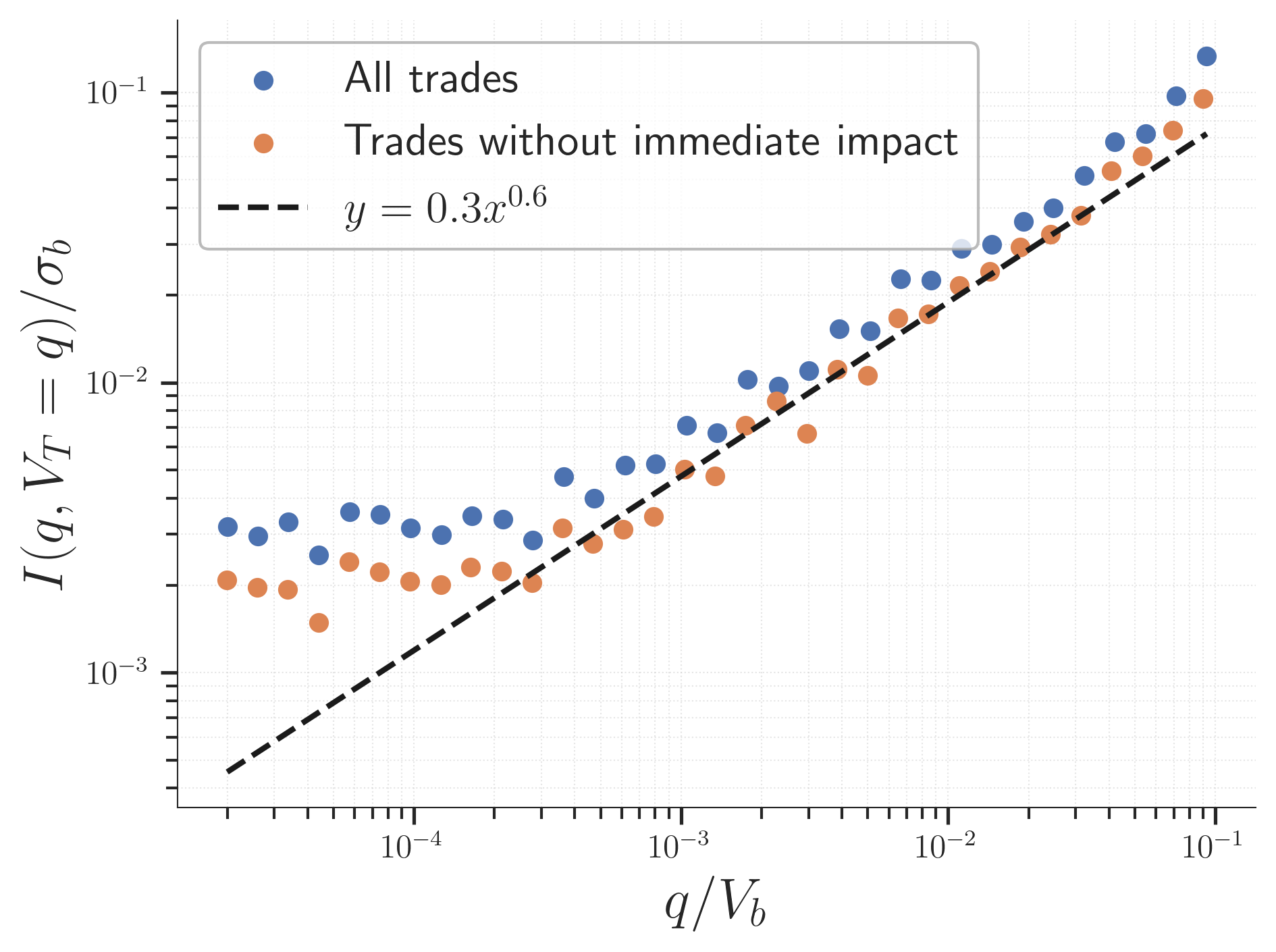

Mechanical Character of Market Impact

The authors argue for a "mechanical" interpretation of market impact by demonstrating that market orders—once processed by the market makers—result in a latent liquidity landscape that aligns with theoretical linear order book models. Herein lies the insight: once an order is processed, the liquidity finds an equilibrium, implying that individual market orders exhibit consistent impact profiles regardless of the originating trading strategy, be it informed or not.

Figure 2: Impact of public market orders illustrating consistent square-root behavior over volume time equal to order size.

Implications and Future Directions

These findings challenge information-centric theories of market impact and strongly support the idea of a mechanically-driven impact process. This mechanical interpretation could lead to novel perspectives in reinterpreting market liquidity models and might serve as a springboard for adaptive trading strategies that minimize market impact in operational execution.

Additionally, this methodology paves the way for future exploration of synthetic metaorders constructed from public tape alone, potentially broadening empirical research avenues in financial markets.

Conclusion

The research delivers compelling evidence in favor of a mechanical origin for the square-root law of price impact. By dissecting the market impact across both macro and micro scales, the study provides foundational insights into liquidity dynamics, urging a re-evaluation of traditional economic interpretations of market behavior. The findings reassure that the understanding of market mechanics could benefit from an emphasis on market structure and liquidity processes rather than solely the informational aspects of trading strategies.