- The paper develops a risk-averse trader model with a non-linear pricing rule to show manipulation impacts short- and long-term price dynamics.

- The experimental study on 817 markets demonstrates that induced price shocks persist up to 60 days, with significant partial reversion occurring mostly in the first week.

- The research highlights that high trader activity and external information sources enhance market resistance to manipulation.

How Manipulable Are Prediction Markets?

Introduction

Prediction markets, where participants bet on the outcomes of real-world events, serve as robust platforms for aggregating diverse information. These markets often rival or surpass traditional forecasting methods. However, concerns about their susceptibility to manipulation persist. The paper, "How Manipulable Are Prediction Markets?", addresses this by presenting both theoretical models and experimental data to explore the manipulability of these markets.

Theoretical Framework

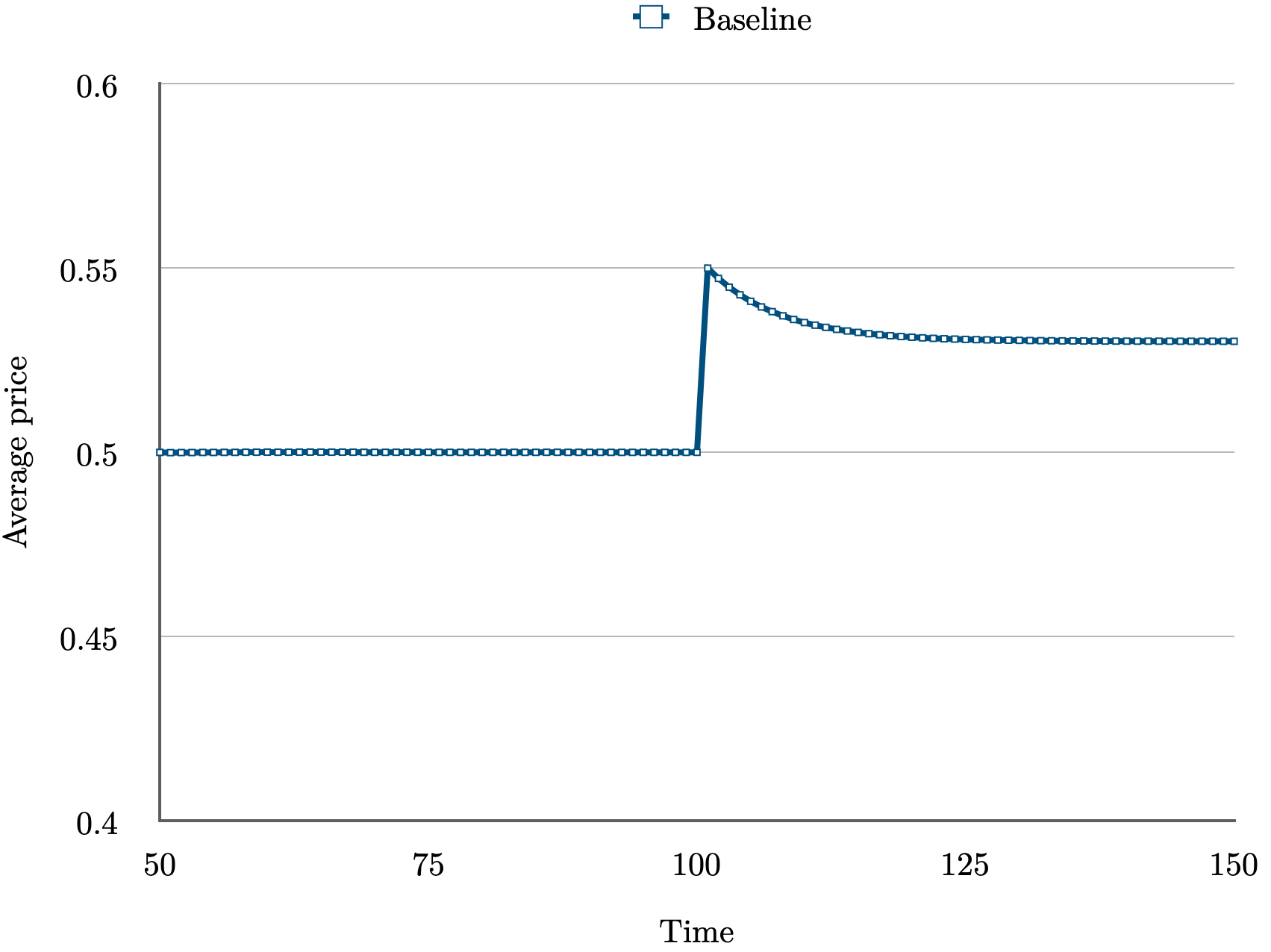

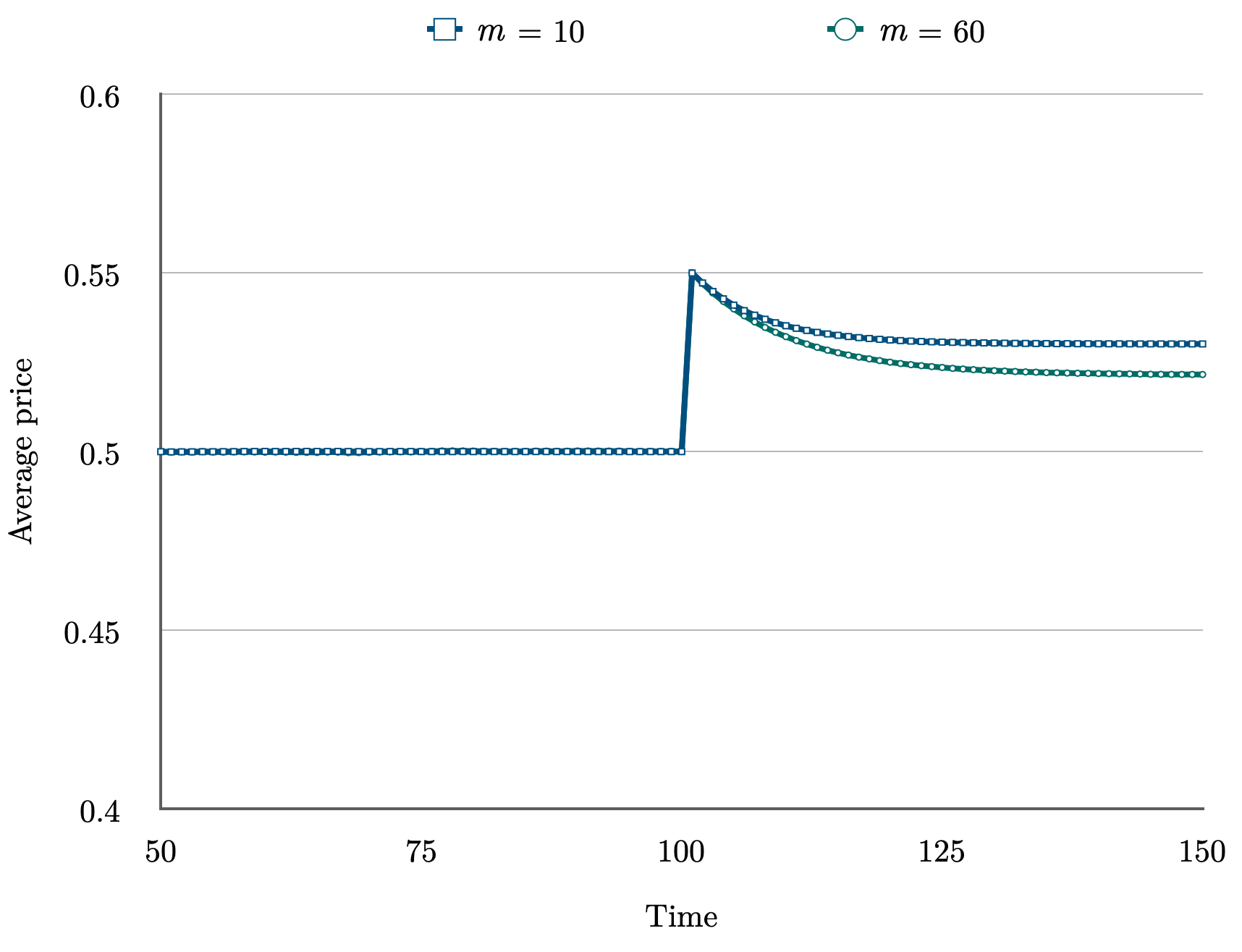

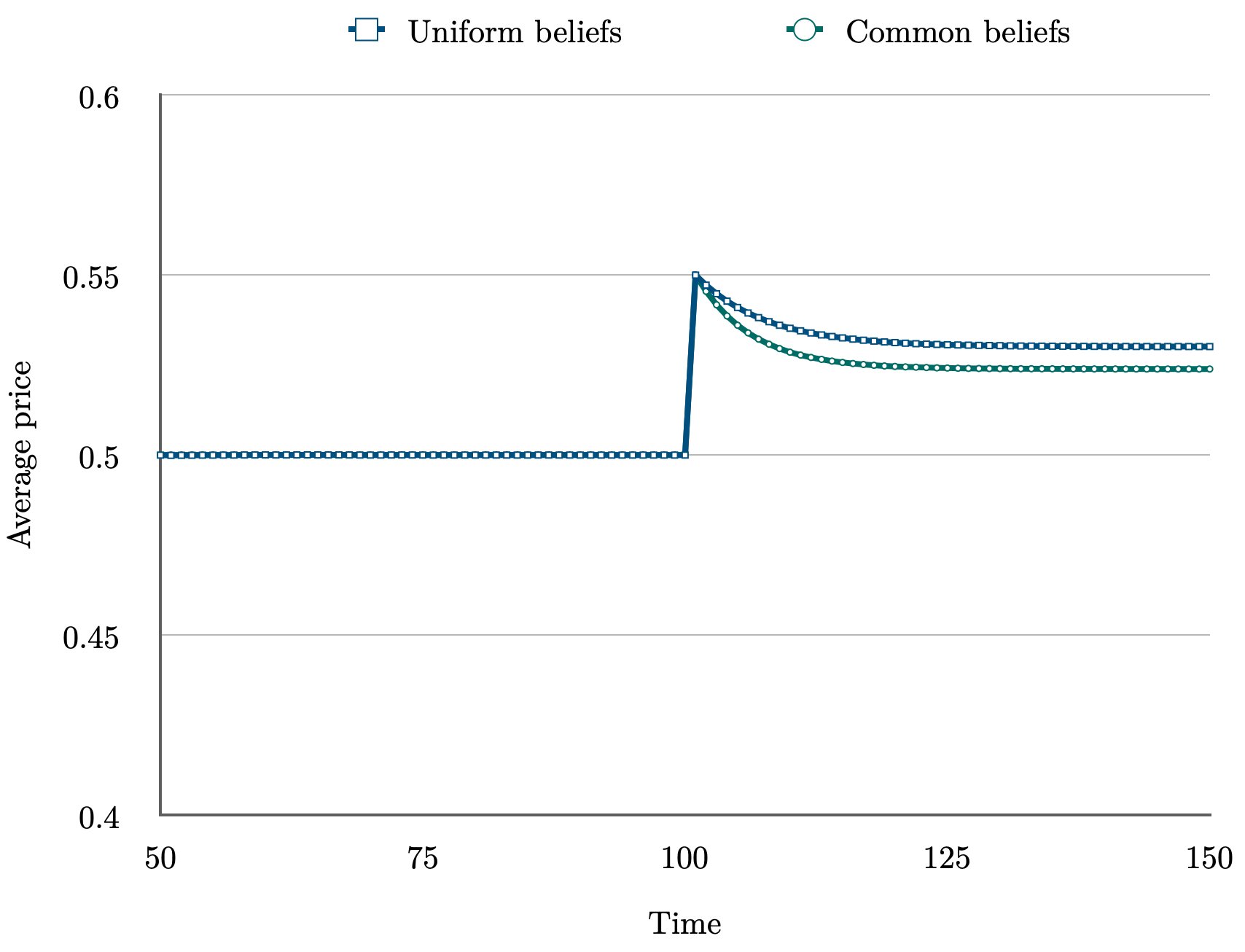

The authors develop a model where traders are risk-averse, choosing bets based on their subjective probabilities of event outcomes. Key innovations of this model include the use of a non-linear pricing rule (constant product rule) as opposed to assuming competitive equilibrium, allowing the examination of price behavior following manipulative trades.

Key Predictions of the Model:

- Manipulation affects prices in both short and long terms, due to initial behavioral adjustments and learning effects from market participants.

- Future trades partially correct manipulation, leading to price reversion towards initial values.

- The extent of reversion is contingent on market characteristics, such as the number of traders and the availability of external information sources.

Figure 1: Price adjustment under different market conditions.

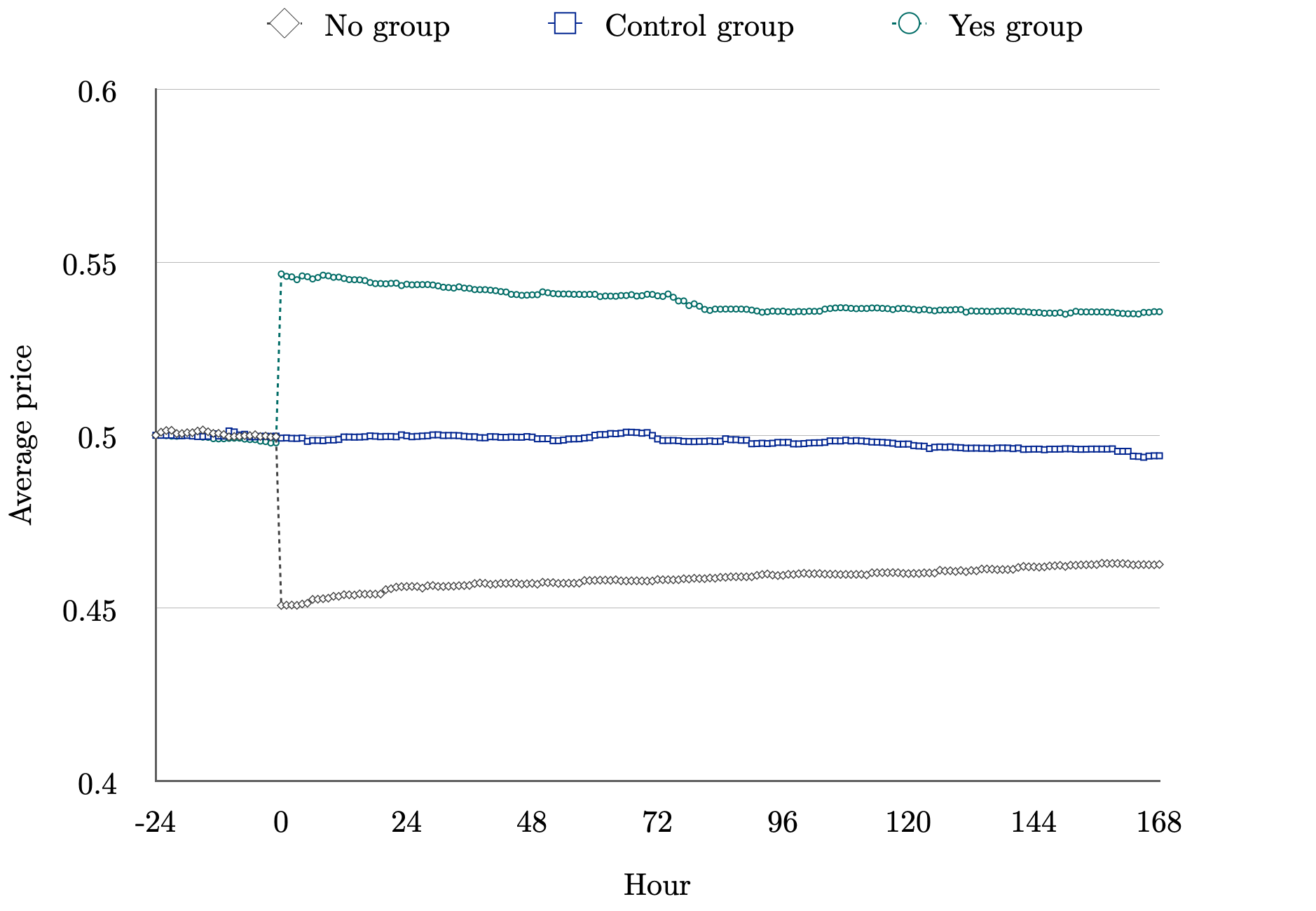

Experimental Design

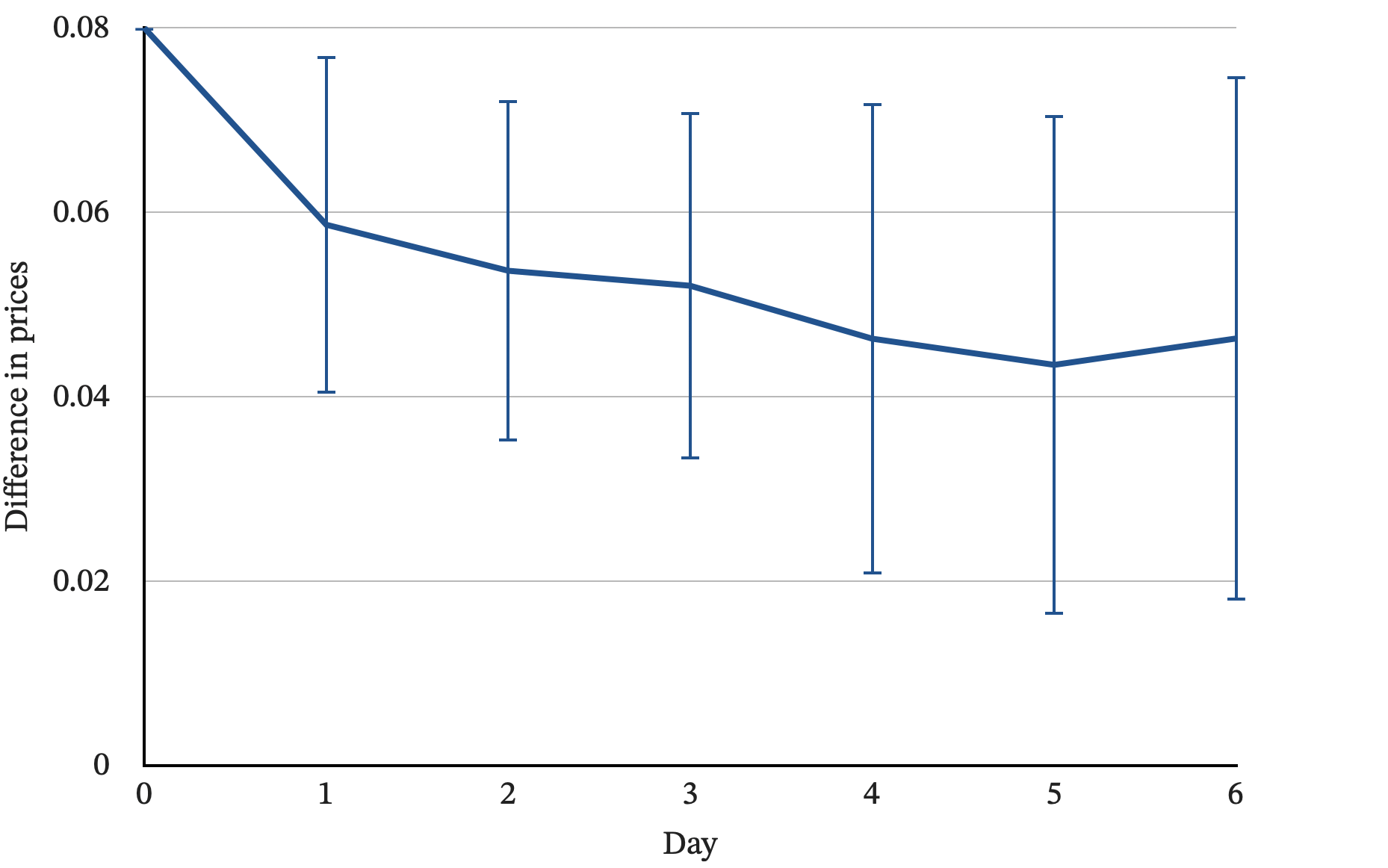

The study undertook a large-scale field experiment on the Manifold Markets platform, involving 817 distinct prediction markets. By inducing random price shocks (manipulations) and tracking price changes over a 60-day period, the study provided empirical evidence on the persistence of manipulation effects.

Figure 2: Average prices over time.

Experimental Findings:

- Persistence: Manipulative price shifts were detectable even 60 days post-intervention, indicating significant persistence of manipulation effects.

- Reversion: As anticipated by the model, partial price reversion occurred, primarily within the first week after manipulation.

- Market Characteristics: Markets with more traders, higher activity, and external information sources (e.g., duplicated questions on Metaculus) exhibited greater resistance to manipulation.

Robustness and Extensions

The study extensively tested for robustness, including analyses controlling for potential cross-market spillovers and re-evaluating the presence of such effects in a broader context. Additional experiments involving Sweepcash markets (a variant of existing markets with direct monetary incentives) corroborated initial findings, suggesting the robustness of observed manipulation dynamics irrespective of the type of incentive structure.

Figure 3: Results for the Sweepcash markets (β^1 estimates).

Implications and Future Directions

The study challenges the view that prediction market manipulations are ephemeral, presenting substantial evidence of both continued manipulability and systematic reversion influenced by market-specific factors. This insight suggests a need for:

- Enhanced design features to mitigate manipulative vulnerabilities.

- Further exploration of optimal manipulation strategies, considering tradeoff dynamics between shock size and long-term price influence.

Potential Extensions:

- Investigating non-trading manipulative strategies such as targeted information dissemination ("buzz").

- Evaluating the role of varying market incentives in influencing manipulation dynamics.

Conclusion

This research underscores the complex interplay between market manipulation and intrinsic market mechanics, highlighting both theoretical and empirical dimensions. By illuminating the conditions under which prediction markets are resilient to manipulation, the study provides a foundation for enhancing market structures and designing more robust information aggregation systems.