- The paper proposes a quantitative framework that augments the Vasicek model with jump processes to capture climate-driven asset devaluation.

- It calibrates model inputs using geographic vulnerability and balance sheet data to cluster firms by climate risk exposure.

- The approach quantifies risk metrics like VaR, revealing significant stress impacts, including an 86% increase in VaR for utilities under stress scenarios.

Physical Climate Risk in Asset Management

Introduction to Physical Climate Risk in Asset Management

The paper "Physical Climate Risk in Asset Management" develops a quantitative framework for assessing climate-related risks in asset management, particularly focusing on physical risks such as extreme weather events. The authors propose a model rooted in the Vasicek model, incorporating downward jumps to capture the disruptive impact of climate events on asset values. This technique aligns financial valuation with the reality of increased climate volatility, reflecting losses due to climate impacts on firm value.

Methodology and Model Description

The proposed model augments the multivariate Vasicek framework by integrating jump processes. Specifically, it models a firm's asset value with a geometric Brownian motion, altered by a Compound Poisson process representing climate-induced losses. Each firm's climate risk is determined by its geographical exposure and asset intensity, which serve as clustering parameters:

V~j(t)=Vj(0)e(rj−2σj2−2ωj2)t+σjWjt+ωjZt+Lk(t)

where Lk(t) symbolizes negative jumps in asset value due to climate risks for firms within a specified cluster.

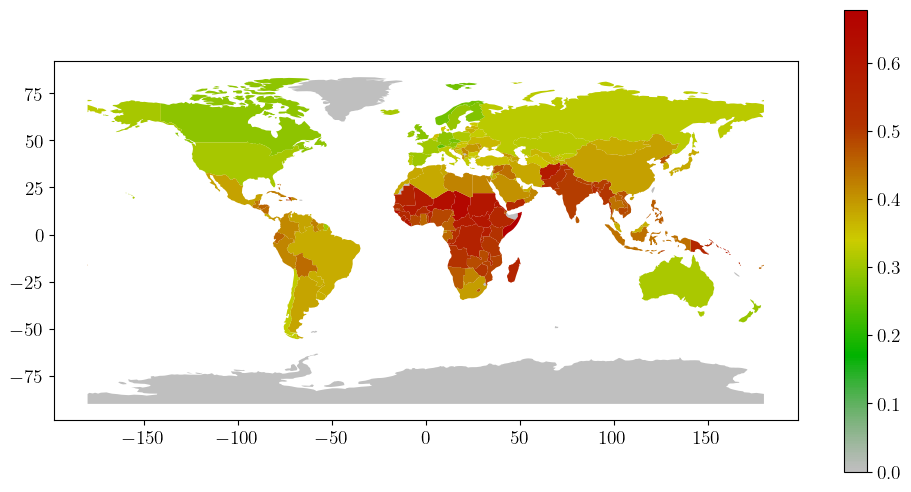

Figure 1: A representation of vulnerability scores across countries worldwide, reflecting their susceptibility to climate-related risks.

Implementation and Calibration

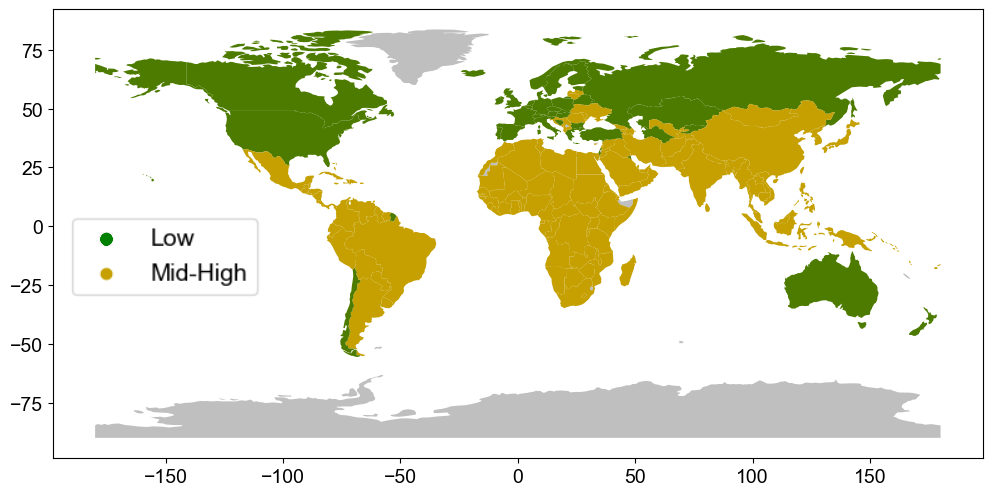

The framework leverages widely available datasets, such as the ND-GAIN Country Index to estimate geographic vulnerability and balance sheet data to determine asset intensity. Firms are clustered into categories based on their vulnerability to climate change and asset intensity, leading to more precise loss modeling. Firms in clusters with greater vulnerability and asset intensity face higher risk of asset devaluation.

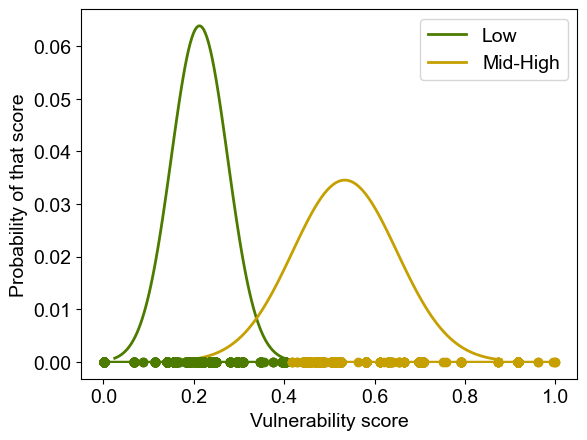

Figure 2: Estimated distributions of the vulnerability scores in the Low (green line) and Mid-High (orange line) clusters.

Applications and Risk Assessment

The model enables calculation of critical risk metrics, notably Value-at-Risk (VaR), adjusted for climate stress scenarios. By comparing a baseline scenario with a stressed scenario, the framework quantifies the potential financial impact of climate risks. The model's adaptability makes it instrumental for asset managers aiming to integrate climate risks into risk management, promoting informed decision-making regarding capital reserves and investment portfolios.

Figure 3: Vulnerability score clustering on the world map: Low Risk (Green) and Mid-High Risk (Orange).

Evaluation and Findings

Empirical evaluations using simulated portfolios demonstrate significant variations in expected loss and VaR between baseline and climate-stressed scenarios. For instance, the utilities sector, highly exposed to physical infrastructure damages, shows an 86% increase in VaR under stress scenarios. These evaluations underscore the need for robust climate risk assessment mechanisms in asset management.

Figure 4: Comparison over Time of VaR for the MSCI Europe Utilities index.

Conclusion

The proposed framework provides a meticulous approach to quantifying physical climate risks in asset management, integrating advanced stochastic processes to mirror climate-induced volatility. It offers a scalable and actionable methodology for financial institutions to assess and mitigate climate-related financial risks. This contribution is significant for regulatory compliance and developing strategic insights into climate risks within investment portfolios. Future research could explore enhancing the granularity of geographic exposure data and applying alternative stochastic processes to better capture the dynamic nature of climate phenomena.

Implications and Future Directions

The implementation of such a model in practice facilitates compliance with evolving regulatory requirements and improves the resilience of financial systems against climate change impacts. Future extensions could involve developing more sophisticated jump processes or incorporating real-time climate change projections to further refine risk assessments.

The paper's methodology provides a pragmatic balance between simplicity and granularity, offering valuable insights for integrating climate risk into financial decision-making processes, thus fostering sustainability in asset management strategies.