- The paper introduces a model-agnostic framework that integrates uncertainty measures with financial optimization to mitigate estimation errors.

- It combines techniques like subsampling and CVaR-SGD to address computational challenges and enhance out-of-sample performance in real market data.

- Empirical results from pairs trading and deep hedging demonstrate that uncertainty-aware strategies yield superior risk-adjusted returns over traditional plug-in approaches.

Uncertainty-Aware Strategies for Financial Optimization

This paper introduces a model-agnostic framework for robust financial optimization, addressing the critical issue of model uncertainty in quantitative finance. The core idea involves enhancing traditional objective functions with an outer "uncertainty measure" defined over the space of possible models. This approach offers a practical way to mitigate the risks associated with relying on single, potentially misestimated models.

Uncertainty Measures and Robust Strategies

The paper formalizes the concept of uncertainty-aware strategies, contrasting them with the conventional "plug-in" approach. The plug-in strategy optimizes an investment objective based on a single estimated probability measure, P^, while the uncertainty-aware strategy considers a distribution of models, (Pθ)θ∈Θ, and incorporates an uncertainty measure, U, to account for model risk. The uncertainty-aware strategy is expressed as:

a∈Aargmax{U(J(X(a),Pθ),Θ)},

where A is the space of admissible actions, X(a) is the payoff of action a, J is the investment objective, and Θ represents the uncertainty about which model is correct. Common risk measures like entropic risk (Entr) and conditional value-at-risk (CVaR) are employed as uncertainty measures.

Analytical Comparison in an i.i.d. Gaussian Setting

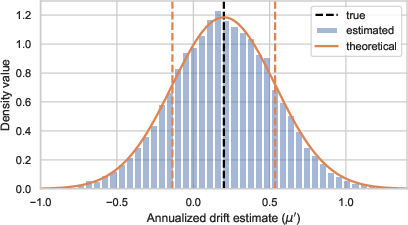

To illustrate the benefits of uncertainty-aware strategies, the paper presents an analytical comparison in a simplified i.i.d. Gaussian setting. Here, the estimation error of the drift can significantly impact investment decisions (Figure 1).

Figure 1: A graphical representation, showing how data of N=90 days are not sufficient to obtain accurate estimates of the mean.

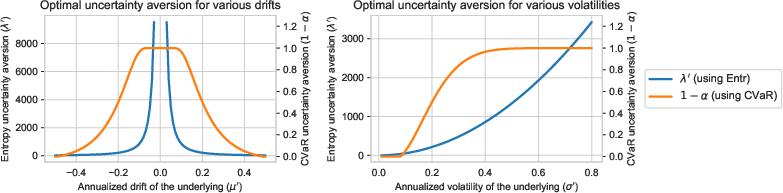

The out-of-sample performance of the plug-in strategy, uncertainty-aware strategies (using both Entr and CVaR), and a mixture measure approach are compared. The analysis demonstrates that uncertainty-aware strategies, for sufficient robustification preferences, outperform the plug-in and mixture measure approaches, particularly when estimation errors are significant. The optimal choice of uncertainty aversion parameters, λ′ and α, depends on the market conditions, with stronger robustification needed in markets with lower drifts and higher volatilities (Figure 2).

Figure 2: Graphical representation of the optimal choice of uncertainty aversion λ′,α that result in the highest out-of-sample performance for the uncertainty-aware strategies.

Subsampling as a Model-Agnostic Approach

The paper introduces a practical subsampling strategy to approximate model uncertainty. This method involves drawing multiple subsamples from the estimated distribution, P^, and using these subsamples to create a distribution of models. This approach is model-agnostic and computationally efficient, drawing parallels to bootstrapping techniques and mini-batch sampling in deep learning. The connection to the i.i.d. Gaussian example is established, showing that subsampling leads to strategies similar to those derived analytically.

Empirical Validation with Real Market Data

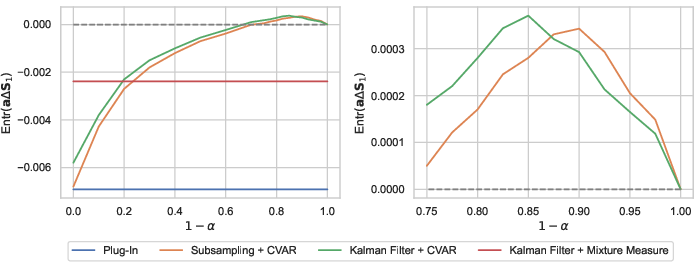

The effectiveness of the subsampling approach is demonstrated using real market data from a pairs-trading task between PepsiCo Inc. (PEP) and Coca-Cola Co. (KO). The returns of the spread process are modeled using an autoregressive model for the mean and a GARCH(1,1) process for the conditional variance. The results show that the uncertainty-aware strategy, with a subsample size of 30 and CVaR as the uncertainty measure, significantly improves performance compared to the plug-in strategy. The performance gains achieved by the subsampling approach are comparable to those obtained using a more elaborate Bayesian approach with a Kalman filter (Figure 3).

Figure 3: The performance of strategies on PEP-KO pair process.

CVaR-SGD for Overcoming Memory Constraints

To address the computational challenges associated with high-dimensional problems, the paper proposes a memory-efficient variant of stochastic gradient descent (SGD) tailored to uncertainty-aware optimization with CVaR. This CVaR-SGD algorithm simulates paths under a single model at a time, reducing memory consumption while maintaining computational efficiency. The convergence of the CVaR-SGD algorithm is formally established, and its effectiveness is demonstrated in a high-dimensional investing example using S{content}P 500 data.

Deep Hedging Example

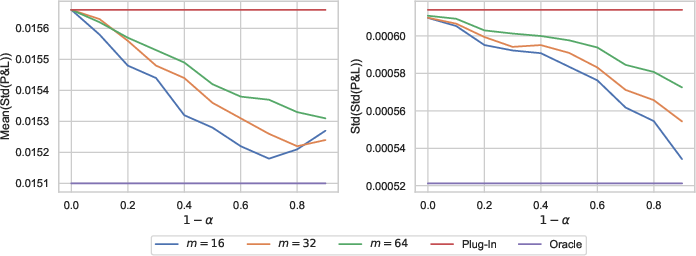

The paper further illustrates the benefits of uncertainty-aware strategies in a deep hedging context. A hedging task for a cliquet option is considered, and the hedging strategy is learned using a neural network. The results show that uncertainty-aware hedges, trained with subsampling and CVaR, consistently outperform their plug-in counterparts in terms of both mean and variance of the resulting objectives on the test distribution (Figure 4).

Figure 4: A plot comparing the mean objective and standard deviation of objective from the plug-in, uncertainty-aware, and oracle hedges.

Conclusion

The paper presents a comprehensive framework for addressing model uncertainty in financial optimization. The proposed uncertainty-aware strategies, combined with the subsampling approach and the memory-efficient CVaR-SGD algorithm, offer a practical and robust solution for a wide range of financial applications. The combination of analytical results, simulated examples, and empirical validation with real market data provides strong support for the effectiveness of the proposed approach. These techniques could be extended to other areas such as optimal execution, portfolio construction, and risk management where uncertainty in model parameters can significantly impact performance.