- The paper presents a quantum algorithm that translates the Kolmogorov forward PDE for local-volatility option pricing into a Hamiltonian simulation problem using Schrödingerisation.

- The methodology employs efficient state preparation, gate-based Hamiltonian simulation, and swap-test retrieval to process high-dimensional asset models and complex payoff structures.

- The approach achieves polynomial speedup for single-asset options and exponential scalability for multi-asset scenarios, addressing the curse of dimensionality.

Quantum Algorithm for Local-Volatility Option Pricing via the Kolmogorov Equation

Introduction and Context

Option pricing in quantitative finance is fundamentally a high-dimensional, path-dependent problem exacerbated by complex payoff structures and non-trivial price dynamics. Classical methods for option pricing, such as finite difference schemes for PDEs and Monte Carlo SDE simulation, often become computationally intractable in the presence of local or stochastic volatility models and multiple risk factors. This paper presents a quantum algorithmic framework for solving the Kolmogorov forward partial differential equation (Fokker–Planck equation) within local-volatility (LV) models by translating the option-pricing PDE into a quantum Hamiltonian simulation problem. The approach uses the Schrödingerisation technique, allowing for the simulation of non-Hermitian dynamics within the constraint of quantum unitary evolution.

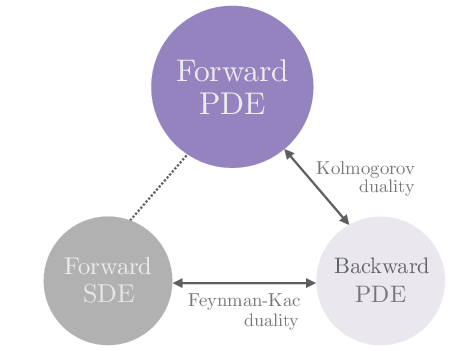

The paper begins by clarifying the distinction between forward and backward PDE formulations for option pricing. The forward approach models the evolution of the underlying asset's price distribution forward in time—computing the expected discounted payoff over the terminal distribution. Alternatively, the backward approach propagates the option value backward from terminal maturity, with the payoff function as a terminal condition.

Figure 1: Equivalent differential-equation formulations for option pricing. Forward models propagate asset dynamics, while backward models propagate option value; both relate through Kolmogorov equations and the Feynman-Kac formula.

A critical insight established by the authors is that, while the backward PDE encodes the contract value at each node, the forward PDE computes the evolved price distribution, from which multiple payoffs can be evaluated efficiently post-evolution. This makes the forward formulation especially advantageous for multiclass pricing scenarios such as basket or path-dependent options.

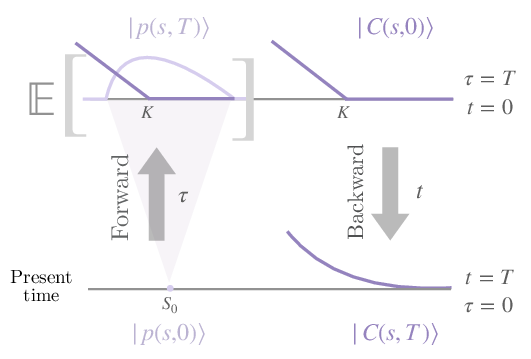

Figure 3: Schematic comparison between the forward (price evolution) and backward (option value evolution) paradigms in option-pricing.

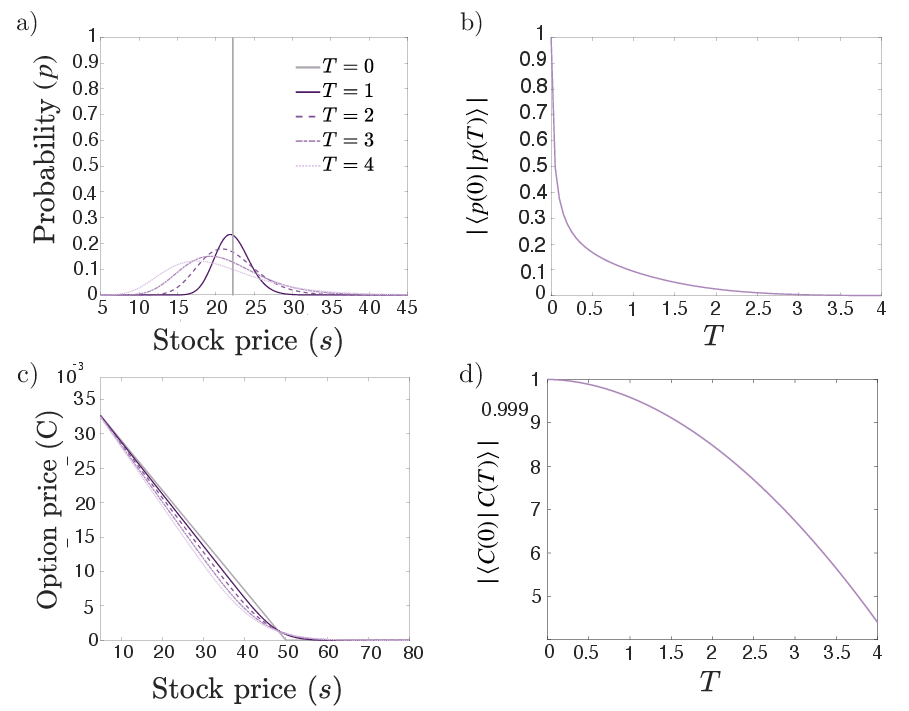

Further analysis in the quantum context highlights that solution overlap (quantum fidelity) between initial and terminal states remains high for backward models—hindering quantum distinguishability during evolution and thus making resource requirements prohibitive. In contrast, forward evolution yields significantly decayed overlaps at maturity, resulting in more favorable quantum readout characteristics.

Figure 2: Decay of quantum state overlap for the forward Kolmogorov equation compared to near-constant overlap in the backward PDE scenario.

The Local-Volatility Model and Quantum Encoding

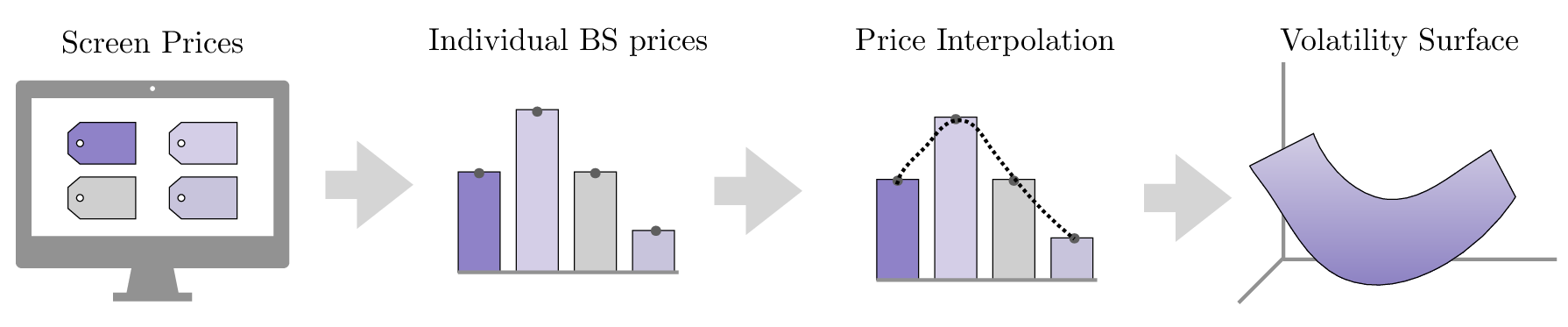

The local-volatility model, foundational in capturing the volatility surface observed in real market data, induces significant computational complexity since volatility becomes an explicit function of both asset price and time. The authors present a construction for volatility surfaces from market-implied Black–Scholes volatilities using Dupire's framework.

Figure 4: Constructing a local-volatility diffusion process from market-implied European options via the Dupire procedure.

To encode this LV model on a quantum computer, classical price grids and volatility surfaces are discretized and mapped to quantum amplitude registers. The resulting probability distribution at maturity is encoded via amplitude encoding—not Q-sampling—facilitating direct manipulation of the Kolmogorov equation dynamics.

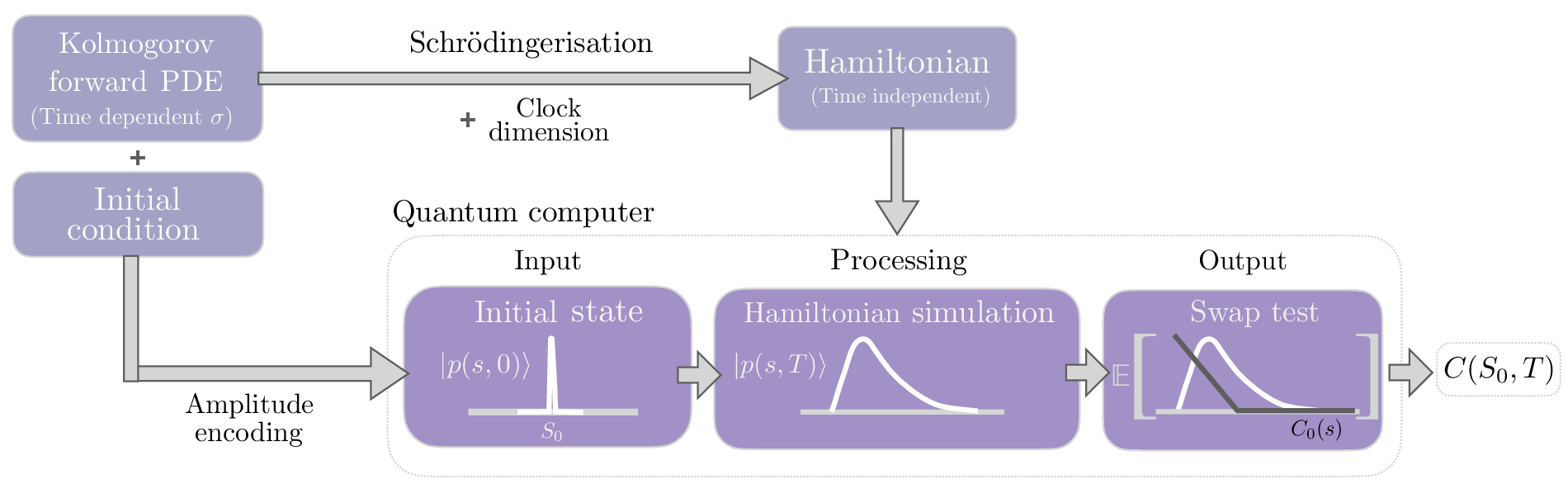

Central to the method is a gate-based quantum algorithm for evolving the discretized Kolmogorov forward PDE under local-volatility using Hamiltonian simulation. The IPO model structure is employed:

- Input: Classical financial data (initial price, volatility surface) is encoded into quantum states using efficient preparation protocols for piecewise polynomials.

- Processing: The evolution is mapped to a Hamiltonian derived from the LV PDE, including non-Hermitian terms, using the Schrödingerisation technique. This introduces auxiliary quantum registers and clock dimensions to handle non-unitary and time-dependent dynamics, respectively.

- Output: Upon completion of the simulation, post-selection and swap-test circuits are used to efficiently retrieve expectation values corresponding to option prices across multiple payoffs.

Figure 5: IPO framework for quantum algorithms: classical input encoding, quantum processing via Hamiltonian simulation, and information retrieval via measurement protocols.

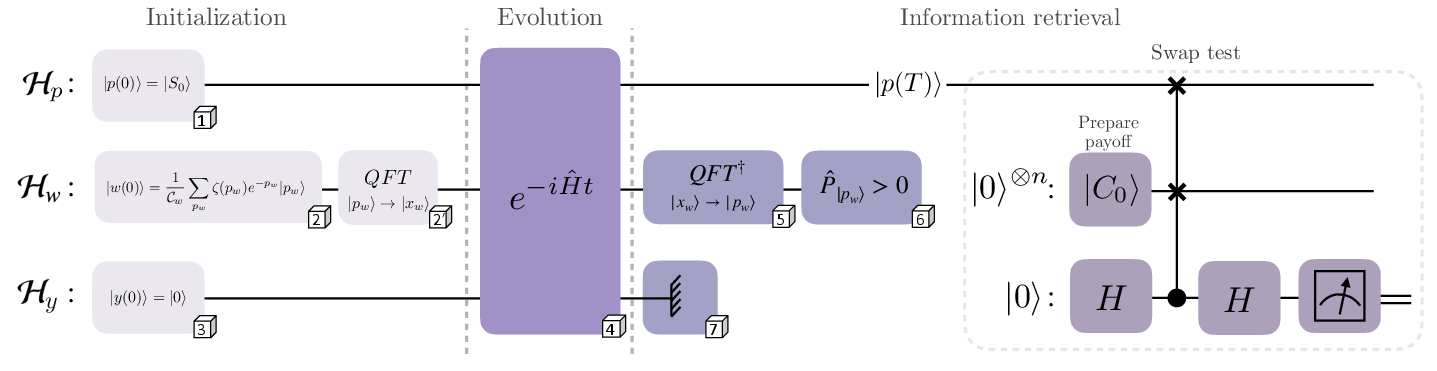

A detailed schematic of the algorithmic workflow is presented:

Figure 6: Complete quantum circuit for Kolmogorov forward equation simulation, including state preparation, ancillary dimension initialization, Hamiltonian simulation, and information retrieval.

Implementation Methodology and Complexity Analysis

State Preparation

States encoding the initial Dirac-delta (price) and auxiliary spaces (Schrödingerisation and clock dimensions) are constructed using circuits for piecewise polynomial functions. This is efficient, scaling polynomially in the register size.

Hamiltonian Simulation and Schrödingerisation

A main result is that the non-unitary LV PDE can be efficiently embedded into a larger Hilbert space and simulated unitarily via the Schrödingerisation scheme. The time dependence in local volatility introduces a clock dimension, rendering the total Hamiltonian time-independent at the cost of moderate Hilbert space enlargement.

Gate complexity for the evolution step is dominated by the maximum discretized derivative operator norm, scaling as ∼22n in the number of qubits per register, reflecting the contribution of the second-order momentum term and necessitating careful balancing of grid resolution and precision.

Block-encoding techniques supplant black-box oracular accesses, allowing explicit circuit-level construction for sparse Hamiltonians with piecewise polynomial coefficients—a significant contribution over previous oracle-based approaches.

Calculation of option prices proceeds via the swap test to estimate expectations between the forward-evolved quantum state and prepared payoff states. This method efficiently accommodates a wide range of payoffs, including multi-asset and basket options. Error propagation is precisely analyzed, with the total error scaling as the sum of discretization bias (O(2−n)) and statistical shot noise (O(Nshots−1/2)).

Classical–Quantum Complexity Comparison

In Appendix analyses, the quantum approach is shown to improve classical cubic scaling for Kolmogorov PDEs to quadratic scaling in spatial grid size, i.e., O(N2logN) quantum gate complexity vs. O(N3) in classical banded solvers. Crucially, the quantum simulation cost grows only linearly with the number of dimensions for multi-asset models, circumventing the curse of dimensionality endemic to classical approaches.

Multi-Asset Extensions and Scaling

The proposed framework accommodates high-dimensional LV models (e.g., baskets and spreads), with initial state preparation and evolution scaling polynomially in the number of assets. The main bottleneck is the operator norm contributed by cross-derivative (correlation) and second-order stochastic terms, but dimensional scaling remains tractable, supporting applications to multi-factor and basket derivatives.

Implications, Limitations, and Future Prospects

This work demonstrates a consistent, end-to-end quantum procedure for numerically evolving the Kolmogorov forward equation under a local-volatility model with rigorous resource and error analysis. The main impact is in showing that:

- Single Option Instance: Quantum speedup is polynomial but not exponential, as leading complexity contributions scale quadratically in grid resolution.

- High-Dimensional Regime: The quantum method achieves exponential improvement with respect to dimension compared to classical algorithms, providing a route to tractable pricing of derivatives with many risk factors.

Bold claim: The polynomial, and in the high-dimensional limit, exponential speedup for basket or multi-factor options distinguishes the presented approach from both classical and previous quantum methods.

Limitations include the reliance on precise initial state preparations, error accumulation in swap-test measurement, and potential challenges in volatility surface discretization fidelity. The extension to American, Asian, or path-dependent exotic options will require addressing jump conditions and free boundaries with further method development.

Conclusion

By mapping the Kolmogorov forward equation for local-volatility option pricing to a quantum Hamiltonian simulation task via Schrödingerisation, this work provides an explicit, resource-aware algorithmic pathway that achieves polynomial speedup for single-asset models and exponential complexity reduction for high-dimensional derivatives. The explicit circuit construction, elimination of black-box dependencies, and rigorous error/complexity analysis set a quantitative standard for future quantum financial engineering. The framework's modularity suggests adaptability to more general stochastic models and risk management tasks, signifying a substantive advance in quantum computational finance.