- The paper demonstrates a novel integration of manifold learning with financial market forecasting by mapping data to various constant-curvature geometries.

- It employs tailored stochastic differential equations and local Gaussian curvature analysis to simulate and classify market dynamics, highlighting toroidal embeddings for cyclic trends.

- Machine learning models applied in tangent spaces improve market predictions, offering enhanced risk assessments and quantitative trading strategies.

The Shape of Markets: Machine Learning Modeling and Prediction Using 2-Manifold Geometries

The paper "The Shape of Markets: Machine Learning Modeling and Prediction Using 2-Manifold Geometries" explores financial market forecasting by embedding high-dimensional market data onto constant-curvature 2-manifolds. The methodology leverages the unique properties of spherical, Euclidean, hyperbolic, and toroidal geometries, with the torus identified as particularly effective for capturing cyclical market dynamics. This novel approach integrates manifold learning with financial forecasting, providing insights applicable to complex, non-linear financial datasets.

Methodology

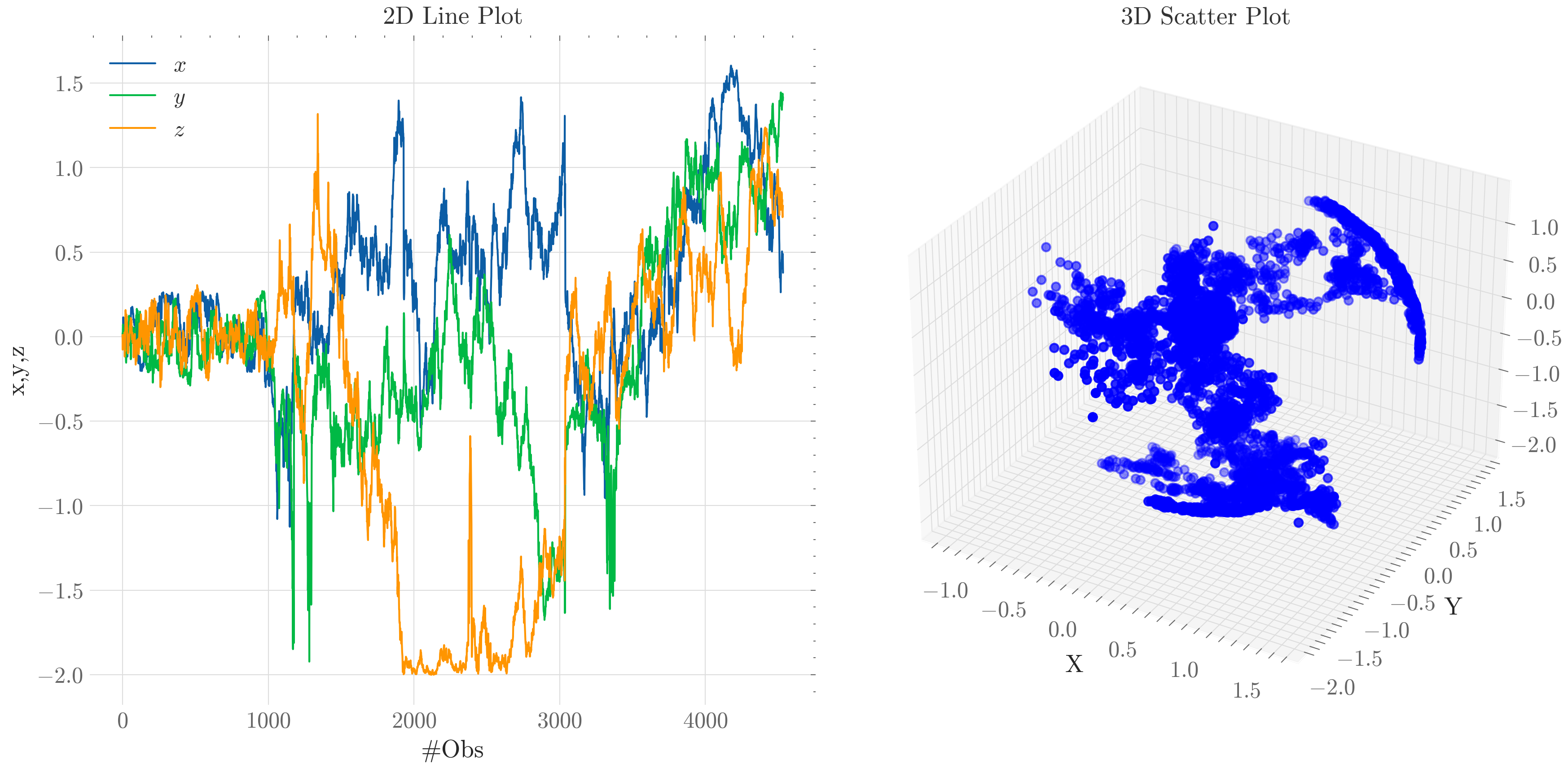

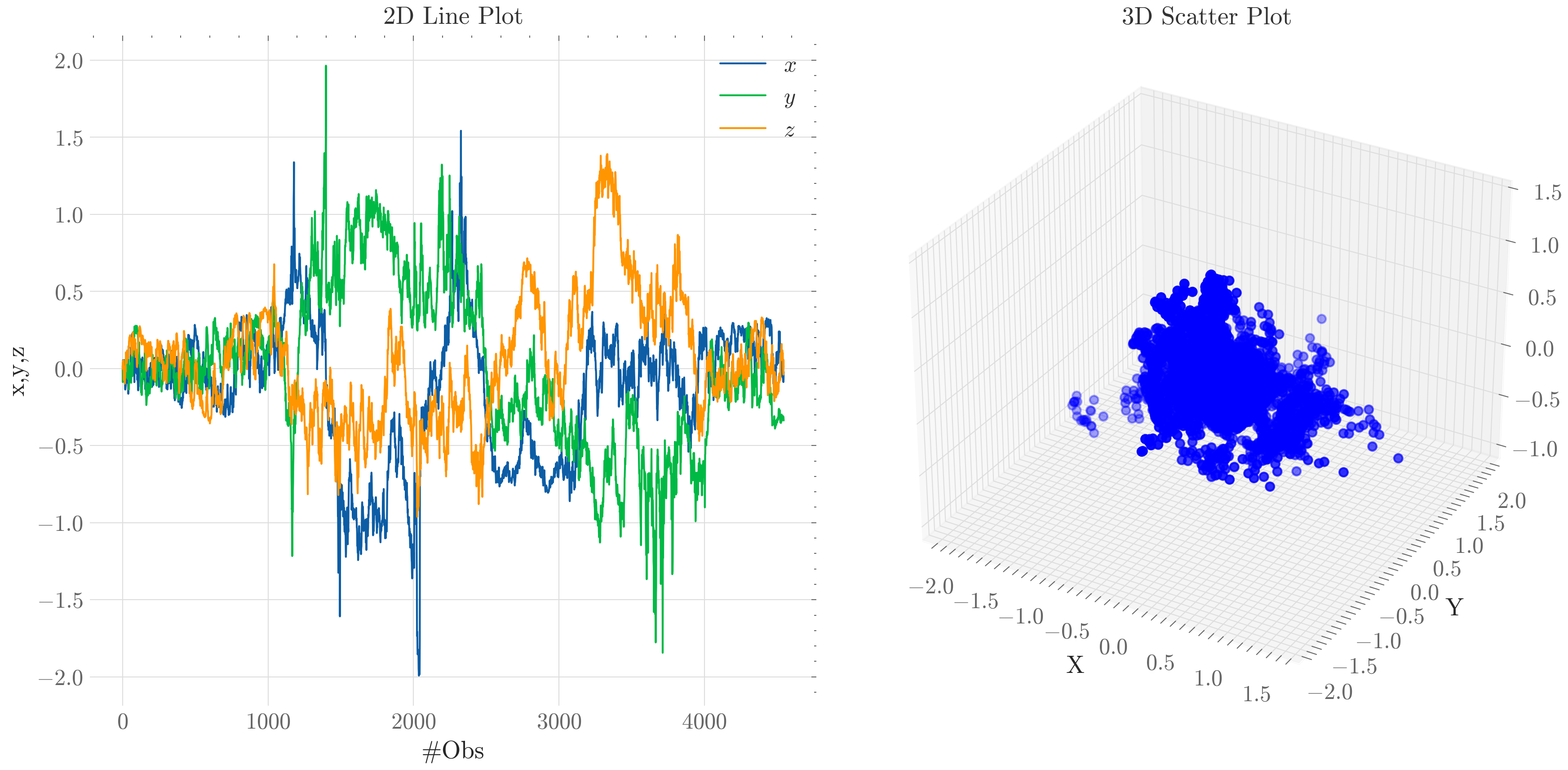

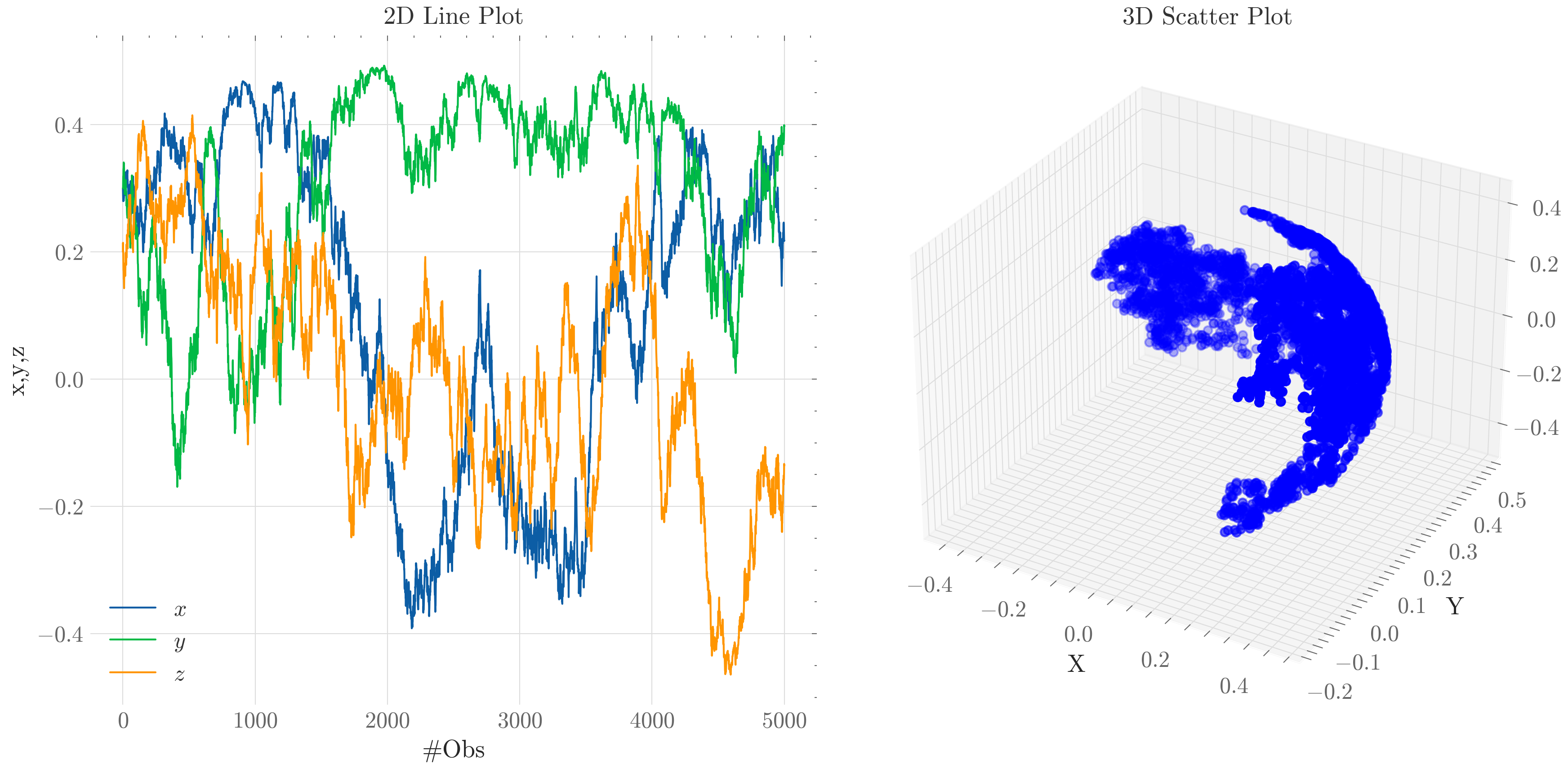

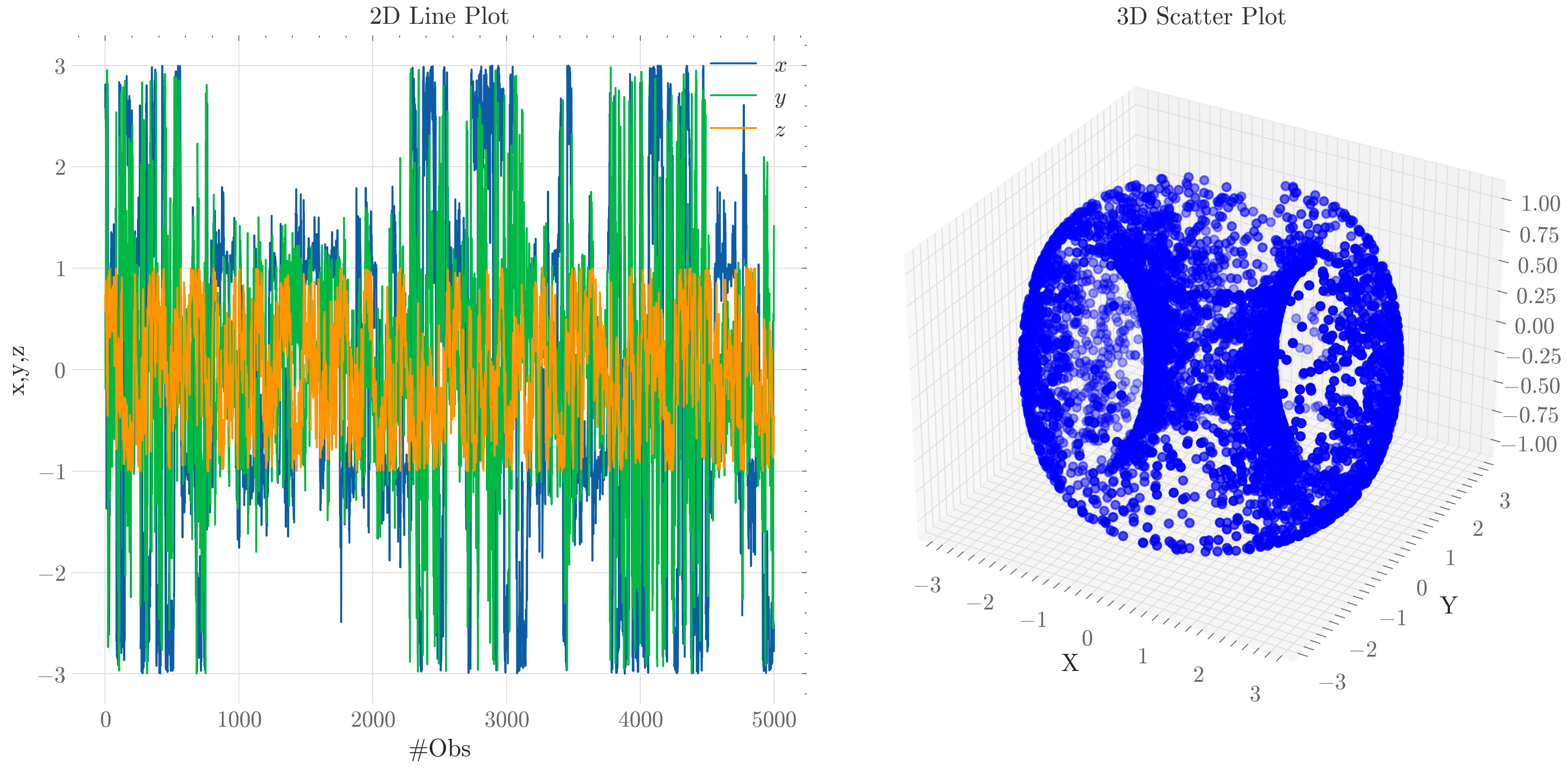

Brownian Motion and Manifold Embedding

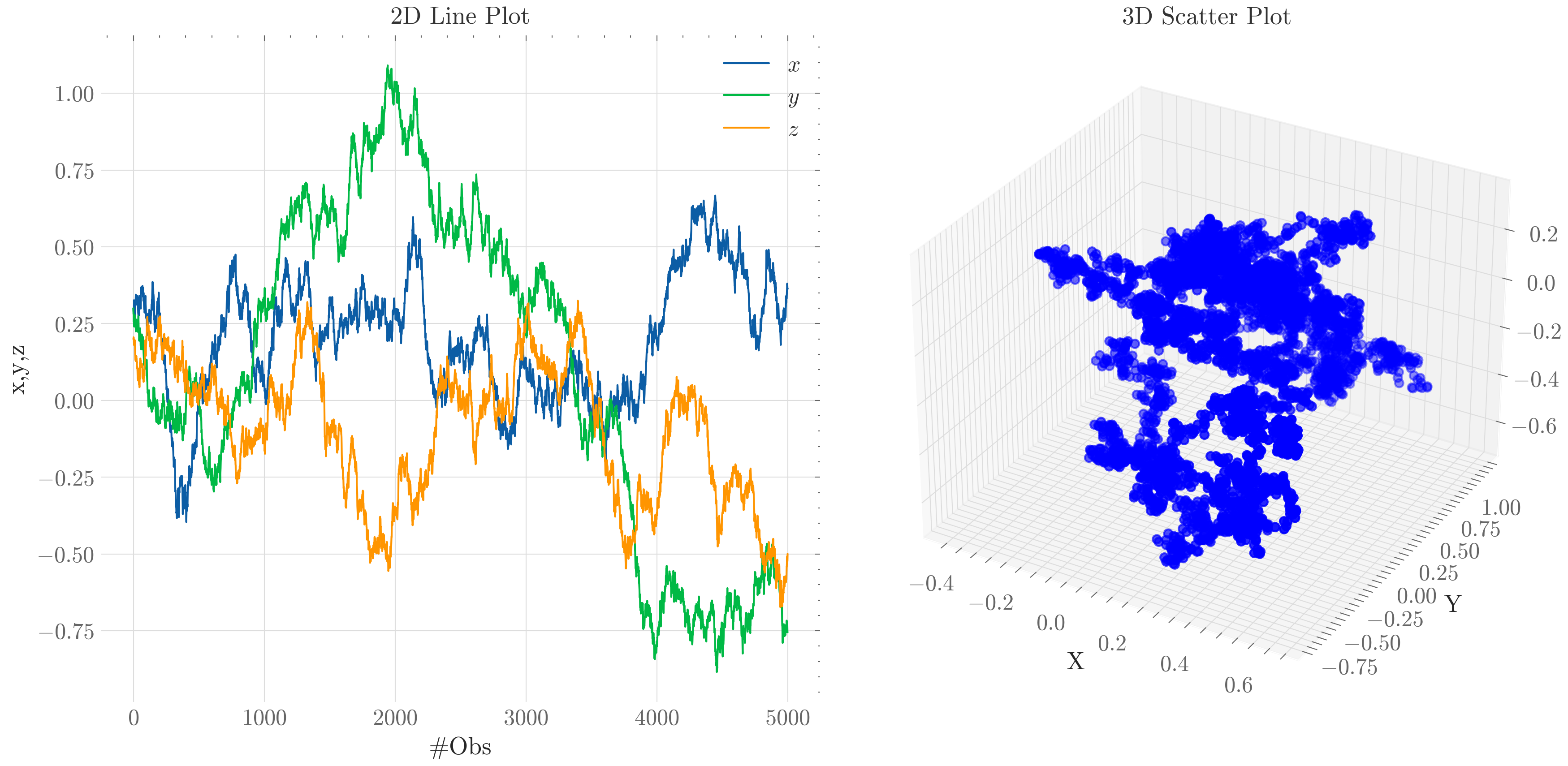

The paper constructs Brownian motions within spherical, Euclidean, hyperbolic, and toroidal geometries to simulate market dynamics. It uses stochastic differential equations (SDEs) tailored to each geometry. Specifically, the model employs Stratonovich SDEs and derives explicit formulations for different geometries, including the unique challenges of simulating on the torus and hyperbolic planes.

Figure 1: Simulated Brownian-motion scenarios: time-series panels (a–g) and the corresponding 3D PCA embedding (h).

Geometry Inference and Market Prediction

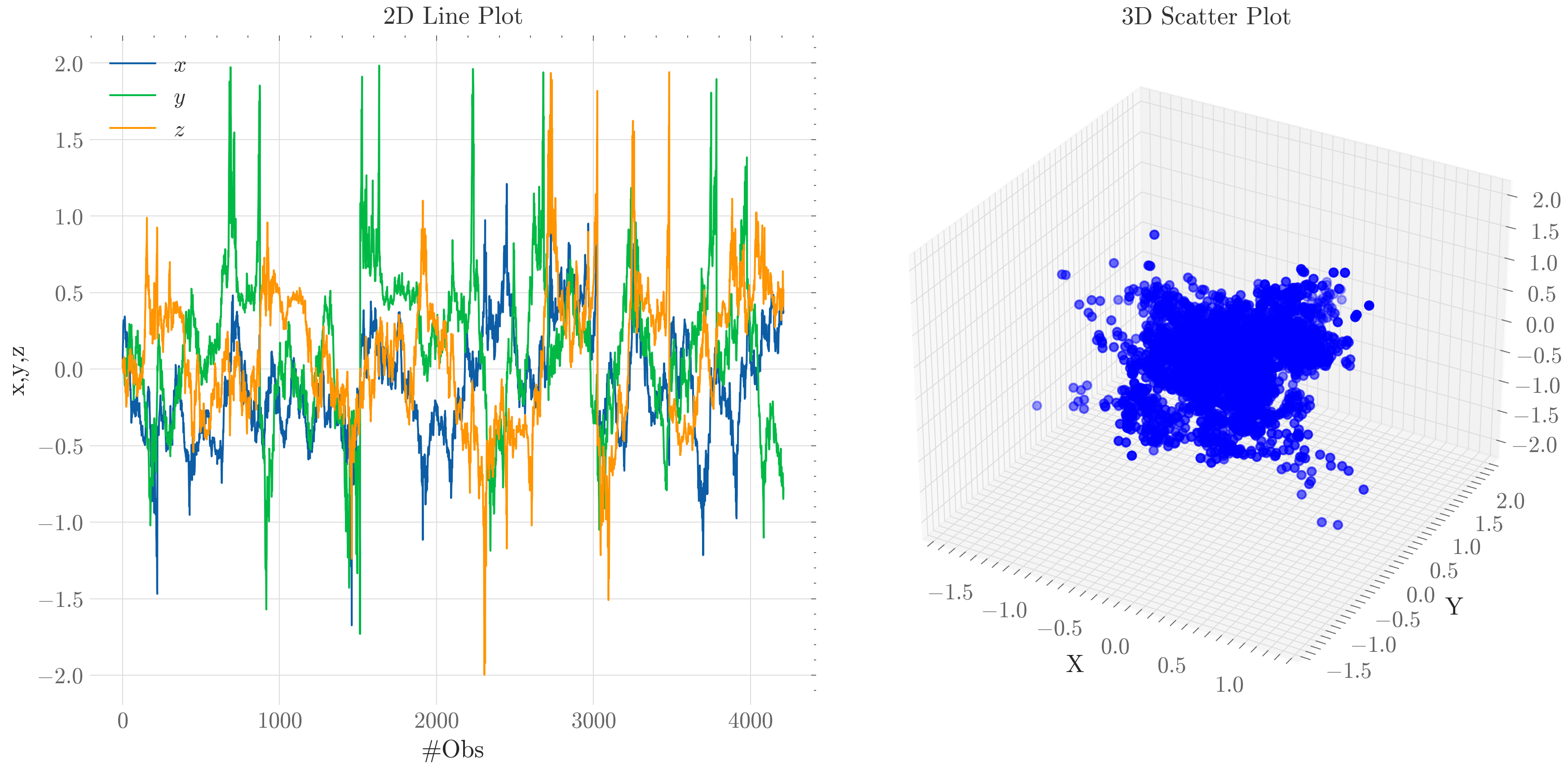

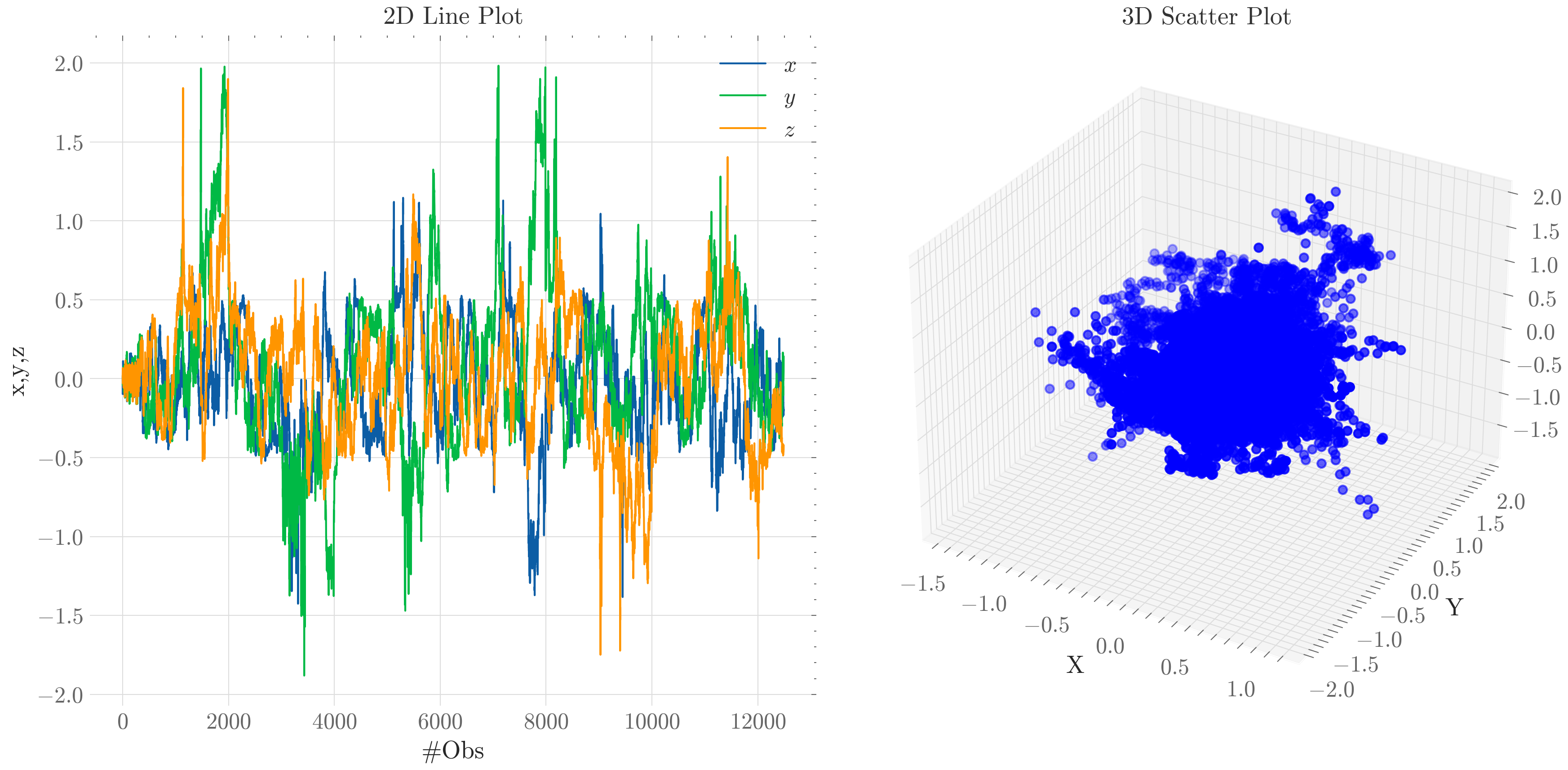

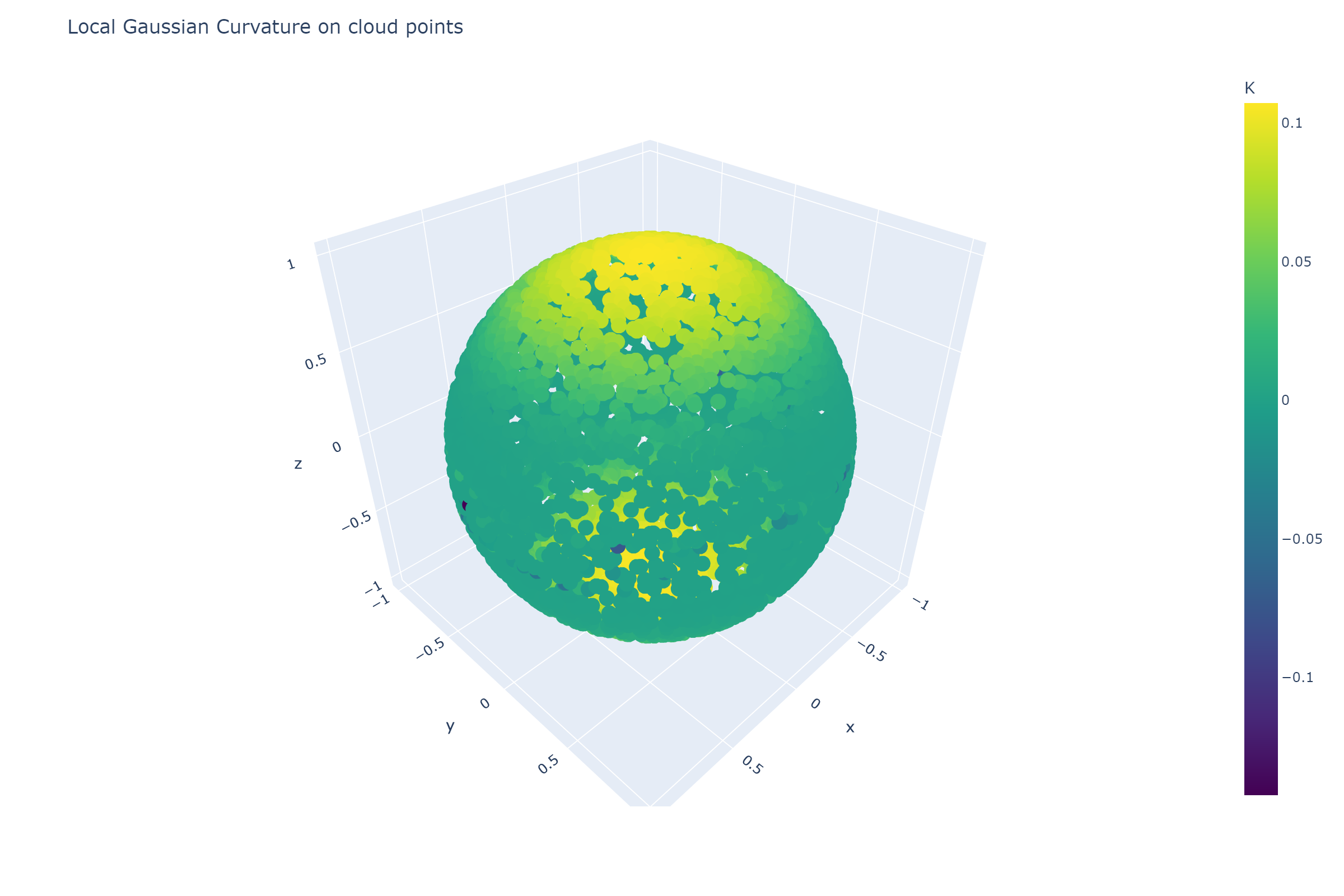

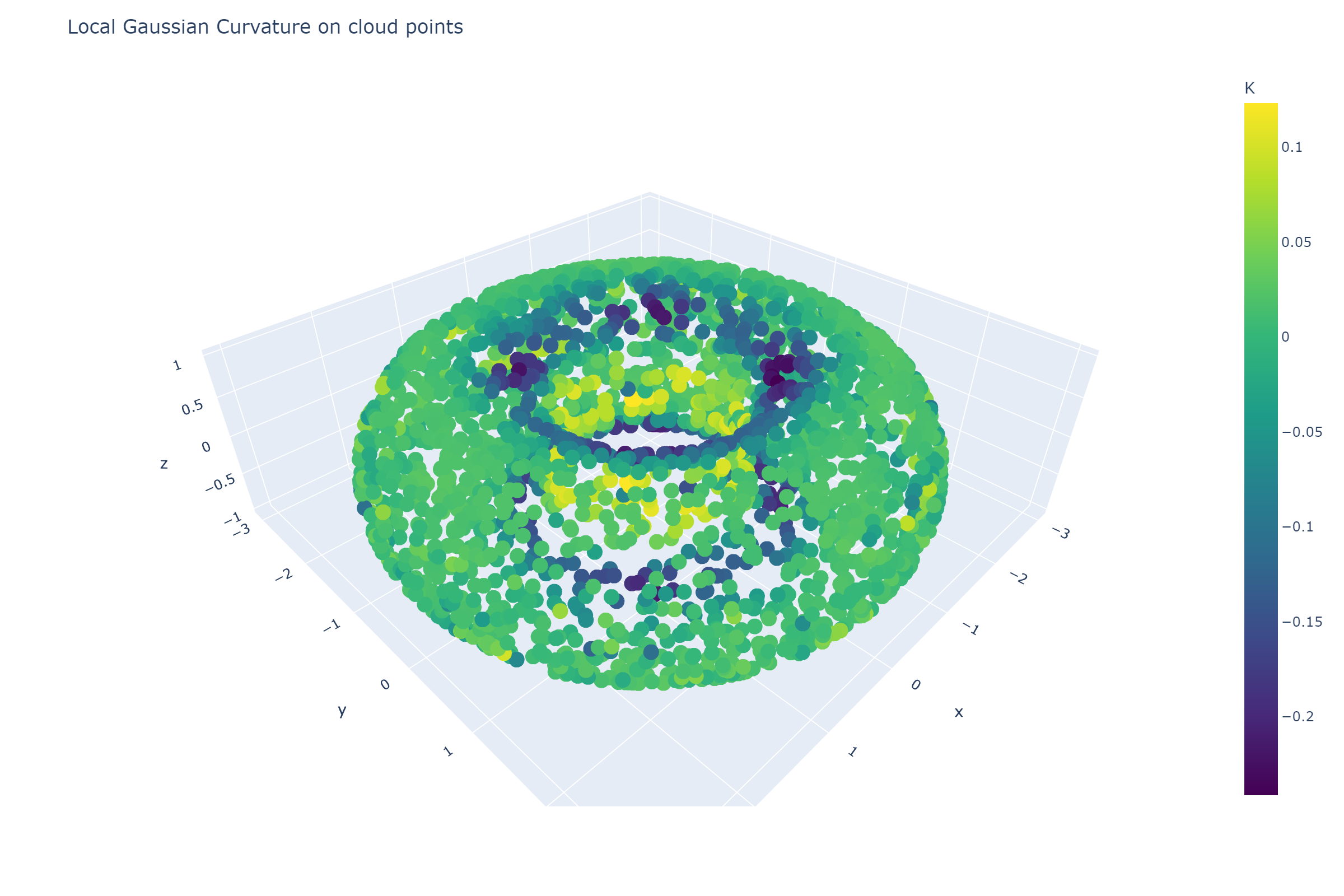

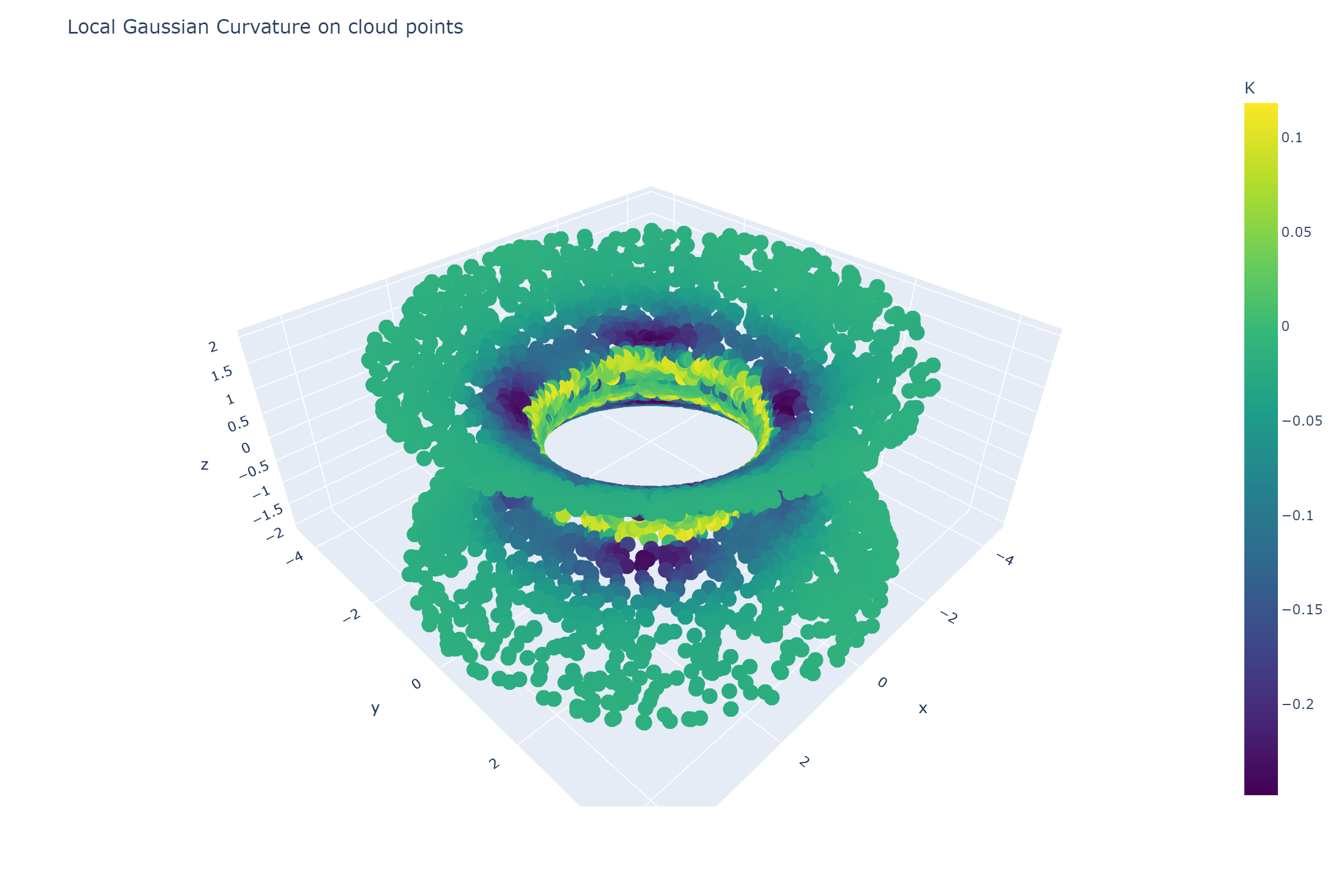

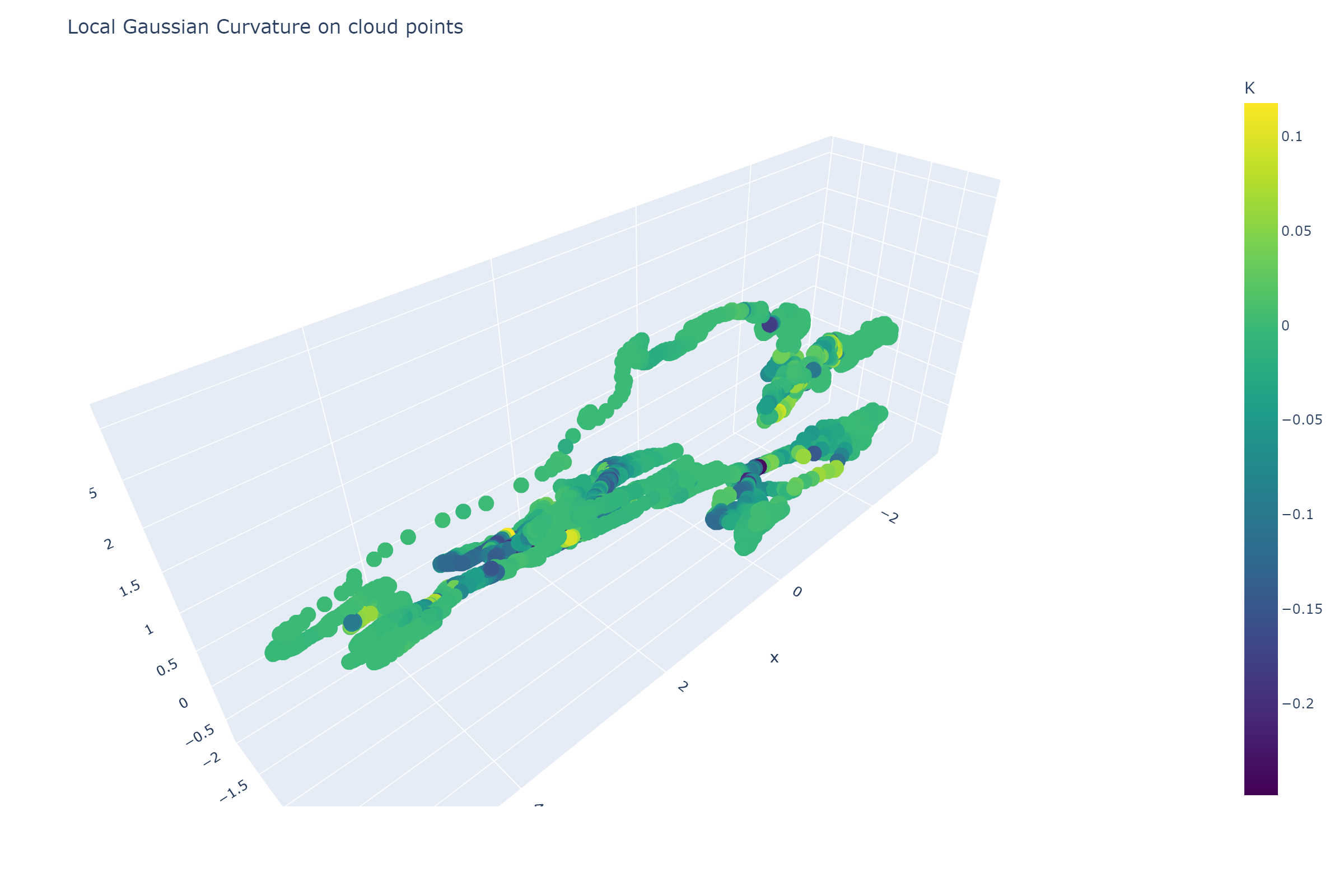

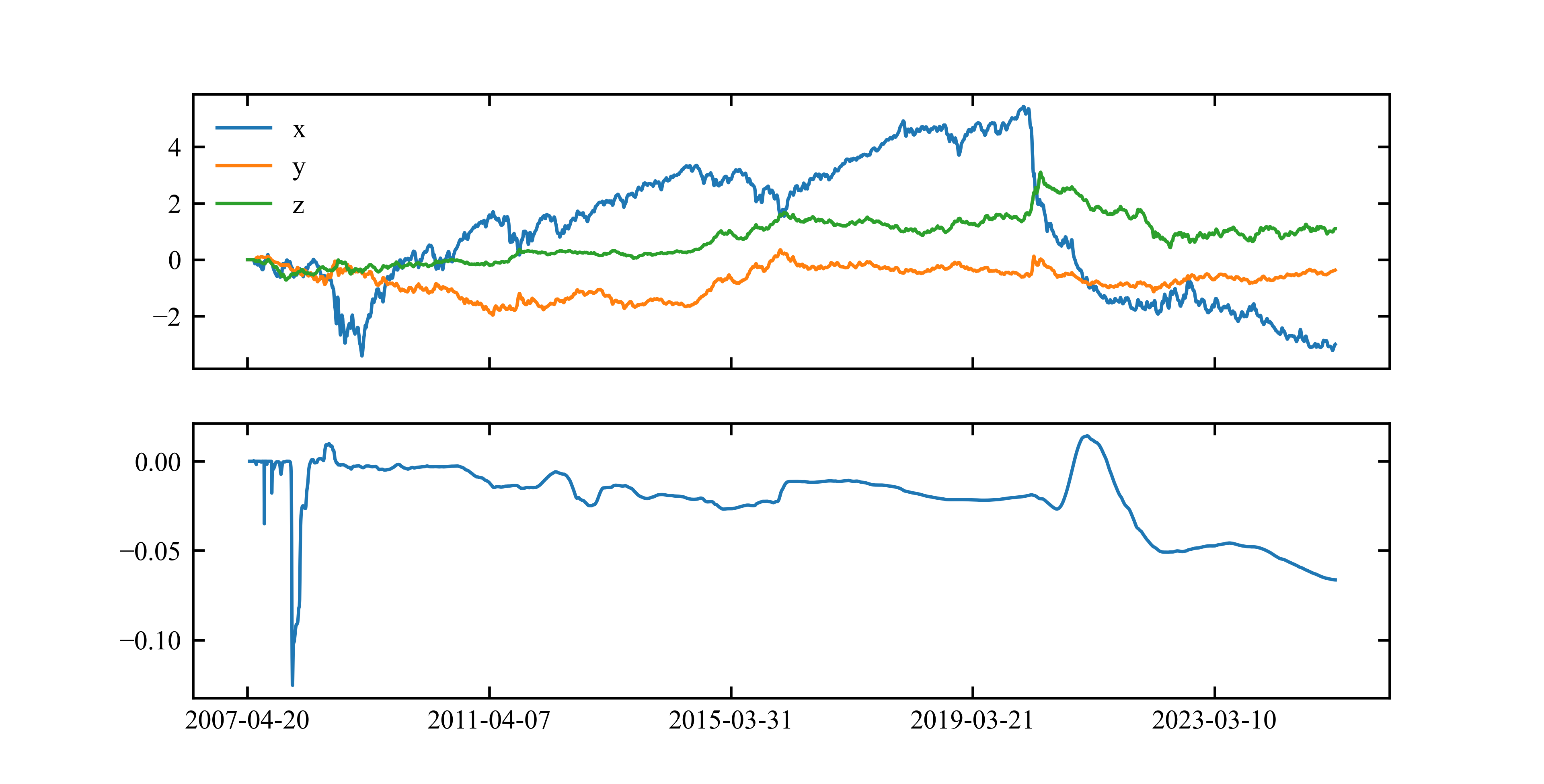

The paper applies local Gaussian curvature analysis to infer the most representative manifold for observed financial trajectories. This involves estimating Gaussian curvatures at each point to determine the underlying geometric nature, effectively classifying market paths based on their curvature behavior.

Figure 2: Local Gaussian curvature estimates K across benchmark shapes and the real-data embedded path. The benchmarks provide sign/scale references; the finance panel shows intermittent, regime-like curvature bursts.

Machine Learning in Tangent Spaces

To predict future market behavior, the paper employs machine learning models, such as Random Forests (RF) and Gaussian Processes (GP), to forecast in the tangent space of the inferred manifold. These forecasts are then mapped back to the manifold space using exponential maps, allowing for geometry-aware market predictions.

Results and Implications

The paper demonstrates the effectiveness of manifold-based embeddings in market forecasting, particularly highlighting the cyclical dynamics captured by toroidal embeddings. The experimental results suggest that manifold geometries provide a robust framework for modeling complex, cyclical market behaviors, outperforming traditional Euclidean models in capturing non-linear financial patterns.

Practical Applications

This approach opens new avenues for financial analytics, potentially enhancing the accuracy of risk assessments and quantitative trading strategies. By aligning financial data with appropriate geometric models, investors can gain deeper insights into market dynamics and improve forecast reliability.

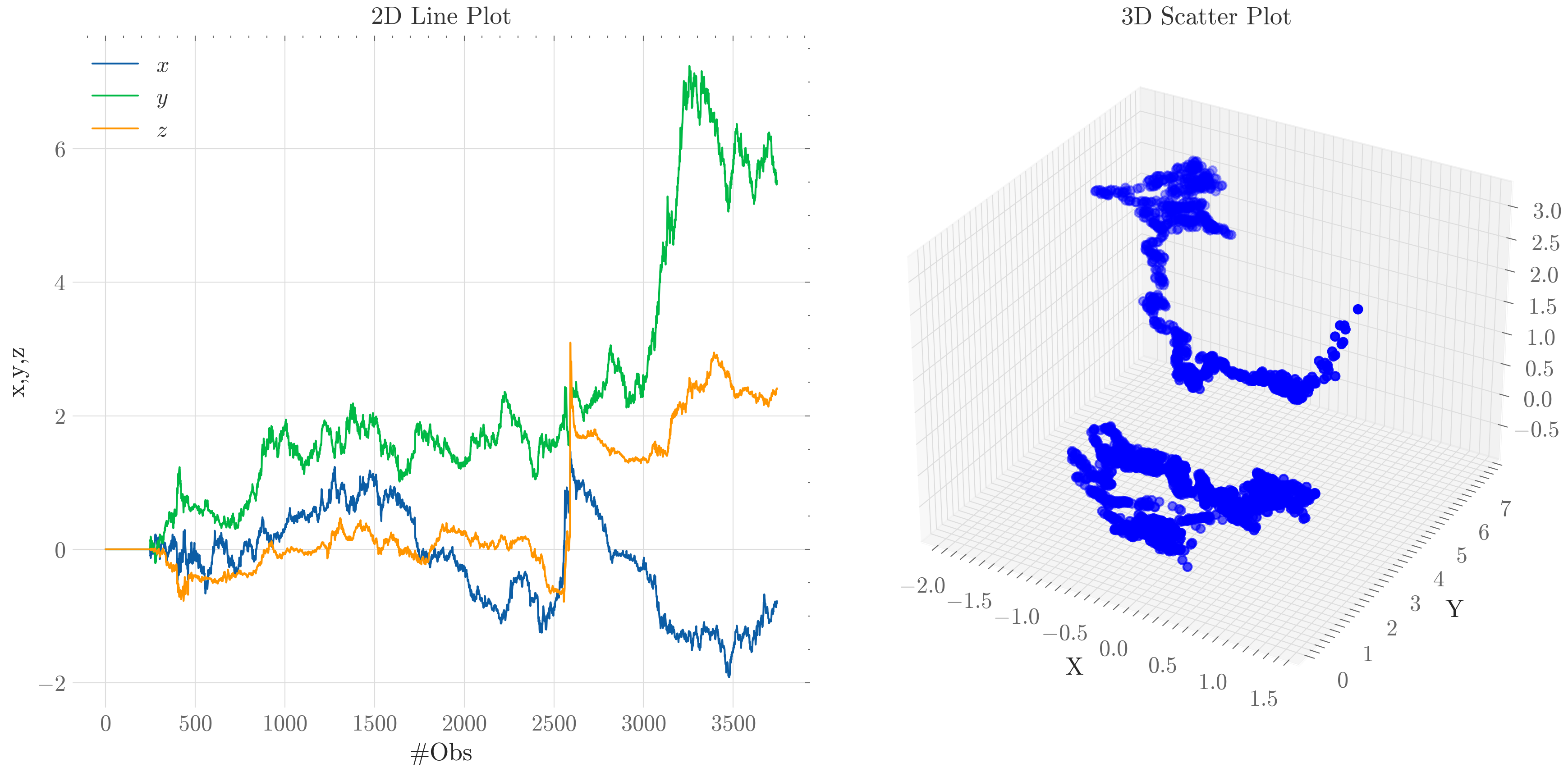

Figure 3: PCA projections evolution (Upper panel) and curvature estimation (Lower panel) for the real financial dataset. x is PC1 (1st eigenportfolio), y is the PC2 (2nd eigenportfolio) and z the PC3 projection (3rd eigenportfolio), respectively.

Conclusion

The integration of differential geometry with machine learning for financial market analysis marks a significant advancement in quantifying market complexities. By embedding market data into constant-curvature manifolds, this methodology uncovers latent market structures that traditional models overlook, providing a more nuanced and predictive understanding of market dynamics. Future research may focus on refining these models and exploring their applications across various financial instruments.