- The paper introduces a steady-state framework that reduces dynamic matching and allocation problems to static optimization via unique stationary distributions.

- It integrates queueing theory with mechanism design to derive optimal admissions, priority rules, and information policies in both NTU and TU market settings.

- The analysis reveals that FCFS uniquely maintains waiting incentives in dynamic queues while large market limits converge to efficient static auction outcomes.

Dynamic Market Design: A Steady-State Framework for Asynchronous Matching and Queueing

Introduction and Motivation

Market design theory has traditionally been based on static models assuming synchronous and simultaneous participation of all agents. However, digital platforms have enabled dynamic marketplaces where buyers and sellers arrive asynchronously according to stochastic processes. This paper ("Dynamic Market Design" (2601.00155)) surveys and develops a robust methodology based on transforming complex, infinite-horizon dynamic allocation and matching problems into tractable static optimization problems by focusing on their long-run stationary distributions. Integrating insights from queueing theory and mechanism design, it addresses both non-transferable utility (NTU) and transferable utility (TU) environments, developing a general framework for optimal admissions, information, and priority policies.

Methodological Core: Stationary Regenerative Mechanisms

The central methodological innovation is the restriction to positive-recurrent, regenerative mechanisms (PRRMs). These mechanisms induce queue-state processes admitting unique stationary distributions, allowing objectives and incentive constraints to be formulated as static programs. Specifically, the designer's dynamic control is abstracted into the choice of a stationary distribution over queue states, subject to implementability via a PRRM. The associated challenge is twofold: (1) characterizing feasible stationary distributions through "Border-style" constraints and (2) reducing the dimensionality of the queue-state space—especially in the presence of agent heterogeneity—without loss for optimality.

This approach permits the derivation of sharp characterizations of optimal policies in both NTU and TU markets, including precise conditions under which classic disciplines such as FCFS, LCFS, and SIRO are, or are not, optimal.

Non-Transferable Utility (NTU): Queueing as a Price Substitute

In NTU settings, monetary transfers cannot be used, necessitating methods such as queueing or lotteries for allocation and screening.

Externalities and Incentive Management: Unlike prices, queue entry imposes externalities on future entrants. The magnitude and nature of these externalities depend on admission policy, priority rules, and the information revealed to agents. PRRMs allow designers to directly manage both entry and information, with incentive compatibility evaluated in the stationary regime.

Benchmark—First-Best and Cutoff Policies

Ignoring incentive constraints, the welfare-maximizing solution is a static cutoff policy on queue/inventory sizes, balancing option values for potential matching against holding costs (c for buyers, d for inventory).

Under complete queue observability (e.g., physical queues), Naor's analysis establishes that FCFS discipline induces excessive queueing relative to the social optimum due to negative congestion externalities. LCFS, as shown by Hassin, can internalize these externalities by concentrating the entire waiting cost on the "first incumbent," making agents' private incentives align with the social optimum. However, practical implementation of LCFS (and related rules like LIEW) faces severe concerns regarding strategic re-entry, interruption costs, and strong aversion by queue participants.

Leshno demonstrates that when social costs of waiting are non-consequential (stockout risk dominates), FCFS may under-incentivize waiting, while SIRO and LIEW (load-independent waiting) can sometimes restore allocation efficiency. Yet, optimal incentives can be achieved equivalently through coarse information policies: by lumping queue states (e.g., only disclosing whether k<K∗), a designer can simulate the incentive effects of SIRO/LIEW, making service discipline less relevant when information is optimally managed.

Crucially, in the absence of aggressive admissions control, FCFS cannot alone implement the welfare optimum—especially when buyers have insufficient incentives to wait.

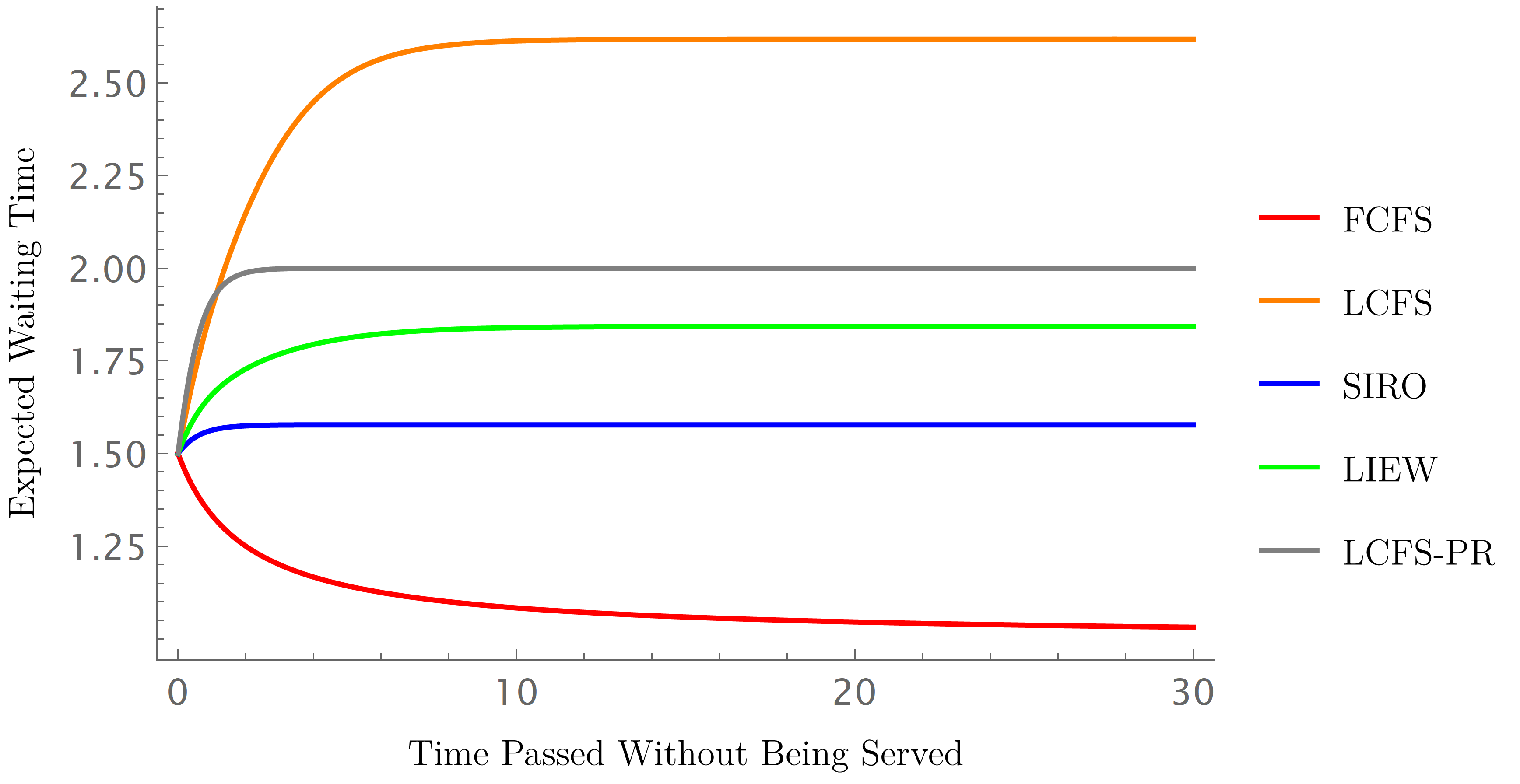

A key result is that, with both admissions control and optimal information design, FCFS is sufficient for implementation of the welfare-optimal stationary distribution for all α∈[0,1] (weights on buyer vs. seller welfare). When encouraged to join (conditional on not exceeding the cutoff), waiting incentives are aligned across possible service disciplines. However, only FCFS supports the necessary dynamic incentives for buyers to remain in the queue over time: under alternative disciplines, residual expected wait times increase as time elapses, prompting abandonment and undermining implementation.

Figure 2: Expected residual wait times under FCFS, SIRO, LIEW, and LCFS, demonstrating that only FCFS ensures incentives to remain in queue decrease over time.

FCFS's unique property is that it ensures waiting times are least dispersed, which, in the context of optimal information design, is critical for supporting equilibrium adherence to both entry and continuation recommendations.

Large Market Limit

As the arrival rates grow, queue fluctuations vanish (the "fluid limit"), and the only inefficiency in FCFS arises from excessive waiting under full observability and no admissions control—welfare can be restored to optimal via tight cutoff or randomization.

Heterogeneous Types and Screening

Extending to heterogeneous types in the fluid model, the framework reveals a sharp trade-off: while randomized allocation eliminates socially wasteful waiting, optimal screening (allocative efficiency) demands waiting costs as implicit prices, generating welfare losses. For regular (decreasing inverse hazard rate) distributions, the socially optimal solution is complete pooling—a random lottery—sacrificing all type-based allocative efficiency to avoid wasteful queueing costs.

Transferable Utility (TU): Dynamic Myersonian Mechanisms

In TU markets, monetary transfers eliminate the need for queueing as an implicit price, but the designer must still manage the intertemporal allocation and competition among stochastically arriving agents and goods.

Optimal Mechanism Structure

The dynamic market design problem generalizes Myerson's static auction theory to stochastic queues of buyers and items. The relaxed problem involves maximizing a virtual surplus functional, subject to Border-type feasibility constraints on static allocation and implementable balance conditions on stationary queue-state transitions. The solution specifies (a) cutoff thresholds for admissions depending on the endogenous queue state, (b) auctions for available goods, and (c) storage caps on inventory. The mechanism can be implemented via dominant-strategy incentive compatible (DSIC) dynamic auctions with state-dependent reserve prices and "cutoff prices," with the allocation rule relying only on reported values (not arrival order).

Revenue and Welfare Maximization Contrasts

Notably, in contrast to NTU, the welfare-optimal mechanism in the large market limit recovers allocative efficiency—all high-value agents are allocated goods without distortion. Under finite queue costs or inventory costs, distinctions between revenue and welfare maximization are nuanced, with the ordering of cutoff thresholds crossing over as queues expand.

Large Market Convergence

In the limit of large or frictionless markets, the stationary distribution becomes degenerate, the dynamic mechanism approaches the static uniform price auction, and all intertemporal queueing and storage vanish.

Theoretical and Practical Implications

Theoretical Significance

- Reduction to Static Programs: The stationary-distribution-based approach enables the leveraging of powerful linear programming and convex analysis methods for otherwise intractable dynamic mechanism design and matching problems.

- Border-like Constraints in Dynamics: The adaptation of Border's reduced-form constraints and majorization characterizations for queue-based feasible allocations is a nontrivial technical innovation.

- Queue Discipline and Information Policy: The results clarify when service priority is material (as in standard queueing games) and when, with optimal information and admissions, it becomes entirely subsumed.

Broader Perspectives and Generalizations

The paper connects to multiple other literatures: screening with state-independent mechanisms, dynamic matching, frictional search markets, dynamic revenue management, and dynamic mechanism design with evolving types. Its queue-regenerative approach sits apart by modeling stochastic arrivals and emphasizing steady-state analysis over finite-horizon or batch models.

Future Directions

Open areas include generalizing NTU analysis to settings with type heterogeneity outside the fluid limit—currently hampered by dimensionality and tractability concerns—and, in TU environments, adding multidimensional private information (costs, patience, complex service requirements). There is also scope for extensions to two-sided private information, correlated arrivals, and learning of unknown demand/supply rates.

Conclusion

This paper establishes a formal and unified steady-state market design framework for dynamic platforms with asynchronous and stochastic arrival of agents and goods. By reducing complex intertemporal mechanism and matching problems to static optimization over stationary distributions, the work delivers comprehensive prescriptions for admissions, information, and priority rules in both NTU and TU regimes. It exposes fundamental trade-offs between screening, allocative efficiency, and social waste, and lays the groundwork for theoretically principled design of modern digital marketplaces that must manage queueing, competition, and matching in real time.