- The paper introduces a breakdown frontier approach to jointly relax monotonicity and independence assumptions in binary-outcome IV frameworks for causal inference.

- Utilizing nonparametric estimators and bootstrapping, the method calculates sharp identification bounds for LATE and ATE under controlled deviations.

- Empirical application to family size and female unemployment shows that even minor violations can undermine standard IV conclusions.

Sensitivity Analysis in Instrumental Variables: Joint Relaxations of Monotonicity and Independence

Introduction

The paper "Sensitivity Analysis for Instrumental Variables Under Joint Relaxations of Monotonicity and Independence" (2603.25529) investigates the partial identification of causal effects in binary-outcome instrumental variables (IV) frameworks, focusing on Local Average Treatment Effects (LATE) and the Average Treatment Effect (ATE) under simultaneous, explicit relaxations of the canonical monotonicity and independence assumptions. The core technical contribution is the construction of "breakdown frontiers," which delineate the largest combinations of violation magnitudes of both assumptions that still allow researchers to draw pre-specified substantive conclusions about the LATE.

Model and Relaxations

The approach denotes an assignment variable Z (the instrument), which may imperfectly affect treatment uptake due to compliance issues. The model permits the actual treatment D to diverge from assignment, with outcomes Y governed by potential outcomes Y(D(z),z), all binary-valued.

Violations of instrument independence are parameterized using the c-dependence framework of Masten & Poirier (2018), where c upper bounds deviations between propensity scores computed on observables versus those that incorporate unobserved potential treatments and outcomes. Simultaneously, monotonicity is relaxed by allowing a strictly positive share of defiers Tdef, constrained to be less than the share of compliers. Both parameters c and Tdef are on probability scales and thus directly trade-off in robustness analysis.

Identification Bounds

The paper delineates sharp identified sets for potential joint and marginal probabilities, and, crucially, for parameters of substantive interest such as the ITT, LATE, and ATE, as functions of c and D0.

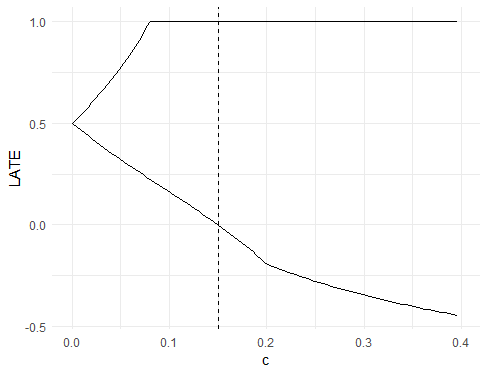

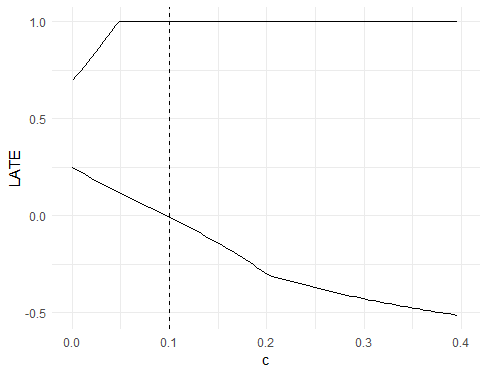

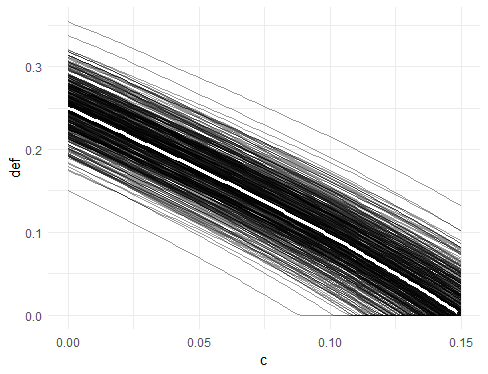

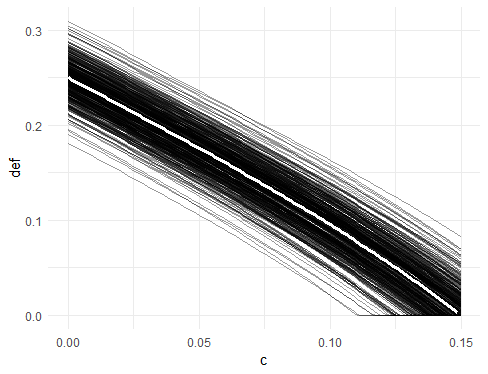

Figure 1: Identified sets for the LATE as a function of D1, contrasting the cases D2 (left) and D3 (right).

For D4, sharp identification is possible if monotonicity is assumed, with the identified set collapsing to the standard Wald estimand for LATE. As D5 increases or D6 grows, the sets widen and may quickly become too broad to yield sign-identified or policy-relevant inference—a critical, nontrivial finding substantiated numerically.

Breakdown Frontiers: Robustness to Assumption Violations

The central methodological innovation is the breakdown frontier (BF): level sets in the D7 plane corresponding to the weakest combinations of assumption violations under which a given conclusion, e.g., D8, can still be maintained. Analytically, the frontiers can be expressed in closed form and are shown, under regularity, to sharply separate robust from non-robust regions for qualitative inference.

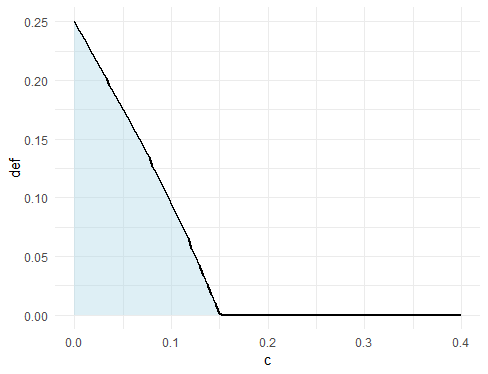

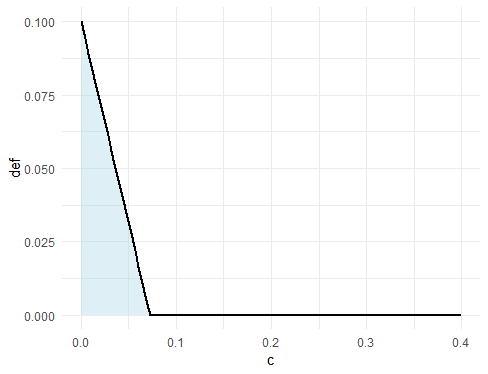

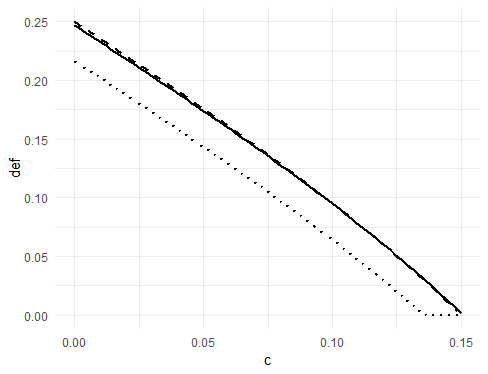

Figure 2: Breakdown frontiers for the LATE exceeding D9 (left) and Y0 (right). Robust regions indicated in blue.

The BF approach generalizes and systematizes sensitivity analysis beyond one-dimensional relaxations, precisely quantifying the joint margin-of-error for both monotonicity and independence. Notably, trade-offs are transparent: allowing larger shares of defiers strictly contracts the set of permissible Y1 values (and vice versa) under which sign-inference or policy conclusions can be drawn.

Estimation and Inference

Consistent, nonparametric sample-analogue estimators of both the identified set bounds and the breakdown frontiers are proposed and analyzed using the mathematical machinery of Hadamard directional differentiability and the functional delta method. Standard nonparametric bootstrapping is extended using the results of Fang & Santos (2018) and Hong & Li (2018), yielding asymptotically valid uniform confidence bands for the frontier curves.

Figure 3: Sampling distribution of the breakdown frontier estimator for N=1000 (left) and N=2000 (right), indicating consistency and the absence of finite-sample bias.

Figure 4: Finite-sample bias of the breakdown frontier estimator is negligible, with coverage of lower confidence bands tracking near true values.

Monte Carlo experiments substantiate the inferential validity, displaying minimal bias and proper coverage even with moderate sample sizes.

Empirical Application: Family Size and Female Unemployment

The methodology is illustrated through a re-analysis of the canonical Angrist & Evans (1998) application, using "same-sex" as an instrument for family size when estimating effects on female non-employment. Baseline calibrations obtained from selection-on-observables techniques and external survey data provide context for plausible magnitudes of Y2 and Y3. The breakdown frontier analysis reveals that even minute violations—Y4, Y5—invalidate the qualitative conclusion that the effect of additional children on non-employment is negative. The permissible robustness region lies strictly inside plausible values for both parameters, sharply limiting the empirical credibility of substantive findings predicated on conventional IV assumptions.

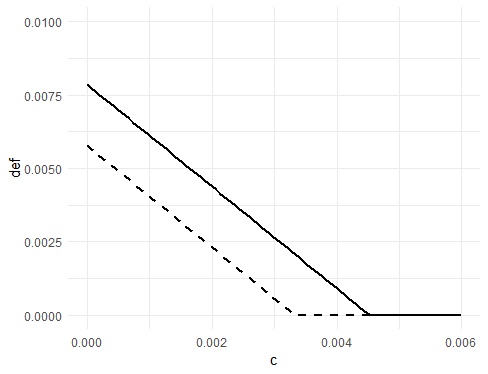

Figure 5: Breakdown frontier for the estimated effect of family size on unemployment; empirical robustness is not supported for realistic violation levels.

Theoretical and Practical Implications

This work makes precise the extent to which standard IV-based inference is reliant on strict monotonicity and independence. The explicit, joint parametrization and graphical presentation via breakdown frontiers provide a tool for immediate assessment of sensitivity; robustness claims must be quantified with respect to both dimensions, not abstractly presumed. Results underscore that in many empirical contexts (especially when both assumptions may be questionable), even weak or moderate violations can suffice to render IV point estimates uninformative.

Theoretically, these findings highlight the crucial role of partial identification and the necessity to report robust regions rather than relying solely on point identification. The functional delta method extensions and uniform bootstrap confidence bands serve as a blueprint for robust inference in other nonstandard settings involving directionally differentiable functionals.

Conclusion

By reframing IV sensitivity analysis as a breakdown frontier problem and rigorously quantifying the limits of assumption-robustness, this research exposes the fragility of qualitative IV conclusions under joint relaxations of monotonicity and independence. The proposed approach is not only methodologically general, but also practically implementable, supporting recalibration of empirical standards in applied econometrics. Future work may extend to multivalued treatments, other forms of non-compliance, or different violation parameterizations, and address inference refinements in weak instrument regimes.