- The paper introduces a novel DRO framework that uses Wasserstein ambiguity sets to enhance decision-making under uncertainty.

- It employs a kernel-based Nadaraya-Watson estimator to ensure convergence to the true conditional distribution with finite-sample guarantees.

- Real-world experiments on the newsvendor and portfolio optimization problems validate its computational tractability and robust performance.

Distributionally Robust Prescriptive Analytics with Wasserstein Distance

The paper "Distributionally Robust Prescriptive Analytics with Wasserstein Distance" introduces a new approach to prescriptive analytics, leveraging distributionally robust optimization (DRO) with Wasserstein ambiguity sets to make decisions under uncertainty concerning historical sample data. This paper is particularly focused on optimizing decisions using covariates or contextual information through a novel distributionally robust framework that has strong theoretical and practical implications.

In prescriptive analytics, the challenge is to choose a decision z that minimizes the conditional expectation E[c(z,Y)∣X=x], given a set of historical covariate and outcome pairs (X,Y). This paper utilizes a distributionally robust approach, which enhances traditional Sample Average Approximation (SAA) and robust optimization methods by formulating the problem using a DRO framework. Under this framework, the ambiguity in the distribution is addressed using Wasserstein metrics, allowing the decision-maker to effectively incorporate covariate information into the optimization process.

Methodology and Contributions

The paper proposes a kernel-based method using the Nadaraya-Watson estimator to construct nominal distributions of Y∣X=x centered within a Wasserstein ball. This approach guarantees that the nominal distribution converges to the true conditional distribution, providing strong out-of-sample performance guarantees and asymptotic convergence. The key contributions are as follows:

- Theoretical Guarantees and Statistical Bounds: The paper shows the statistical consistency of the estimator and provides finite-sample performance bounds using measure concentration inequalities. This includes demonstrating asymptotic convergence of both solutions and optimal values.

- Kernel-Based Wasserstein DRO: The kernel-based approach leverages the Nadaraya-Watson estimator, which provides flexibility in capturing the relationship between covariates and outcomes without strong parametric assumptions.

- Applications to Real-World Problems: The paper evaluates its framework through synthetic and empirical experiments on the newsvendor problem and portfolio optimization, illustrating its computational tractability and effectiveness in practical settings.

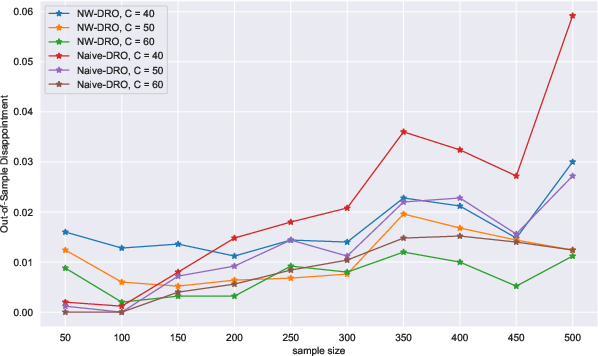

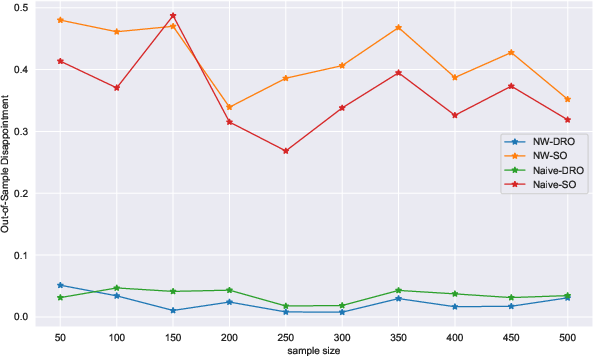

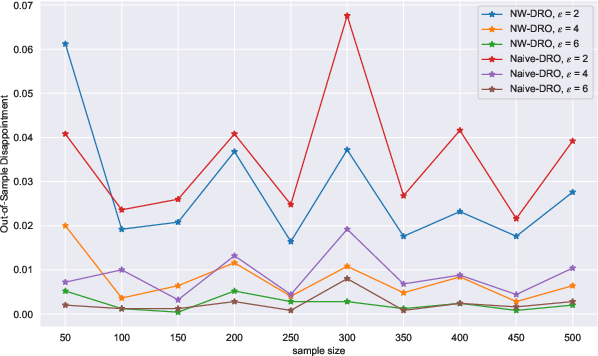

Figure 1: Out-of-sample disappointment against sample size n based on 2500 simulations. The radius of the Wasserstein ambiguity set is specified by ε (fixed size) or ε=C/n (varying size).

The duality principles are employed to reformulate the DRO problem into a convex optimization problem, making it computationally tractable. The strong duality is established by leveraging the properties of the Wasserstein metric, which allows the reduction of the primal problem to a series of convex problems through linear programming techniques.

These formulations are particularly beneficial for applications in portfolio optimization and risk management, where the authors show that CVaR-based risk measures can be calculated under this framework efficiently.

Implications and Future Directions

The proposed methodology offers a robust analytical framework for incorporating uncertainty in prescriptive analytics, particularly when dealing with complex and uncertain environments. As the field evolves, exploring extensions of this model to more complex distributions and incorporating variable selection algorithms would be a compelling direction for future research. Moreover, methodologies that address sparse or high-dimensional covariate spaces can further enhance the applicability of this framework in diverse real-world scenarios.

Conclusion

This paper makes significant strides in the development of distributionally robust mechanisms for prescriptive analytics, providing a theoretically sound and practically effective approach for decision-making under uncertainty. The integration of kernel methods with robust optimization techniques underpins a novel framework capable of delivering strong performance across various application domains.