From interacting agents to Boltzmann-Gibbs distribution of money

Published 11 Aug 2022 in math.PR | (2208.05629v1)

Abstract: We investigate the unbiased model for money exchanges: agents give at random time a dollar to one another (if they have one). Surprisingly, this dynamics eventually leads to a geometric distribution of wealth (shown empirically by Dragulescu and Yakovenko in [11] and rigorously in [2,12,15,18]). We prove a uniform-in-time propagation of chaos result as the number of agents goes to infinity, which links the stochastic dynamics to a deterministic infinite system of ordinary differential equations. This deterministic description is then analyzed by taking advantage of several entropy-entropy dissipation inequalities and we provide a quantitative almost-exponential rate of convergence toward the equilibrium (geometric distribution) in relative entropy.

The paper establishes that unbiased one-coin exchanges yield a Boltzmann-Gibbs (exponential) wealth distribution with a mean μ at equilibrium.

It rigorously derives a uniform-in-time propagation of chaos, connecting stochastic agent dynamics to a deterministic nonlinear ODE system.

The study employs entropy-dissipation and log-Sobolev inequalities to quantify convergence rates and ensure robust error bounds in the wealth distribution.

From Interacting Agents to Boltzmann-Gibbs Distribution of Money: A Technical Summary

Model Formulation and Dynamical Framework

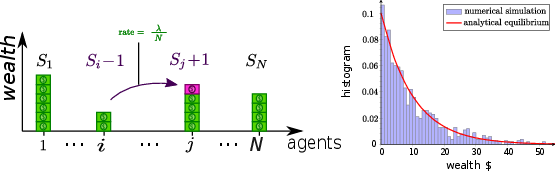

The paper rigorously investigates an agent-based model of wealth exchange, specifically the unbiased (one-coin) exchange mechanism first empirically observed to yield Boltzmann-Gibbs (geometric/exponential) wealth distributions. In a closed economy of N agents with mean wealth %%%%1%%%%, each agent initiates events in which, at random times (Poisson rate), they transfer a single unit of wealth to another randomly selected agent, provided they have at least one unit. The conservation law S1(t)+⋯+SN(t)=Nμ holds perpetually.

The primary stochastic dynamics can be represented:

At event times, agent i (the giver) and agent j (the receiver) are chosen uniformly. If Si(t)≥1, (Si,Sj)→(Si−1,Sj+1); otherwise, no exchange occurs.

This unbiased, memoryless, mean-field process is illustrated in (Figure 1), which showcases both the agent-level exchange rule and numerical evidence for the emergence of the exponential wealth distribution.

Figure 1: The unbiased exchange model dynamics and empirical steady-state wealth distribution, with decay consistent with an exponential profile of mean μ.

Mean Field Limit and Nonlinear ODE System

In the thermodynamic limit (N→∞), the dynamics for the marginal wealth distribution pn(t)=N→∞limP(S1(t)=n) are described by the infinite-dimensional, nonlinear ODE system: dtdp(t)=L[p(t)],

where

and r=1−p0 is the total proportion of agents with positive wealth.

This law of large numbers limit, which is standard in propagation of chaos theory [cf. (2208.05629)], reduces the stochastic agent-based dynamics to a deterministic nonlinear Markov process. The schematic correspondence is depicted in (Figure 2), and the reduction procedure is highlighted in (Figure 3).

Figure 2: Nonlinear ODE system describing the evolution of the marginal wealth distribution; interactions reduce to effective drift and jump operators.

Figure 3: Hierarchy of limiting procedures from the stochastic agent model to mean-field dynamics and further to ODE analysis.

At equilibrium, the ODE system admits the unique solution,

pn∗=(1−r∗)(r∗)n,

where r∗=μ/(1+μ), corresponding to the geometric (Boltzmann-Gibbs) distribution with mean μ.

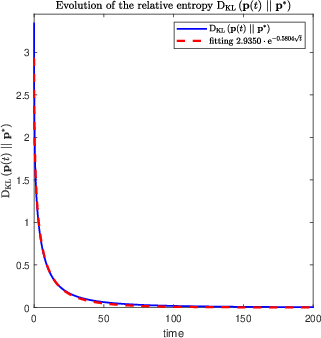

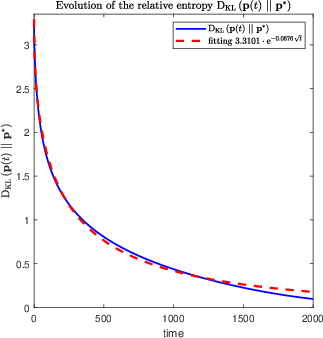

which quantifies proximity to equilibrium and admits an entropy-dissipation relation (i.e., an H-theorem property): dtdDKL(p(t)∥p∗)≤0.

The paper proves both polynomial and nearly-exponential decay of relative entropy:

For all time, DKL(p(t)∥p∗)≤C/(t+C).

For large t, DKL(p(t)∥p∗)≤Ce−Ct for some C>0 (almost exponential convergence).

These rates are established via analytic methods, notably entropy-entropy dissipation inequalities supported by log-Sobolev type estimates, not requiring direct recourse to the stochastic system, in contrast to previous literature. The functional framework allows one to track key macroscopic features (mass, mean, exponential moments) uniformly in time, and avoid finite-time blowups present in earlier methods.

Figure 4: Numerical validation of entropic convergence, displaying the nearly-exponential decay DKL(p(t)∥p∗)≈C1e−C2t for various initial data.

where q(t) is the histogram of the empirical distribution for the N-agent system and p(t) is the mean-field solution.

The relative entropy between these measures also decays: En∑qn(t)logpn(t)qn(t)≤C1+logNloglogN.

The proof relies on:

A precise stochastic entropy-dissipation calculation at the N-agent level.

Exponential moment propagation (via large deviation estimates), ensuring uniform control over wealth tails.

Quantitative log-Sobolev inequalities, interpolating between the empirical and the mean-field measure.

Careful handling of large deviations to guarantee that random fluctuations (ℓ1 norm) are controlled at all time, not just finite intervals.

Notably, the argument is analytic and does not rely on probabilistic optimal-coupling representations as in prior studies on related models. This yields a robust methodology applicable to a broad range of agent-based exchange mechanisms.

Implications and Future Directions

From a theoretical standpoint, the results provide an unambiguous explanation for the ubiquity of the exponential wealth distribution in unbiased binary exchange models, rigorously connecting agent-level stochasticity to deterministic infinite-particle behavior, and quantitatively characterizing relaxation to equilibrium using information-theoretic metrics.

The uniform-in-time propagation of chaos result, previously unavailable for this model, is essential for justifying the validity of kinetic or mean-field descriptions at all times, not only in transient or steady-state regimes. The technical apparatus (entropy dissipation, log-Sobolev estimate, exponential moment propagation) is highly portable and expected to extend to various generalizations, including poor-/rich-biased exchanges, models with random saving propensities, or systems incorporating debt and bankruptcy.

On the practical side, such agent-based to kinetic derivations, with explicit error bounds, are crucial for validating simulations and for informing the design and interpretation of economic, social, or physical models exhibiting similar stochastic exchange phenomena.

Conclusion

The paper delivers a rigorous and quantitative derivation of the emergence of the Boltzmann-Gibbs distribution of money in an unbiased agent-based exchange model. By providing analytic decay rates for entropy and uniform-in-time propagation of chaos, the work advances both the theoretical foundations of econophysics and the rigorous understanding of large-scale interacting particle systems. It opens future avenues toward more realistic models featuring heterogeneity, targeted exchange rules, or additional macroeconomic constraints, through the transplanted methodological innovations.