- The paper introduces a novel framework that leverages LLM filtering, multi-agent evaluation, and DNN optimization to mine alpha factors effectively.

- It employs adaptive composite weighting and rigorous backtesting on the SSE 50 Index, achieving significantly higher cumulative returns than traditional approaches.

- The approach demonstrates robust dynamic risk management and market responsiveness, evidenced by high Information Coefficient scores in various market conditions.

Automate Strategy Finding with LLM in Quant Investment

Introduction

The paper "Automate Strategy Finding with LLM in Quant Investment" addresses the instability and high uncertainty in current deep learning models for quantitative trading by proposing a novel framework that integrates LLMs and multi-agent architectures to improve portfolio management and alpha mining. It introduces a framework composed of multiple modules that leverage LLMs to mine alpha factors and ensemble learning to construct a diverse pool of trading agents with varying risk preferences.

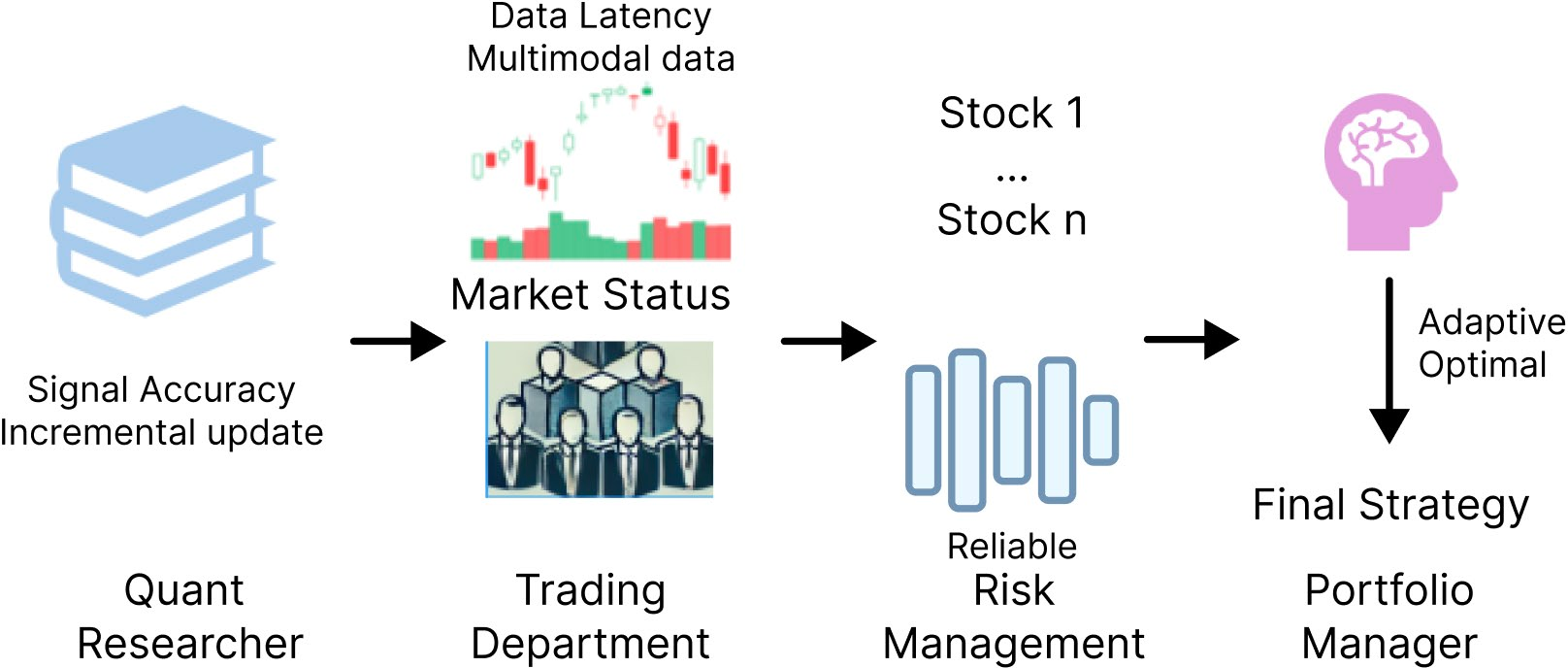

Figure 1: Pipeline of Quant Trading Company.

The framework is designed to dynamically adapt to market conditions and generate adaptive investment strategies. It begins by collecting and categorizing potential alpha factors from various financial data sources using LLMs, followed by back-testing these seed alphas for performance evaluation. This evaluation includes specific market conditions to determine their capacity to yield excess returns. The process is enhanced by a multi-agent system that assesses these factors within multimodal market scenarios. An adaptive composite alpha formula is then created by dynamically weighing the relevance of each agent.

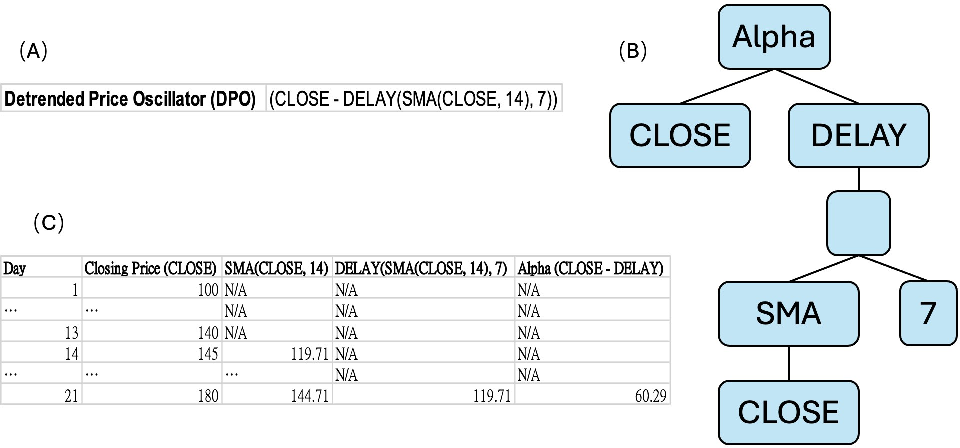

Figure 2: (A) An example of the seed alpha; (B) Its equivalent expression tree; (C) Step-by-step computation of this seed alpha on an example time series.

Methodology

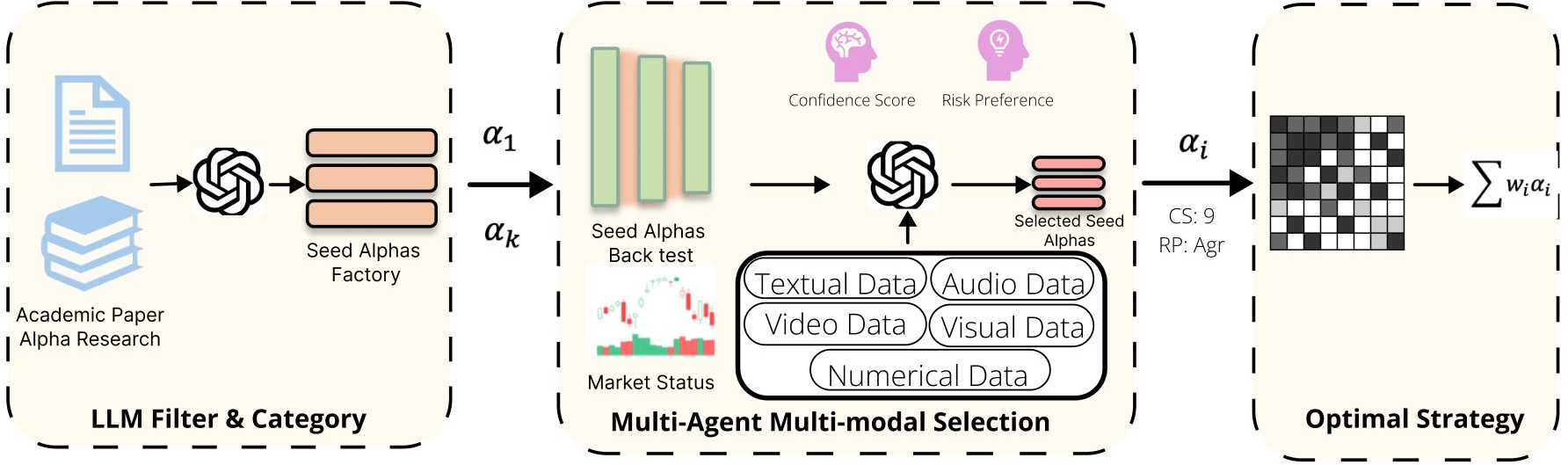

The methodology is structured into three main components:

- LLM Filter and Category: The framework utilizes the summarization and categorization capabilities of LLMs to build a Seed Alphas Factory. This involves processing vast multimodal datasets to filter and categorize seed alphas into independent alpha categories.

- Multi-Agent Evaluation: Specialized agents evaluate the relevance of each seed alpha based on real-time market conditions. This multi-agent approach captures nuanced market dynamics from various perspectives, allowing for a more sophisticated analysis of alpha strategy efficacy.

- Dynamic Strategy Optimization: A Deep Neural Network (DNN) is used to optimize the weights assigned to selected alphas, based on their historical performance and current market conditions. This results in a dynamically adaptive investment strategy.

Figure 3: Overview of the strategy generate process (CS stands for confidence score; RP stands for risk preference).

Experiment

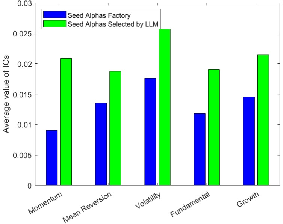

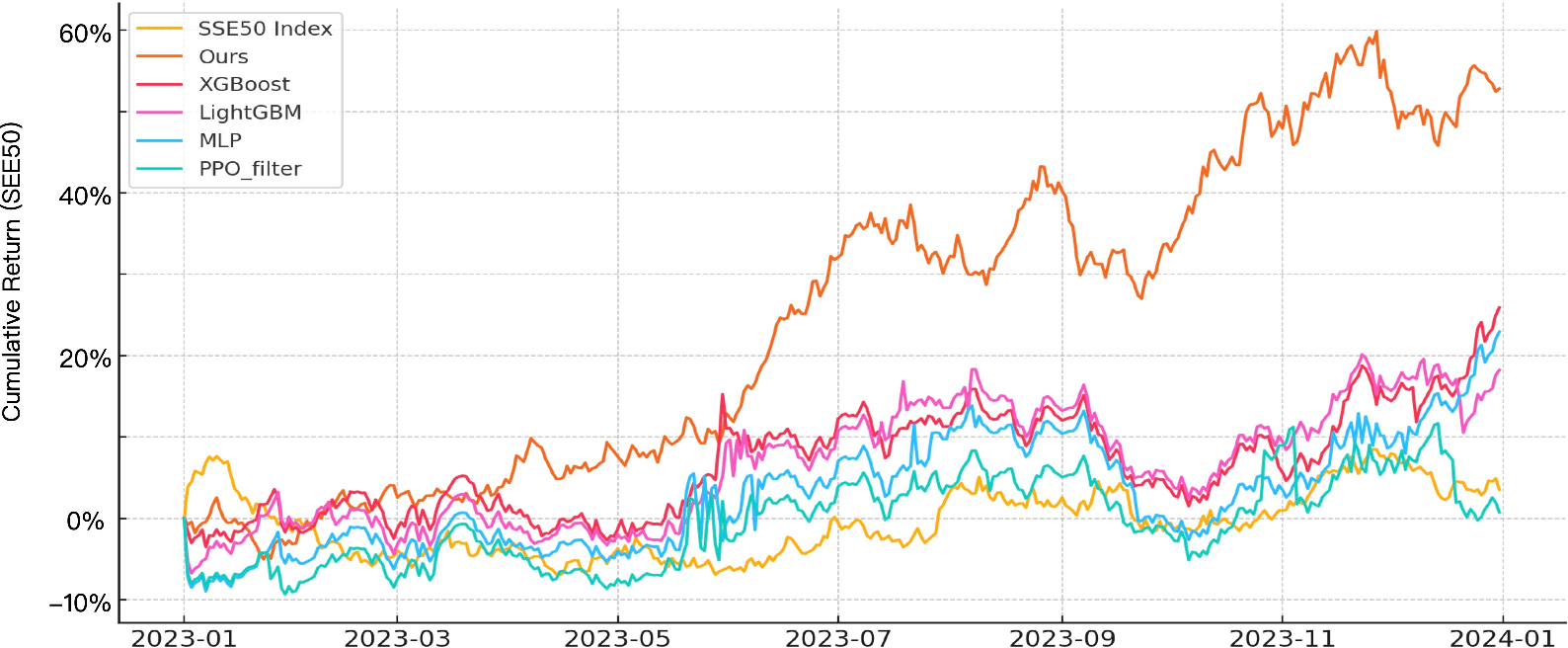

The experiments demonstrate the framework's capability to extract multimodal knowledge and select relevant alphas that adapt to changing market conditions. The proposed strategy, when tested on the SSE 50 Index dataset, shows significant outperformance over traditional alpha mining methods. The Information Coefficient (IC) metric is used to measure predictive power, with higher IC values indicating superior alpha strategies. The back-test results show a cumulative return significantly higher than the index, underscoring the framework's effectiveness.

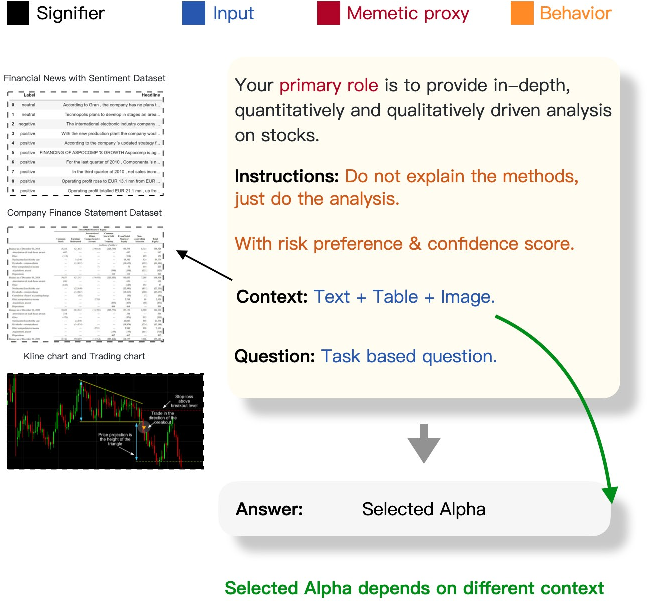

Figure 4: Multimodal LLM Analysis architecture.

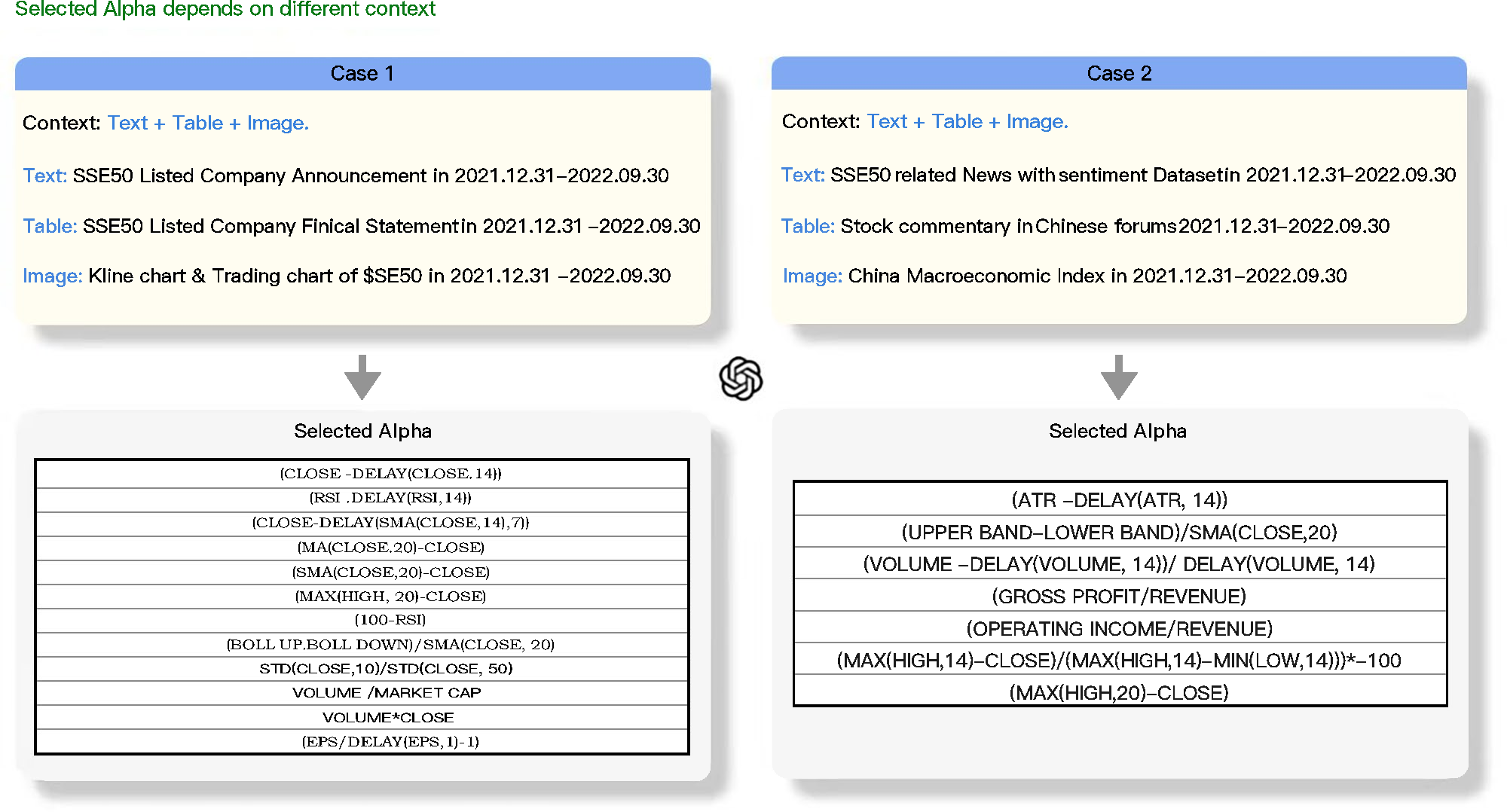

Figure 5: Sample Experiment on Different Market Status Input and Alpha Selection.

Figure 6: Average IC Comparation after LLM Selection.

Figure 7: Backtest Result on SSE50 Comparison Between Index and Our performance.

The research aligns with existing studies on formulaic alphas and financial domain LLMs, situating itself within the intersection of AI-enhanced stock prediction and investment strategy optimization. The introduction of multi-agent systems and LLMs represents a methodological shift from traditional heuristic-based models to more dynamic, data-driven approaches.

Conclusion

The proposed framework offers a significant advancement in quantitative stock investment by leveraging LLMs and multi-agent architectures to enhance alpha mining and portfolio management. The framework's adaptability and robust performance across various market conditions highlight the potential of AI-driven approaches in finance. Future investigations might explore the integration of knowledge graph techniques and consideration of more sophisticated mixture-of-experts models to further refine alpha selection and strategy optimization.