- The paper presents a robust model detecting sequence-independent and sequence-dependent cross-chain arbitrages in decentralized finance.

- The methodology analyzes transaction timing, amounts, and bridge usage to validate arbitrage strategies over nine blockchains.

- The study highlights key security implications, including centralization, network congestion, and private mempool usage in DeFi.

Cross-Chain Arbitrage: The Next Frontier of MEV in DeFi

The paper "Cross-Chain Arbitrage: The Next Frontier of MEV in Decentralized Finance" explores the emergent and complex practice of cross-chain arbitrage within decentralized finance (DeFi), aiming to uncover its mechanics, prevalence, profitability, and security implications. This study uniquely focuses on Sequence-Independent Arbitrage (SIA) and Sequence-Dependent Arbitrage (SDA), detailing their execution strategies across various blockchains.

Methodology

Arbitrage Detection Model

The paper introduces a robust model for detecting cross-chain arbitrages, focusing primarily on two-hop arbitrages involving pairs of transactions across different blockchains. Arbitrage matches are validated by examining transaction amounts and timings, while also ensuring associated entities by either identical EOA or interacted smart contracts across the chains.

Bridge Usage Detection

Arbitrage strategies are categorized based on bridge usage. Native and multichain bridges support asset transfer between blockchains, and the paper proposes two detection methods: unique identifiers for native bridges, and ERC-20 token transfer events for multichain bridges.

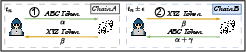

Figure 1: Sequence-Independent Cross-Chain Arbitrage (SIA).

Analysis of Cross-Chain Arbitrages

The study spans nine blockchains and reveals approximately 260,808 cross-chain arbitrages generating lower-bound profits of $9,496,115 from nearly$465,797,487 in traded volume. Arbitrum emerges as the most active network by arbitrage count, with Ethereum leading in traded volume due to its liquidity.

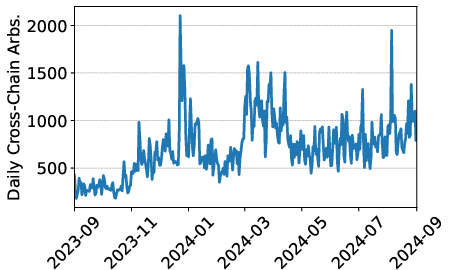

Figure 2: Daily number of cross-chain arbitrages executed between September 2023 and August 2024.

Arbitrage Durations and Tokens

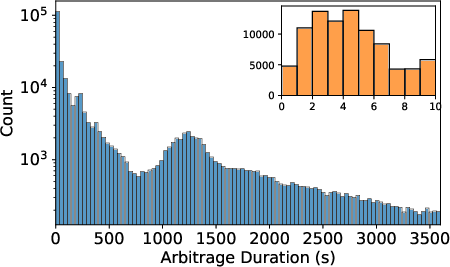

Arbitrage durations generally exhibit positive skewness, often completed within seconds, though some require extended periods due to bridging delays. Token analysis highlights low-liquidity tokens being heavily involved, deviating from typical modalities involving stable, highly liquid token pairs like WETH-USDC.

Figure 3: Distribution of cross-chain arbitrage durations with an inset plot highlighting the first ten seconds where arbitrages frequently occur.

Security Implications

Arbitrageur Centralization

A single address, 0xCA74, controls a significant portion of the arbitrage market, indicating centralization tendencies. This centralization is further compounded by the strategic execution necessary for SIA, demanding off-chain coordination and inventory management.

Network Congestion

High failure rates among top smart contract-based arbitrageurs, particularly on Polygon, suggest potential network congestion from failed transaction attempts, highlighting the risks involved in non-atomic arbitrage operations.

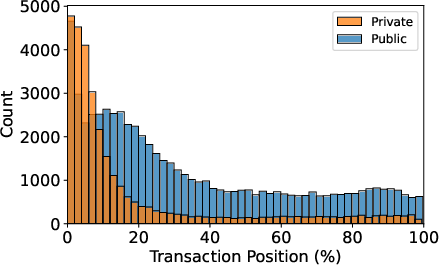

Private Mempools

The growing use of private mempools, particularly on Ethereum, gives arbitrageurs a competing edge by ensuring transaction priority without exposing them to frontrunning risks. This trend indicates an increasing sophistication in arbitrage strategies, seeking execution advantages.

Figure 4: Distribution of normalized cross-chain arbitrage transaction positions (%) for public and private transactions on Ethereum.

Sequencer Incentives and Future Directions

Sequencer Incentives

As cross-chain arbitrages gain momentum, controlling transaction sequencing across blockchains becomes potential collateral damage, posing threats of centralization. Shared-sequencing solutions, such as Espresso Systems and Astria, could mitigate risks by enabling fair and decentralized access.

Risk-Optimized Strategy

Innovative arbitrage strategies, as shown in the paper, potentially alleviate risks by employing loans and leveraging bridging mechanics, allowing for flexible responses to market dynamics while managing asset positions efficiently.

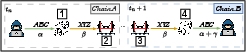

Figure 5: Example of a risk-optimized cross-chain arbitrage strategy between Ethereum and Arbitrum, where the arbitrageur completes the arbitrage at tn±ϵ using a loan and later closes the loan position with the bridged output of the hedge leg upon its arrival at tn+1.

Conclusion

The emergence of cross-chain arbitrages signifies an evolution in MEV and DeFi landscapes, emphasizing the need for both strategic adaptability and infrastructure collaboration across blockchain networks. The paper solidifies its contribution by detailing practical methodologies and highlighting potential systemic risks requiring strategic foresight and collaborative solutions in blockchain interoperability. The adaptation of shared-sequencing platforms represents a promising avenue for sustaining decentralization and equitable opportunity in cross-chain MEV extraction.