- The paper demonstrates that integrating ChatGPT's real-time analysis of firm news significantly enhances risk-adjusted momentum strategy performance.

- It employs a novel prompt-engineered approach to extract predictive signals for dynamically adjusting stock selection and portfolio weights.

- Empirical results reveal substantial improvements in Sharpe and Sortino ratios, while also reducing transaction costs with optimal rebalancing frequencies.

ChatGPT in Systematic Investing -- Enhancing Risk-Adjusted Returns with LLMs

Introduction

The paper "ChatGPT in Systematic Investing -- Enhancing Risk-Adjusted Returns with LLMs" investigates the potential of LLMs for improving cross-sectional momentum strategies by extracting predictive signals from firm-specific news (2510.26228). The focal point of the study lies in utilizing ChatGPT prompts engineered to extract insights in real-time, enhancing the performance of momentum portfolios typically dominated by historical price data. These signals condition stock selection and portfolio weights, seeking to outperform standard benchmarks in financial markets.

Methodology

The research constructs a dataset by combining daily U.S. equity returns from S&P 500 constituents with high-frequency news data. A bespoke prompt-engineered interaction with ChatGPT is designed, where the model evaluates firm-specific news to predict the continuation of recent stock performance. Such evaluations produce scores used dynamically to weigh stocks in momentum portfolios. These prompt-engineered interactions not only frame the LLM as an interpreter of financial news with real-time implications but also aim to derive incremental value from established momentum strategies.

Data Sources

- Equity Returns: S&P 500 constituents are used due to their liquidity and coverage.

- News Articles: Stock-specific articles are sourced, facilitating a granular analysis of intraday market responses.

- Prompt Engineering: Custom prompts guide ChatGPT to assess the momentum continuation likelihood based on recent news. This methodology enables score generation that reflects the probability of a stock’s upward trend continuation.

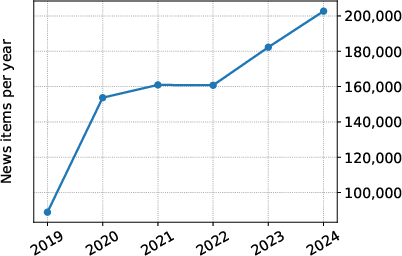

Figure 1: Time-Series of total yearly news items utilized in the analysis.

Results

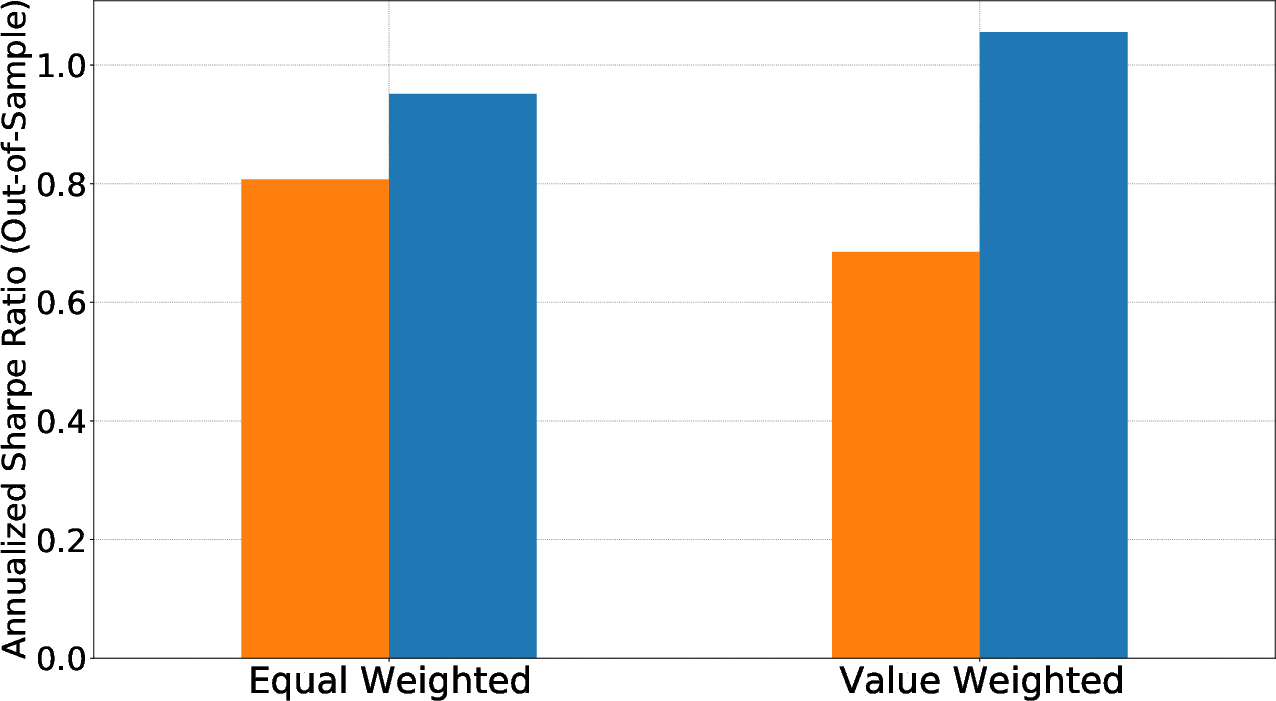

The paper demonstrates that incorporating LLM-driven insights into traditional momentum strategies yields economically significant performance improvements. The LLM-enhanced strategy, designed with a particular focus on news sentiment scores, consistently delivers higher Sharpe and Sortino ratios compared to the baseline momentum benchmark in both in-sample and out-of-sample tests.

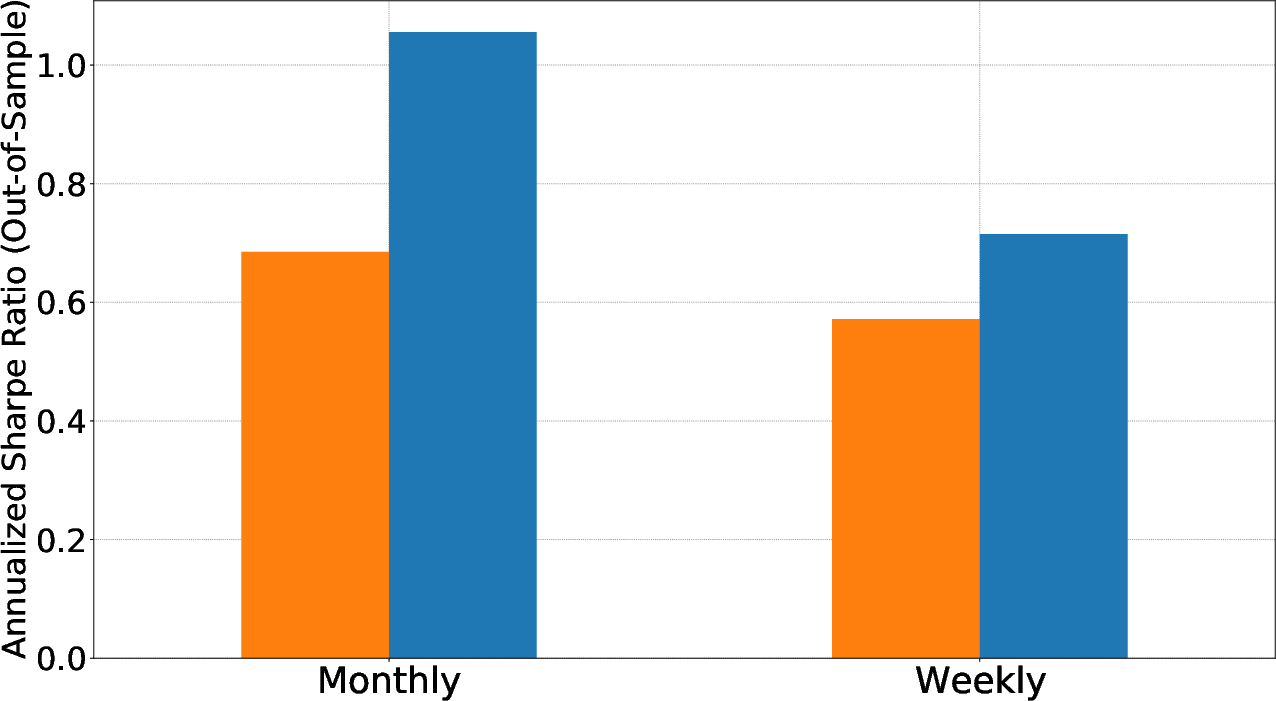

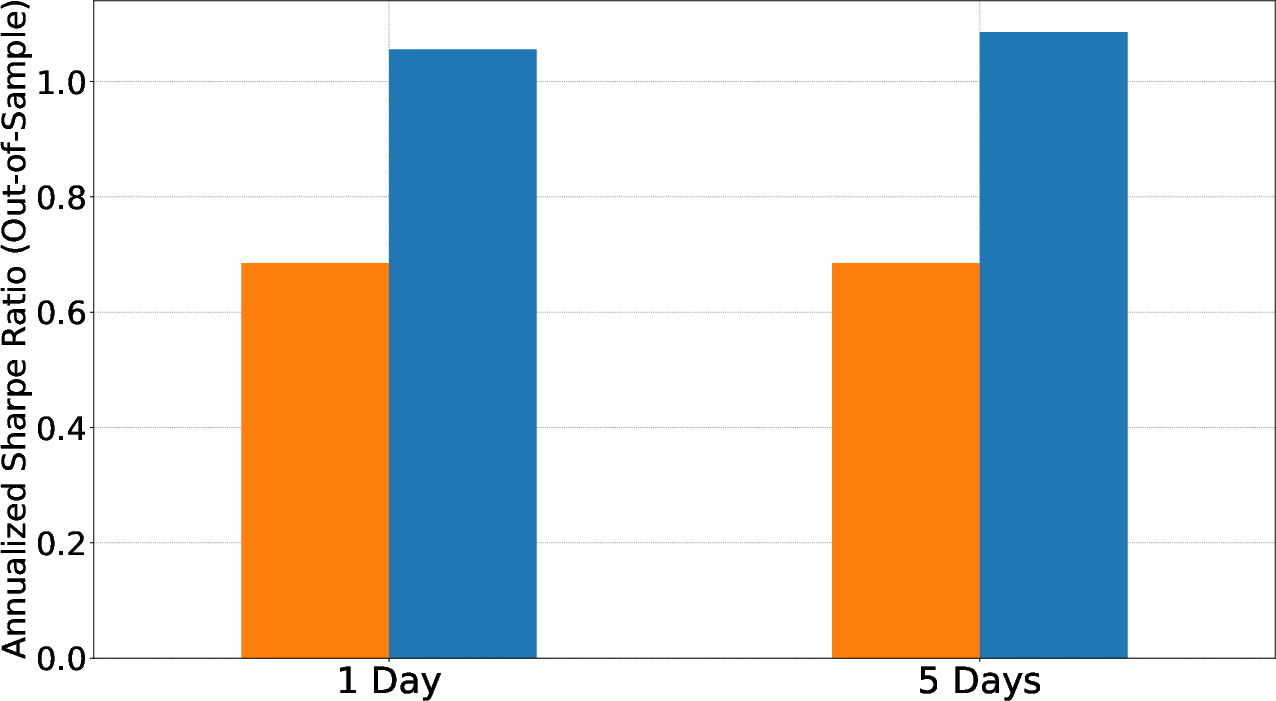

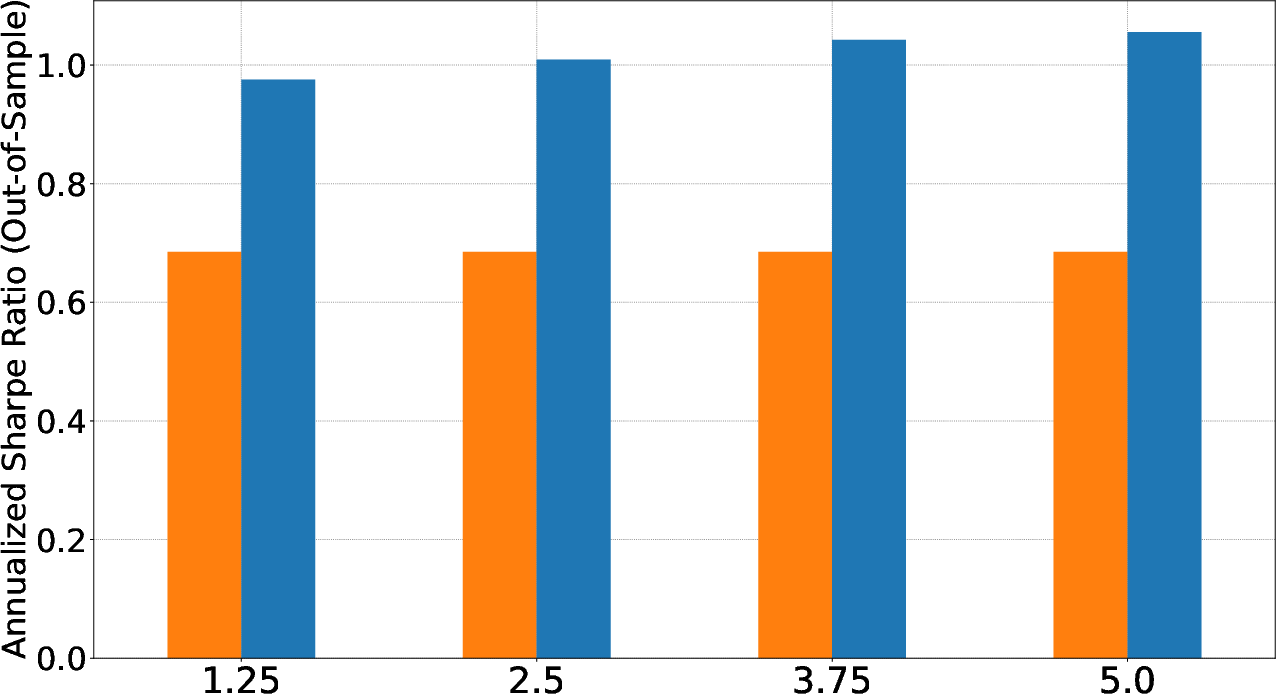

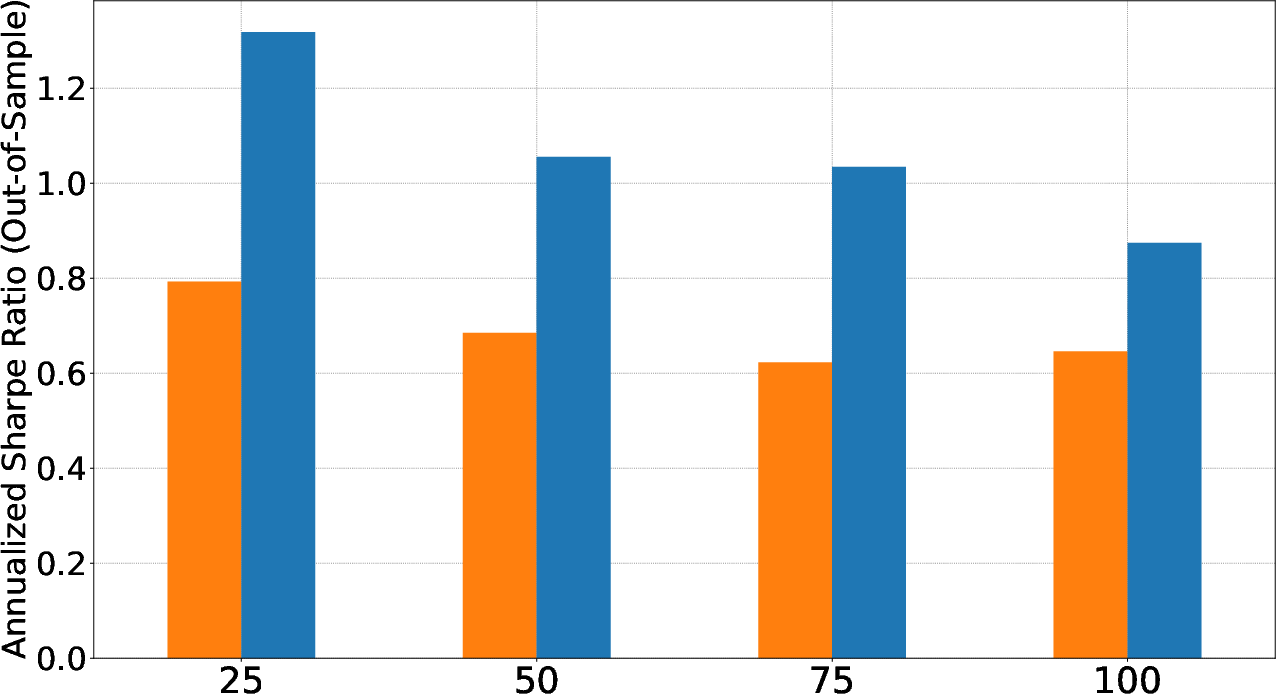

The optimal strategy identified encompasses several key parameters: a one-day news lookback, monthly rebalancing frequency, and concentrated selection of high-conviction stocks. Notably, the LLM-enhanced portfolio showed a Sharpe ratio improvement from 0.57 to 0.69 in the full sample, and from 0.79 to 1.06 in the out-of-sample period. Such improvements underscore the effectiveness of real-time news integration into momentum signal frameworks.

Figure 2: The cumulative returns of the best performing LLM-Enhanced strategy versus a baseline momentum strategy, highlighting superior performance post-ChatGPT integration.

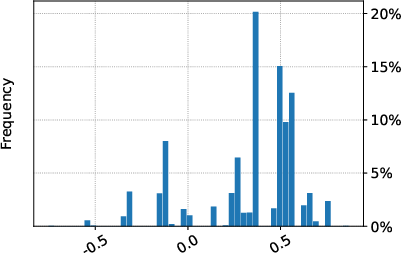

Parameter Sensitivity

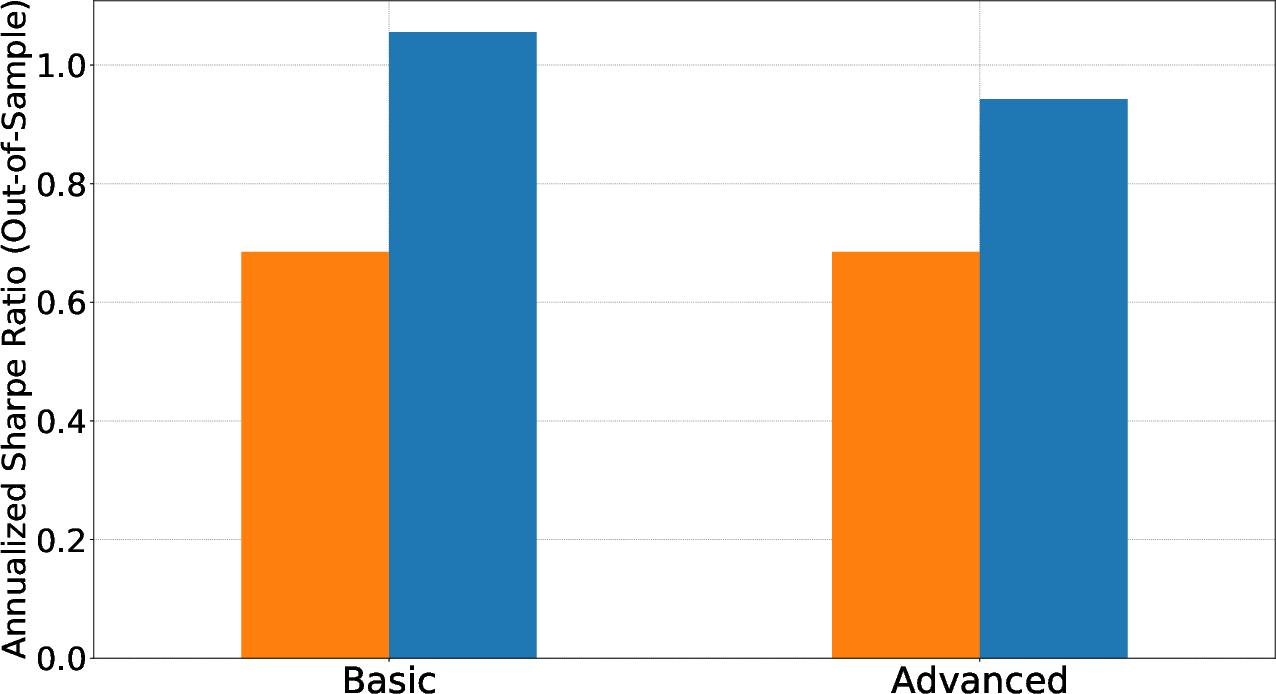

The LLM strategy demonstrates enhanced results at a monthly rebalancing frequency due to reduced transaction costs and increased turnover. The study finds that simpler prompt designs produce slightly better performance, indicating efficacy even without complex input formulations.

Figure 3: Sharpe ratio variations as affected by different rebalancing frequencies, showcasing optimal periods for trade efficiency.

Conclusion

This study provides compelling evidence for integrating LLMs into momentum-based investing strategies, highlighting that LLMs can interpret financial news and extract signals that enhance the performance of momentum portfolios. The findings suggest that LLMs, like ChatGPT, can add measurable value by dynamically interpreting firm-specific news, thus representing a viable approach to marrying machine learning advancements with financial strategy design.

Overall, while the research underscores the inherent limitations related to a limited out-of-sample period, the robust performance after the model's training data cutoff and strong in-sample results advocate for the promising role of LLMs in systematic investing.

Future research could further explore model fine-tuning, broader market applications, and integration with alternative datasets to continue advancing the efficacy of AI-enhanced financial strategies.