- The paper introduces a novel framework that incorporates endogenous market resistance and a concave price impact function via a nonlinear stochastic Fredholm equation.

- The methodology employs a combined analytical and numerical approach, including Nyström discretization and backward Picard iterations achieving error rates below 10⁻¹¹.

- The empirical analysis demonstrates that varying resistance convexity significantly alters trading aggressiveness, emphasizing the need to adjust execution strategies in illiquid markets.

Optimal Trading with Market Resistance and Concave Price Impact: Analytical Structure and Numerical Implications

Introduction and Theoretical Framework

This paper, "Trading with market resistance and concave price impact" (2601.03215), situates itself at the intersection of contemporary market microstructure modeling and optimal execution strategies. It rigorously investigates how endogenous market resistance—arising from strategic antagonistic trading in response to metaorders—shapes the dynamics of price impact, departing from the canonical linear models to capture the empirically observed concave and transient response of prices.

The authors introduce a framework where a strategic trader faces a sophisticated counterparty capable of (partially) detecting and anti-correlating her metaorder, thus exerting resistance to her market impact. The core mathematical model features a concave, transient price impact specified through a power-law propagator kernel and a parametric resistance function, both encoded within a generalized Volterra operator framework. This structure captures both empirical regularities (such as the square-root law for impact as a function of participation) and the microstructural feedback between order flow and liquidity provision.

Classically, market impact models ignore adversarial resistance and specify the impacted price as a linear convolution of order flow through a decaying kernel. In this work, the authors build upon frameworks proposed in [durin2023two] and others, formalizing how a resistance term arises naturally when liquidity providers exploit temporary mispricings induced by large trades.

Specifically, market resistance is modeled as a fixed-point problem: the resistance rate at time t is given by $r^u_t = \mathcal{U}\left(\int_0^t G_{\lambda, \nu}(t-s)\big(u_s - r^u_s\big)\,\dd s \right)$, with a resistance function U whose convexity captures the aggression and detection ability of antagonistic agents.

These microstructural insights yield a market impact law where impact no longer scales linearly with traded volume; instead, for sufficiently convex U, it exhibits power-law behavior and recovers the empirical square-root law for large metaorders. The resistance mechanism attenuates the permanent impact by offsetting the component of order flow detected as uninformed.

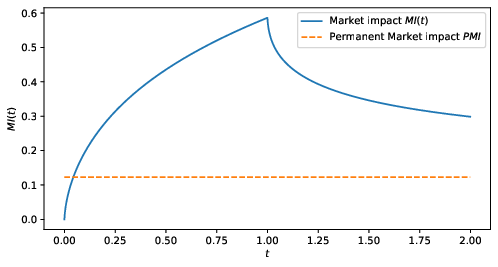

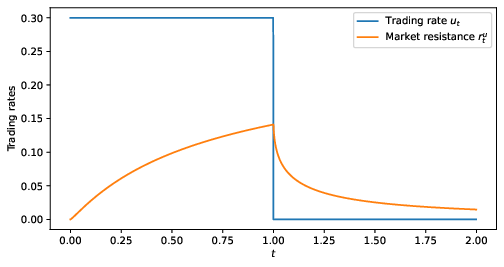

Figure 1: Market impact profile highlights the time course of price response and corresponding trading/resistance rates under a typical execution scenario with quadratic resistance.

Optimal Trading Problem: Mathematical Structure and Existence

The optimal trading problem is formulated as a stochastic control problem, maximizing expected PnL under transient and permanent price impact in the presence of resistance and risk penalties. The main theoretical advance is the derivation of a first-order optimality condition in the form of a nonlinear stochastic Fredholm equation. In the linear resistance regime, the problem admits a unique solution characterized by the positive semidefiniteness of the effective impact operator. In the general convex case, the authors leverage coercivity, Fréchet differentiability, and monotonicity to establish (under technical conditions) the existence of an optimal control.

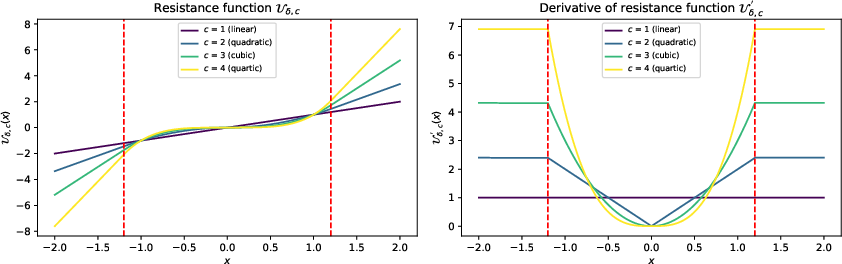

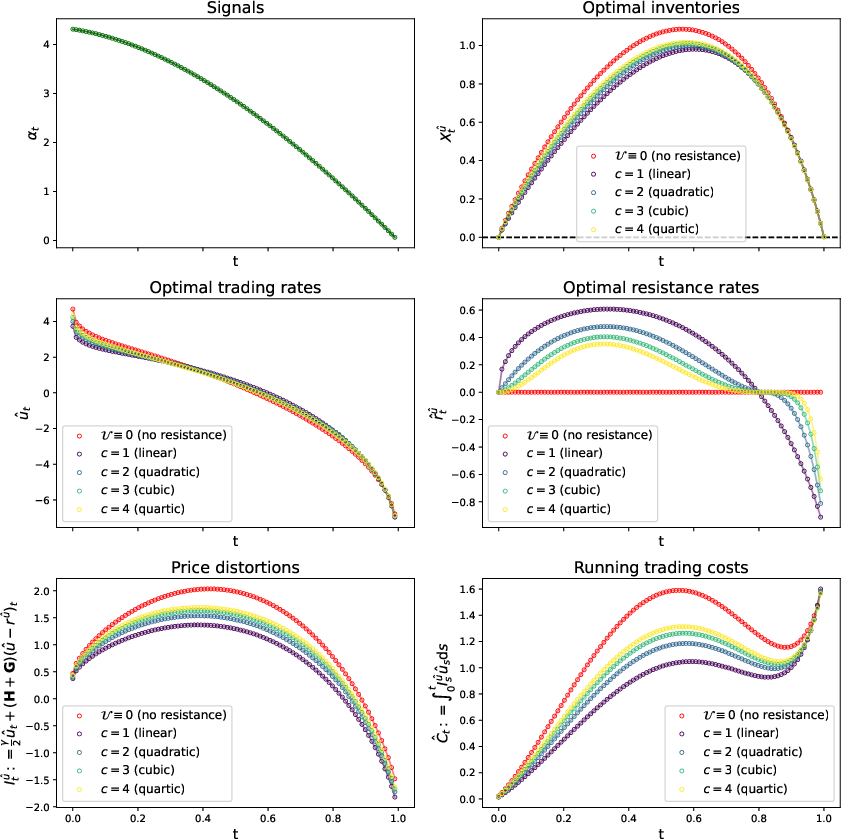

The resistance function's convexity c plays a central role; the transition from c=1 (linear, adversarial reaction proportional to impact) to c=2 (quadratic, more realistic in view of empirical square-root laws) and higher modulates both the shape and persistence of market impact.

Figure 2: Resistance function specification demonstrates the sensitivity of the resistance function and its derivative with respect to different convexity parameters c.

Numerical Approach and Algorithmic Contributions

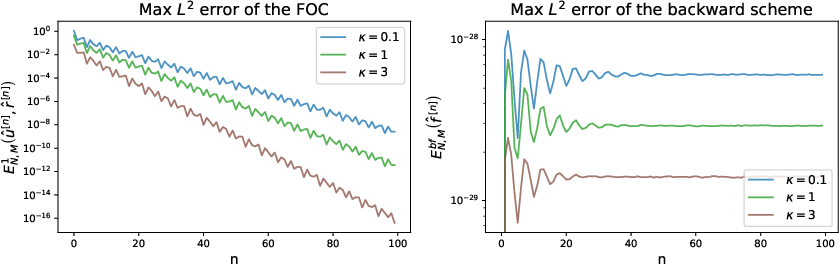

Given the nonlinearity and high-dimensionality of the resulting stochastic Fredholm equation, the authors devise an efficient iterative scheme based on Nyström discretization and backward Picard iterations for the resistance fixed point. Theoretically, they establish exponential convergence of their scheme under moderate technical regularity; numerically, they verify stringent accuracy criteria (e.g., errors below 10−11 for 100 iterations) across various market configurations.

Figure 3: Convergence of the numerical scheme as a function of signal decay demonstrates rapid error reduction consistent with exponential convergence theory.

Their regression-based approach (using Ridge and Laguerre expansions for conditional expectations in the stochastic setting) allows robust estimation even in the presence of noisy alpha signals, with tractable behavior under discretization and stochastic simulation.

Sensitivity Analysis, Empirical Regimes, and Trading Implications

The numerical section is particularly detailed in illustrating how optimal round trips—executions prompted by temporally extended buy signals—are qualitatively shaped by both market resistance specifications and impact decay properties.

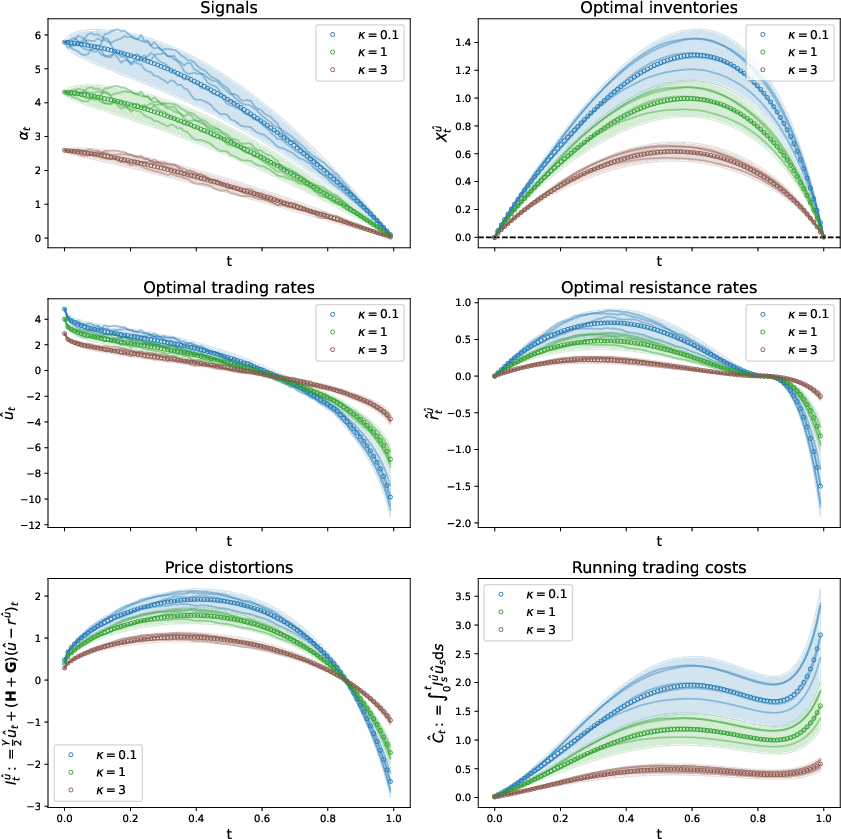

- Signal Mean Reversion: For slower mean-reverting signals, optimal trading becomes more aggressive, inducing larger resistance and higher temporary price distortion.

- Convexity of Resistance: Increasing convexity parameter c in U causes the trading rate to become more aggressive and resistance rates to display more pronounced lags near zero when changing transaction direction. Notably, with c=2, the square-root law in participation emerges as an endogenous outcome, not a modeling postulate.

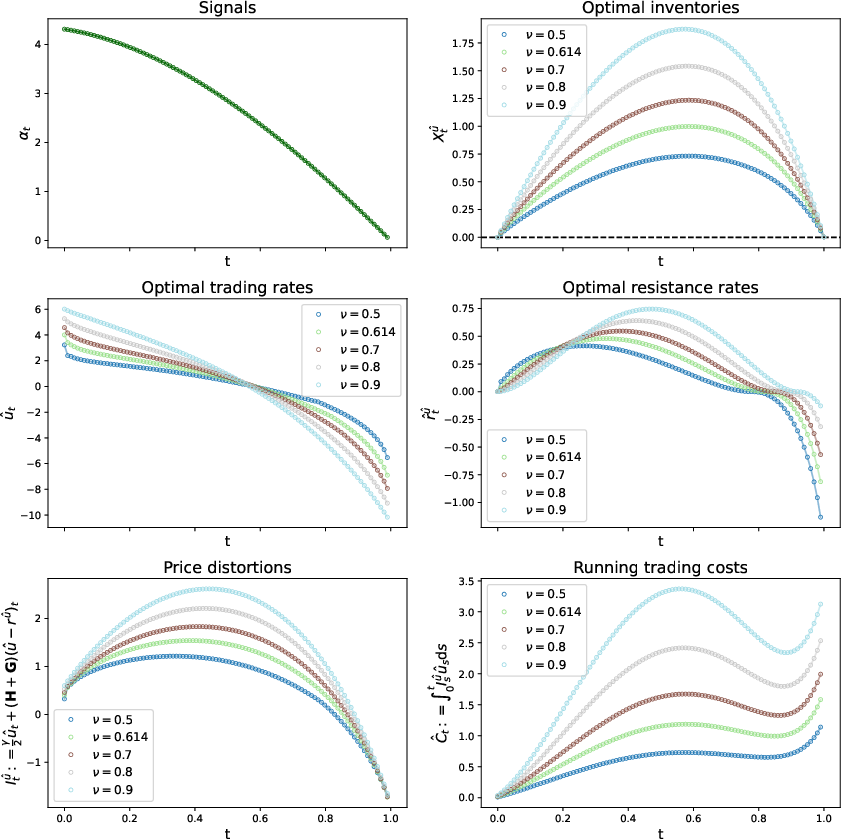

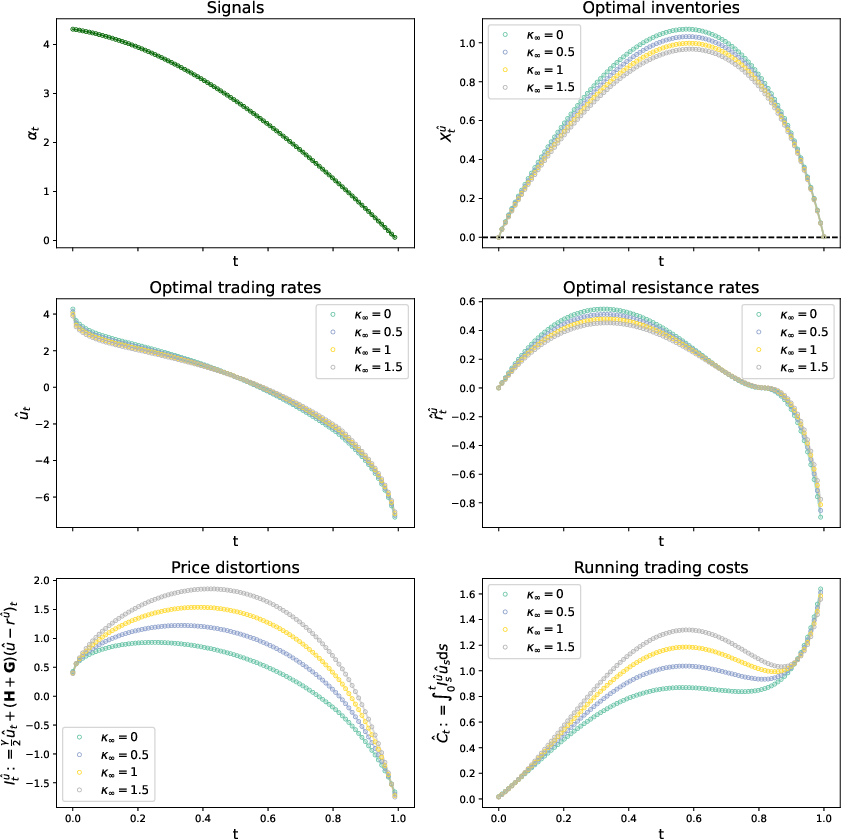

- Impact Decay and Permanent Impact: Faster kernel decay (ν→1) encourages more aggressive trades, while higher permanent impact coefficient κ∞ reduces aggressiveness, reflecting the role of long-term price effect in execution cost minimization.

Figure 4: Optimal round-trips for buy signals with different mean-reversion rates κ, demonstrating the interplay between alpha decay and trading/resistance profile.

Figure 5: The effect of resistance convexity on trading behavior, contrasting absence of resistance with increasing convexity parameters c.

Figure 6: Sensitivity of optimal round-trips to different impact decay exponents ν in the power-law kernel, showing how more persistent impact slows round trip completion.

Figure 7: The effect of permanent impact κ∞ modulation on aggressiveness and completion of optimal round trips.

Theoretical and Practical Implications

The model provides a flexible unification of market impact mechanisms, allowing researchers and practitioners to interpolate between classical linear propagators and empirically validated, resistance-dampened nonlinear regimes. The endogenous emergence of the square-root law, driven by microstructural detection and antagonistic trading, clarifies the circumstances under which the law manifests and provides a route to stress-test the robustness of algorithmic execution strategies under varying liquidity and signal-detection environments.

In terms of optimal execution, the results imply that ignoring resistance effects (e.g., as implicit in non-adversarial Almgren–Chriss-type models) can significantly underestimate expected impact costs and misestimate the trading speed-risk tradeoff, particularly in high participation and illiquid settings.

On the mathematical front, the analysis connects non-Markovian control under path-dependent and nonlinear impact with advanced tools from Fredholm theory and operator differential equations, extending earlier results to the presence of stochastic signals and robustly nonlinear cost surfaces.

Conclusion

This paper rigorously characterizes optimal trading in markets exhibiting endogenous resistance and nonlinear, concave impact. It establishes both analytical and numerical existence of optimal controls, explores the parametric sensitivity of market quality and trading efficiency, and offers an implementable algorithmic blueprint for practical execution. The model’s ability to interpolate between regimes and its microstructural foundation suggest multiple avenues for future research: including models of partial (imperfect) resistance, multi-agent equilibrium extensions, and robust estimation in live market data environments.