- The paper’s main contribution is evaluating three position sizing methods in put-writing, revealing the hybrid Kelly-VIX approach’s superior risk control.

- The analysis demonstrates that ultra-short-dated, far OTM options deliver enhanced risk-adjusted returns through dynamic sizing validated by Monte Carlo simulations.

- The paper offers actionable insights for institutional investors, emphasizing portfolio diversification and drawdown management amid variable market volatility.

Overview

"Sizing the Risk: Kelly, VIX, and Hybrid Approaches in Put-Writing on Index Options" (2508.16598) explores systematic put-writing strategies for the S&P 500 Index, emphasizing position sizing as a determinant of long-term performance. Despite the recognized volatility risk premium, the practical application of short-dated put-writing strategies lacks clarity in prior literature. This paper evaluates three position sizing techniques: the Kelly criterion, VIX-based volatility regime scaling, and a novel hybrid strategy blending both. The findings show that ultra-short-dated, far out-of-the-money (OTM) options yield superior risk-adjusted returns. The hybrid sizing consistently manages return generation and drawdown control, particularly under low-volatility conditions. This research offers actionable insights for institutional investors aiming to integrate systematic volatility harvesting into diversified portfolios.

Methodology

Position Sizing Strategies

- Kelly Criterion: Based on maximizing logarithmic wealth growth, applied using a Monte Carlo simulation to estimate probabilities and outcomes.

- VIX-Rank Sizing: Dynamically adjusts position size based on the VIX's percentile rank over a historical window, with the rank indicating market sentiment.

- Hybrid Kelly-VIX Approach: Combines the Kelly criterion with VIX-Rank as a scaling factor, adapting bet sizes according to volatility conditions.

Strategy Configurations

Results

Kelly Criterion Sizing

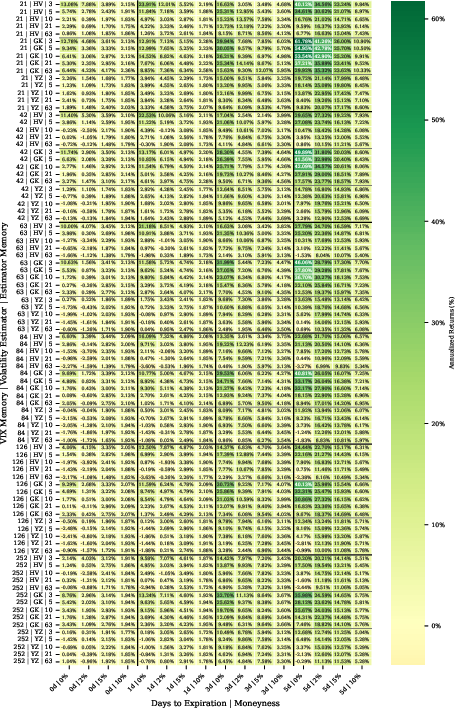

- Performance: The best results were observed with 5-10% OTM options and 0-1 DTE.

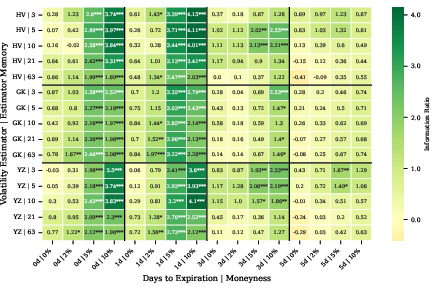

- Volatility Estimators: The Garman-Klass estimator was most effective with longer windows (63 days), while shorter windows (5-10 days) favored Yang-Zhang.

- Risk-Adjusted Returns: Kelly sizing excelled in risk control but with modest absolute returns.

VIX-Rank Sizing

- DTE Impact: Longer DTE resulted in higher absolute returns, whereas shorter DTE provided better information ratios.

- VIX Tenor Variety: Shorter VIX tenors (e.g., VIX9D) yielded better risk-adjusted results due to more relevant short-term volatility insights.

Kelly-VIX Sizing

Implementation and Considerations

Computational Requirements

- Monte Carlo Simulations: Essential for estimating Kelly fractions, demanding significant computational resources depending on scenario complexity.

- Historical Volatility Calculations: Require high-frequency market data for effective implementation.

Practical Applications

- Institutional Investors: These strategies provide avenues for enhancing portfolio efficiency through systematic volatility premia exposure.

- Market Regime Adaptation: The hybrid method is particularly adaptable to shifting market environments, seamlessly adjusting position sizes.

Implications for Portfolio Management

- Diversification: The put-writing techniques discussed offer an opportunity for diversification within portfolios, emphasizing controlled risk.

- Drawdown Management: Hybrid approaches deliver consistent control over potential losses, crucial during market downturns.

Conclusion

The insights from "Sizing the Risk: Kelly, VIX, and Hybrid Approaches in Put-Writing on Index Options" contribute valuable strategies for institutional investors focusing on volatility risk premiums through systematic put-writing. The combination of dynamic sizing methods adapts efficiently to market conditions, enhancing risk-adjusted returns across various scenarios. Future work should explore parameter sensitivity, alternative underlyings, and international markets to further bolster the robustness of these findings.