- The paper presents a novel implicit numerical method combined with policy iteration to solve the complex HJBQVI in market making.

- It incorporates an alpha signal via an Ornstein-Uhlenbeck process to optimally manage order execution and mitigate inventory risk.

- The methodology demonstrates unconditional stability and improved computational efficiency through rigorous convergence analysis under monotonicity and diagonal dominance.

Analysis of the Implicit Numerical Scheme for HJBQVI in Market Making

Introduction

The paper "Implicit Numerical Scheme for the Hamilton-Jacobi-Bellman Quasi-Variational Inequality in the Optimal Market-Making Problem with Alpha Signal" (2512.20850) introduces an implicit numerical method designed to solve a complex optimization problem related to market making within a limit order book. The study addresses the challenges of traditional explicit time discretization schemes by offering an unconditionally stable alternative, namely an implicit numerical scheme combined with a policy iteration algorithm. This approach is geared towards optimizing the profitability of market making activities while considering both stochastic and impulse controls.

Market making plays a vital role in providing liquidity in electronic exchanges, characterized by the continuous submission of limit and market orders. The paper builds upon classical market making models by incorporating an alpha signal—a stochastic process reflecting predictability in price dynamics. This introduces a Hamilton-Jacobi-Bellman Quasi-Variational Inequality (HJBQVI) as a representation of the optimization problem, which combines stochastic control with impulse control mechanisms.

The paper constructs a framework in which the midprice of an asset evolves in response to stochastic Poisson processes influenced by both bid and ask dynamics. The alpha signal, representing price trend information, is instilled within the model through an Ornstein-Uhlenbeck process that reflects market imbalances. The market maker's goal is effectively articulated as minimizing inventory risk while capitalizing on predictable price movements.

Numerical Scheme and Convergence

An implicit time discretization scheme is propounded to resolve the HJBQVI. This scheme circumvents the time-step constraints typically imposed by explicit methods, facilitating computational efficiency and accuracy. The policy iteration algorithm computes solutions for discretized forms of the HJBQVI at each time step.

The convergence to the unique viscosity solution is substantiated under conditions of monotonicity, stability, and consistency, leveraging the comparison principle. Moreover, the policy iteration algorithm is validated using convergence results pertaining to diagonal dominance conditions, ensuring the reliable derivation of numerical solutions.

Numerical Experiment

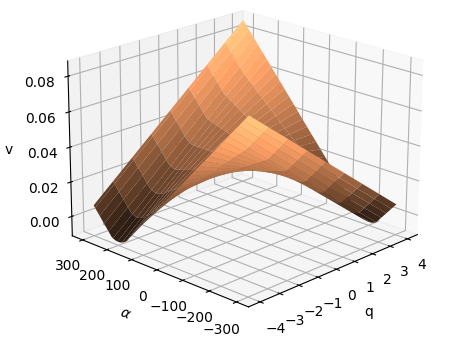

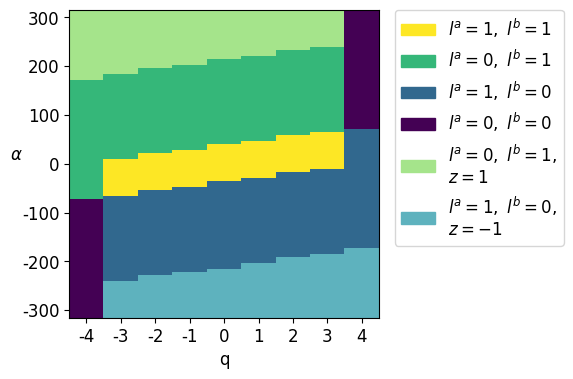

The experimental setup features a numerical resolution of the HJBQVI with specified parameters such as trading horizon, asset price increments, and market order intensities. The numerical results demonstrate the surface of the value function and the optimal control strategy at the initial time.

Figure 1: Surface of the value function v at time t=0.

The findings articulate the adaptive strategy employed by market makers as influenced by the alpha signal, with optimal control transitioning between limit and market orders based on the signal's magnitude.

Implications and Future Directions

The advancement of an implicit numerical scheme for solving HJBQVI in market making paves the way for enhancing the computational efficiency and accuracy of trading strategies in electronic exchanges. By mitigating time-step constraints, the method supports the deployment of more sophisticated market models that include predictable components.

Future directions may involve extending the methodology to encompass broader classes of financial instruments and market conditions, thereby augmenting the robustness and versatility of market making strategies. Additionally, the integration of machine learning techniques could complement the alpha signal's role, further refining trade execution under stochastic and impulse controls.

Conclusion

The paper delivers a comprehensive exploration of an implicit numerical approach to tackle the HJBQVI in the market making problem, providing substantial improvements over explicit methods. The rigorous mathematical framework and numerical validation underscore the utility of the proposed scheme in advancing high-frequency trading strategies.